As

filed with the Securities and Exchange Commission on June 7, 2024

Registration

No. 333-[●]

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

DC 20549

FORM

F-3

REGISTRATION

STATEMENT

UNDER

THE

SECURITIES

ACT OF 1933

DOGNESS

( INTERNATIONAL ) CORPORATION

(Exact

name of registrant as specified in its charter)

| British

Virgin Islands |

|

N/A |

|

Not

Applicable |

(State

or other jurisdiction

of

incorporation or organization) |

|

(Translation

of Registrant’s

Name

into English) |

|

(I.R.S.

Employer

Identification

No.) |

No.

16 N. Dongke Road

Tongsha

Industrial Zone

Dongguan,

Guangdong 523217

+86-769-38958222

(Address,

including zip code, and telephone

number,

including area code, of registrant’s

principal

executive offices) |

|

CT

Corporation System

111

Eighth Avenue

New

York, New York 10011

(800)

624-0909

(Name,

address including zip code, and

telephone

number, including area code, of agent

for

service) |

With

a copy to:

Anthony

W. Basch, Esq.

Benming Zhang, Esq.

Kaufman

& Canoles, P.C.

Two

James Center

1021

East Cary Street, Suite 1400

Richmond,

Virginia 23219

Fax:

804-771-5777

Approximate

date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement as determined

by the registrant.

If

the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check

the following box: ☐

If

any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the

Securities Act of 1933, check the following box. ☒

If

this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the

following box and list the Securities Act registration statement number of the earlier effective registration statement for the same

offering. ☐

If

this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If

this Form is a registration statement pursuant to General Instruction I.C. or a post-effective amendment thereto that shall become effective

upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. ☐

If

this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.C. filed to register additional

securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. ☐

Indicate

by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933. Emerging growth

company ☐

If

an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided

pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

†

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards

Board to its Accounting Standards Codification after April 5, 2012.

The

registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the

registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective

in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date

as the Commission acting pursuant to said Section 8(a) may determine.

The

information in this prospectus is not complete and may be changed. The selling shareholders named in this prospectus may not sell these

securities until the registration statement filed with the Securities and Exchange Commission is declared effective. This prospectus

is not an offer to sell these securities and the selling shareholders named in this prospectus are not soliciting offers to buy these

securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY

PROSPECTUS |

SUBJECT

TO COMPLETION |

DATED

JUNE 7, 2024 |

Up

to 2,000,000 Class A Common Shares

Offered

by the Selling Shareholders of

DOGNESS

( INTERNATIONAL ) CORPORATION

This

prospectus relates to the resale from time to time by the selling shareholders identified in this Prospectus under the caption “Selling

Shareholders” (the “Selling Shareholders”) of up to 2,000,000 of our Class A Common Shares, no par value per share

(the “Resale Shares”) issued in a private placement at a price of $2.50 per share, pursuant to certain securities purchase

agreement entered on May 9, 2024.

The

Selling Shareholders may sell any or all of the Resale Shares offered by this prospectus from time to time on terms to be determined

at the time of sale through ordinary brokerage transactions or through any other means described in this prospectus under the caption

“Plan of Distribution.” The Resale Shares may be sold at fixed prices, at market prices prevailing at the time of sale, at

prices related to prevailing market price or at negotiated prices.

We

will not receive any of the proceeds from the sale of the Resale Shares by the Selling Shareholders and we will bear all costs,

expenses and fees in connection with the registration of the Resale Shares offered hereby.

Our

Class A Common Shares are listed on the NASDAQ Capital Market under the symbol “DOGZ”. On June 6, 2024, the closing

sale price of our Class A Common Shares as reported by the NASDAQ Capital Market was $13.75.

The

Resale Shares are being registered to permit the Selling Shareholders, or their respective pledgees, donees, transferees or other successors-in-interest,

to sell the Resale Shares from time to time in the public market. We do not know when or in what amount the Selling Shareholders may

offer the securities for sale. The Selling Shareholders may sell some, all or none of the securities offered by this Prospectus.

The

Resale Shares may be sold by the Selling Shareholders to or through underwriters or dealers, directly to purchasers or through agents

designated from time to time. For additional information regarding the methods of sale you should refer to the section entitled “Plan

of Distribution” in this Prospectus.

All

references to “we”, “us”, “our Company,” “the Company,” or “our” are to Dogness

( International ) Corporation and its subsidiaries. “RMB,” “Renminbi” and “¥” are to the legal

currency of China and all references to “USD,” “U.S. dollars,” “dollars,” and “$” are

to the legal currency of the United States.

Investing

in our securities being offered pursuant to this prospectus involves a high degree of risk. You should carefully read and consider the

risk factors beginning on page 21 of this prospectus and in the applicable prospectus supplement before you make your investment

decision.

We

are not a Chinese operating company but a British Virgin Islands holding company with operations conducted by our subsidiaries established

in Delaware, mainland China, Hong Kong Special Administrative Region of the People’s Republic of China and British Virgin Islands.

Therefore, investing in our securities involves unique and a high degree of risk. You should carefully read and consider the risk factors

of this report (beginning on page 21), especially the risk factors under the caption “Risks Related to Our Corporate Structure

and Operation” (beginning on Page 28) and “Risks Related to Doing Business in China” (beginning on page 34).

Unless

otherwise indicated or the context requires otherwise, references in this prospectus to “China” or the “PRC”

are to the mainland of People’s Republic of China, Taiwan, Hong Kong Special Administrative Region of the People’s Republic

of China (“HKSAR” or “Hong Kong”), and the special administrative regions of Macau (for the purposes of this

prospectus only); “mainland China” are to the mainland of the People’s Republic of China, excluding Taiwan Hong Kong,

and Macau (for the purposes of this prospectus only); “Mainland China Subsidiaries” refer to our subsidiaries incorporated

in mainland China, including Dogness Intelligent Technology (Dongguan) Co., Ltd., a mainland China company (“Dongguan Dogness”),

Dongguan Jiasheng Enterprise Co., Ltd., a mainland China company (“Dongguan Jiasheng”), Zhangzhou Meijia Metal Product Co.,

Ltd, a mainland China company (“Meijia”), and Dogness Intelligence Technology Co., Ltd., a mainland China company (“Intelligence

Guangzhou”); “Hong Kong Subsidiaries” refer to our subsidiaries incorporated in Hong Kong, including Jiasheng Enterprise

(Hongkong) Co., Limited, a Hong Kong company (“HK Jiasheng”) and Dogness (Hongkong) Pet’s Products Co., Limited, a

Hong Kong company (“HK Dogness”). We will also refer to all of our subsidiaries, as the “Subsidiaries”.

The

Securities registered under the Securities Act and the Exchange Act are of the off-shore holding company Dogness ( International ) Corporation

(the “Company”), a British Virgin Islands business company, which owns equity interests, directly or indirectly, of the operating

subsidiaries. Subsidiaries conduct operations in China and the holding company does not conduct operations in China.

We

are subject to legal and operational risks associated with being based in and having the majority of the company’s operations in

mainland China and Hong Kong. These risks include, among others, the following:

| |

● |

PRC

government oversight. The Chinese government may impose regulations on the operation of our Hong Kong and mainland China operating

entities and exercise significant oversight over the conduct of their business, and may exert more supervision over offerings conducted

overseas and/or foreign investment in China-based issuers, which could result in a material change in our operations and/or the value

of our Class A Common Shares. Any actions by the Chinese government to exert more oversight and supervision over offerings that are conducted

overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue

to offer Securities to investors and cause the value of such securities to significantly decline or be worthless. See Risk Factors

– Risks Related to Doing Business in China – “Changes in China’s economic, political and social conditions,

as well as in any government policies, laws and regulations from time to time may cause us to change the way we operate our business

and, could have a material adverse effect on our business and the value of our Class A Common Shares” and “The Chinese

government exerts substantial oversight over our business activities and may decide to strengthen such supervision from time to time,

which could result in a material change in our operations and the value of our Class A Common Shares” and “The Chinese

government exerts oversight and supervision over overseas offerings and listing conducted by China-based issuers under the Listing Records

Rules and/or the Confidentiality Provisions, which could significantly limit or completely hinder our ability to offer or continue to

offer our Class A Common Shares to investors and could cause the value of our Class A Common Shares to significantly decline or become

worthless.” |

| |

|

|

| |

● |

PRC

legal enforcement risk. The mainland China legal system is based on written statutes. Prior court decisions may be cited

for reference but have limited precedential value. We conduct our business primarily through our subsidiaries established in China.

These subsidiaries are generally subject to laws and regulations applicable to foreign investment in China. However, since these

laws and regulations could change from time to time and the mainland China legal system continues to rapidly evolve, the interpretations

and enforcement of many laws, regulations and rules are subject to changes at the same time, we may not be able to accurately predict

what legal protections would be available to us in future. See Risk Factors – Risks Related to Doing Business in China

– “The laws and regulations of mainland China could change from time to time, and we may not be able to accurately

predict what legal protections would be available to us in future”. |

| |

|

|

| |

● |

Shareholder

enforcement risk. Since we conduct a significant portion of our operations in mainland China, the majority of our assets

are located in mainland China, and all of our directors, officers or senior management other than Yunhao Chen, are located in mainland

China, it may be more difficult for shareholders to enforce liabilities and enforce judgments on those individuals compared to doing

so in your home country against defendants resided in your home country. Our PRC legal counsel, Jincheng Tongda & Neal

Law Firm, or JT&N, has advised us that mainland China does not have treaties providing for the reciprocal recognition and enforcement

of judgments of courts with the British Virgin Islands and the United States. Therefore, we cannot assure the recognition and enforcement

in mainland China of judgments of a court in British Virgin Islands or the United States in relation to any matter not subject to

a binding arbitration provision. See Risk Factors – Risks Related to Doing Business in China – “You may

experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing original actions in mainland

China or Hong Kong against us, compared to doing so in your home country against defendants resided in your home country, and the

ability of U.S. authorities to bring actions in mainland China may also be limited”. |

| |

● |

Repatriation

of offering proceeds to PRC. In utilizing the proceeds of this offering in the manner described in “Use of Proceeds,”

as an offshore holding company of our PRC operating subsidiary, we may decide to make loans or additional contributions to our Mainland

China subsidiaries. Certain governmental registrations, submissions or approvals need to be completed or obtained in this regard.

Failure to complete such registrations, submissions or obtain such approvals, our ability to use the proceeds from our initial public

offering and to capitalize or otherwise fund our PRC operations may be negatively affected. See Risk Factors – Risks Related

to Doing Business in China – “We must remit the offering proceeds to China before they may be used to benefit our

business in China, the process of which may be time-consuming, and we cannot assure that we can finish all necessary governmental

registration processes in a timely manner” and “PRC regulation of loans and direct investment by offshore holding

companies to mainland China entities may delay or prevent us from using the proceeds of this Offering to make loans or additional

capital contributions to our Mainland China Subsidiary, which could materially and adversely affect our liquidity and our ability

to fund and expand our business”. |

| |

|

|

| |

● |

Restriction

on currency conversion. The PRC government imposes restrictions on the convertibility of the RMB into foreign currencies and,

in certain cases, the remittance of currency out of mainland China. We receive a majority of our revenues in Renminbi, which currently

is not a freely convertible currency. Restrictions on currency conversion imposed by the PRC government may limit our ability to

use revenues generated in Renminbi to fund our expenditures denominated in foreign currencies or our business activities outside

mainland China. See Risk Factors – Risks Related to Doing Business in China – “Governmental restrictions

on currency conversion may limit our ability to use our revenues effectively and the ability of our Mainland China Subsidiaries to

obtain financing”. |

| |

|

|

| |

● |

Restrictions

on dividend payment. As a holding company, we rely principally on dividends and other distributions on equity from our subsidiaries,

including those based in China, for our cash requirements, including for services of any debt we may incur. Our Mainland China Subsidiaries’

ability to distribute dividends is based upon their distributable earnings. Current PRC regulations permit our Mainland China Subsidiaries

to pay dividends to their respective shareholders only out of their accumulated profits, if any, determined in accordance with PRC

accounting standards and regulations. In addition, if our Mainland China Subsidiaries incur debt on their own behalf in the future,

the instruments governing the debt may restrict their ability to pay dividends or make other payments to us. Any limitation on the

ability of our Mainland China Subsidiaries to distribute dividends or other payments to their respective shareholders could materially

and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends

or otherwise fund and conduct our business. See Risk Factors – Risks Related to Doing Business in China – “We

may rely on dividends and other distributions on equity paid by our subsidiaries, including those based in the PRC, for our cash

and financing requirements we may have, and any limitation on the ability of our Mainland China Subsidiaries to make payments to

us could have a material and adverse effect on our ability to conduct our business”. |

| |

|

|

| |

● |

Possibility

to be classified as “Resident Enterprise.” Under the Enterprise Income Tax Law, Dogness may be classified as a “Resident

Enterprise” of China. Such classification will likely result in unfavorable tax consequences to us and our shareholders outside

of mainland China, including repayment of any underpayments and penalties for underpayment. See Risk Factors – Risks Related

to Doing Business in China – “We may be classified as a “resident enterprise” for mainland China enterprise

income tax purposes; such classification could result in unfavorable tax consequences to us and our non-PRC shareholders”. |

Recently,

the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance

notice, including cracking down on illegal activities in the securities market, adopting new measures to impose filing requirements on

China-based companies for their initial public offerings or listings in overseas stock markets and extend the scope of cybersecurity

reviews, and expanding the efforts in anti-monopoly enforcement.

On

July 6, 2021, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council

jointly released the Opinions on Severely Cracking Down on Illegal Securities Activities According to Law, or the Opinions. The Opinions

emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over

overseas listings by Chinese companies. Effective measures, such as promoting the construction of relevant regulatory systems will be

taken to deal with the risks and incidents of China-concept overseas listed companies, and cybersecurity and data privacy protection

requirements, etc. The Opinions and any related implementing rules to be enacted may subject us to compliance requirement in the future.

On

February 17, 2023, with the approval of the State Council, China Securities Regulatory Commission (the “CSRC”) issued the

relevant system and rules for the management of overseas listing records, which will be implemented from March 31, 2023. A total of six

institutional rules (the “Listing Records Rules”) have been issued this time, including the Trial Measures for the Administration

of Overseas Issuance and Listing of Securities by Domestic Enterprises (hereinafter referred to as the “Trial Measures”)

and five supporting guidelines. Under the Listing Records Rules, a company established in mainland China seeking securities offering

and listing, by both direct or indirect means, in an overseas market is required to undertake filing procedures with the CSRC for its

overseas offering and listing activities. The Trial Measures also set forth a list of circumstance under which overseas offering and

listing by domestic companies established in mainland China is prohibit, including: (i) where such securities offering and listing is

explicitly prohibited by the PRC laws; (ii) where the intended securities offering and listing may endanger national security as reviewed

and determined by competent PRC authorities under the State Council in accordance with PRC laws; (iii) where the domestic company established

in mainland China, or its controlling shareholders and the actual controller, have committed crimes such as corruption, bribery, embezzlement,

misappropriation of property or undermining the order of the socialist market economy during the latest three (3) years; (iv) where the

domestic company established in mainland China seeking securities offering and listing is suspected of committing crimes or major violations

of laws and regulations, and is under investigation according to law, and no conclusion has yet been made thereof; and (v) where there

are material ownership disputes over equity held by the controlling shareholder of the company established in mainland China or by other

shareholders that are controlled by the controlling shareholder and/or actual controller. In accordance with the Trial Measures, the

listing and trading of our Class A Common Shares on Nasdaq is deemed as an indirect overseas offering and listing by domestic companies

established in mainland China, and thus, we are subject to the Listing Records Rules and the relevant filing procedures as required.

Further, we believe, as of the date of this prospectus, none of the circumstances prohibiting the overseas offering and listing by domestic

companies established in mainland China as listed above applies to us, and we can offer and continue to offer our Class A Common Shares

on Nasdaq.

In

accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC

along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we have been listed overseas

before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall

carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-on offerings on Nasdaq,

dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control,

investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing

status or transfer of listing segment, and voluntary or mandatory delisting. If we or our mainland China Subsidiaries in future fail

to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of

the Trial Measures, the CSRC may order rectification, issue warnings to us and/or our mainland China Subsidiaries, and impose a fine

of between RMB 1,000,000 yuan and RMB 10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions,

such as the SEC, via cross-border securities regulatory cooperation mechanisms.

Further,

on February 24, 2023, the CSRC, together with Ministry of Finance, National Administration of State Secrets Protection, and National

Archives Administration of China, released the Provisions on Strengthening the Confidentiality and Archives Administration Related to

the Overseas Securities Offering and Listing by Domestic Enterprises (the “Confidentiality Provisions”), which came into

effect on March 31, 2023 with the Trial Measures. Under the Confidentiality Provisions, domestic companies established in mainland China

seeking overseas offering and listing, by both direct and indirect means, are required to institute a sound confidentiality and archives

system. If such domestic companies established in mainland China intend to, either directly or through its overseas listed entity, publicly

disclose or provide to relevant individuals or entities including securities companies, securities service providers and overseas regulators,

any documents and materials that contain state secrets or working secrets of government agencies, they shall obtain approval from competent

authorities and complete the relevant filing procedure with the competent secrecy administrative department prior to their disclosure

or provision of such documents and materials. Further, if they provide or publicly disclose documents and materials which may adversely

affect national security or public interests, they shall strictly follow the corresponding procedures in accordance with relevant laws

and regulations. Once effective, any failure or perceived failure by us or our subsidiaries to comply with the above confidentiality

and archives administration requirements under the Confidentiality Provisions and other relevant PRC laws and regulations may cause relevant

entities to be held legally liable by competent authorities, and referred to the judicial organ to be investigated for criminal liability

if suspected of committing a crime. As of the date of this prospectus, we believe that we and our subsidiaries have not provided or publicly

disclosed any documents or materials involving state secrets or work secrets of PRC government agencies or any of which may adversely

affect national security or public interests, to relevant securities companies, securities service institutions, overseas regulatory

agencies and other entities and individuals. We intend to continue strictly complying with the Confidentiality Provisions and other relevant

PRC laws and regulations in our offering and listing on Nasdaq.

However,

any failure of us or our mainland China Subsidiaries to fully comply with the Listing Records Rules and/or the Confidentiality Provisions

may significantly limit or completely hinder our ability to offer or continue to offer our Class A Common Shares on Nasdaq, cause significant

disruption to our business operations, severely damage our reputation, materially and adversely affect our financial condition and results

of operations and cause our Class A Common Shares to significantly decline in value or become worthless. See “Risk Factors —

Risks Related to Doing Business in China — The Chinese government exerts oversight and supervision over overseas offerings and

listing conducted by China-based issuers under the Listing Records Rules and/or the Confidentiality Provisions, which could significantly

limit or completely hinder our ability to offer or continue to offer our Class A Common Shares to investors and could cause the value

of our Class A Common Shares to significantly decline or become worthless.”

We

or our Subsidiaries may also be subject to PRC laws relating to the use, sharing, retention, security and transfer of confidential and

private information, such as personal information and other data. On November 14, 2021, the Cyberspace Administration of China (“CAC”)

released the Regulations on the Network Data Security Management (Draft for Comments), or the Data Security Management Regulations Draft,

to solicit public opinion and comments till December 13, 2021, which has not been promulgated as of the date of this prospectus. Pursuant

to the Data Security Management Regulations Draft, data processors holding more than one million users/users’ individual information

shall be subject to cybersecurity review before listing abroad. Data processing activities refers to activities such as the collection,

retention, use, processing, transmission, provision, disclosure, or deletion of data. According to the latest amended Cybersecurity Review

Measures, which was promulgated on November 16, 2021 and became effective on February 15, 2022, an online platform operator holding more

than one million users/users’ individual information shall be subject to cybersecurity review before listing abroad. As of the

date of this prospectus, we have not been informed by any PRC governmental authority of any requirement that we or our Subsidiaries file

for approval for this offering. We don’t believe that we or any of our Subsidiaries will be subject to either the amended Cybersecurity

Review Measures or the Data Security Management Regulations Draft since none of us hold more than one million users/users’ individual

information. However, since the existing or new laws or regulations or detailed implementations and interpretations may be modified or

promulgated, there could be potential adverse impact on our Subsidiaries’ daily business operation, their ability to accept foreign

investments, and our ability to continue to list or offer securities on an U.S. exchange. See “Risk Factors — Risks Related

to Doing Business in China — The Chinese government exerts substantial oversight over our business activities and may decide

to strengthen such supervision from time to time, which could result in a material change in our operations and the value of our Class

A Common Shares.”

On

February 7, 2021, the Anti-Monopoly Committee of the State Council promulgated the Anti-monopoly Guidelines for the Platform Economy

Sector, or the Anti-monopoly Guideline, aiming to improve anti-monopoly administration on online platforms. The Anti-monopoly Guideline,

operating as the compliance guidance under the then-existing PRC anti-monopoly regulatory regime for platform economy operators, specifically

prohibits certain acts of the platform economy operators that may have the effect of eliminating or limiting market competition, such

as concentration of undertakings. The PRC anti-monopoly regulatory regime started with the Anti-Monopoly Law promulgated by the Standing

Committee of the National People’s Congress of China (“SCNPC”) on August 30, 2007 and effective on August 1, 2008,

which requires that transactions which are deemed concentrations and involve parties with specified turnover thresholds must be cleared

by the Ministry of Commerce of China (“MOFCOM”) before they can be completed. In addition, on February 3, 2011, the General

Office of the State Council promulgated a Notice on Establishing the Security Review System for Mergers and Acquisitions of Domestic

Enterprises by Foreign Investors, or Circular 6, which officially established a security review system for mergers and acquisitions of

domestic enterprises by foreign investors. Further, on August 25, 2011, MOFCOM promulgated the Regulations on Implementation of Security

Review System for the Merger and Acquisition of Domestic Enterprises by Foreign Investors, or the MOFCOM Security Review Regulations,

which became effective on September 1, 2011, to implement Circular 6. Under Circular 6, a security review is required for mergers and

acquisitions by foreign investors having “national defense and security” concerns and mergers and acquisitions by which foreign

investors may acquire the “de facto control” of domestic enterprises with “national security” concerns. Under

the MOFCOM Security Review Regulations, MOFCOM will focus on the substance and actual impact of the transaction when deciding whether

a specific merger or acquisition is subject to security review. If MOFCOM decides that a specific merger or acquisition is subject to

security review, it will submit it to the Inter-Ministerial Panel, an authority established under the Circular 6 led by the NDRC, and

MOFCOM under the leadership of the State Council, to carry out the security review. The regulations prohibit foreign investors from bypassing

the security review by structuring transactions through trusts, indirect investments, leases, loans, control through contractual arrangements

or offshore transactions.

The

Holding Foreign Companies Accountable Act (“HFCAA”) could subject us to a number of prohibitions, restrictions and potential

delisting if either we or our auditor was designated as a “Commission-Identified Issuer” or an auditor listed on an HFCAA

determination list, respectively. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act,

which, if enacted, would decrease the number of consecutive “non-inspection years” from three years to two, and thus our

shares could be prohibited from trading and delisted after two years instead of three. On August 26, 2022, the PCAOB signed a Statement

of Protocol with the China Securities Regulatory Commission and the Ministry of Finance of the PRC, which sets out specific arrangements

on conducting inspections and investigations by both sides over relevant audit firms within the jurisdiction of both sides, including

the audit firms based in mainland China and Hong Kong. This agreement marked an important step towards resolving the audit oversight

issue that concern mutual interests, and sets forth arrangements for both sides to cooperate in conducting inspections and investigations

of relevant audit firms, and specifies the purpose, scope and approach of cooperation, as well as the use of information and protection

of specific types of data.

On

December 15, 2022, the PCAOB Board determined that the PCAOB was able to secure access to inspect and investigate registered public accounting

firms headquartered in mainland China and Hong Kong and voted to vacate its previous determinations to the contrary. However, should

PRC authorities obstruct or otherwise fail to facilitate the PCAOB’s access in the future, the PCAOB Board will consider the need

to issue a new determination. On December 29, 2022, the Consolidated Appropriations Act, 2023, was signed into law, which, among other

things, amended the HFCAA to reduce the number of consecutive non-inspection years an issuer can be identified as a Commission-Identified

Issuer before the Commission must impose an initial trading prohibition on the issuer’s securities from three years to two years.

Therefore, once an issuer is identified as a Commission-Identified Issuer for two consecutive years, the Commission is required under

the HCFAA to prohibit the trading of the issuer’s securities on a national securities exchange and in the over-the-counter market.

However, as noted above, on December 15, 2022, the PCAOB vacated its previous determinations that it is unable to inspect and investigate

completely PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong. Accordingly, until such time as the

PCAOB issues any new determination, there are no issuers at risk of having their securities subject to a trading prohibition under the

HFCAA.

As

of the date hereof, our auditor, Audit Alliance LLP, is not among the auditor firms listed on the HFCAA determination list, which list

notes all of the auditor firms that the PCAOB is not able to inspect. However, trading in our securities on any U.S. stock exchange or

the U.S. over-the-counter market may be prohibited under the HFCAA if the PCAOB, issues a new determination and it also determines that

it cannot inspect the work papers prepared by our auditor and that as a result an exchange may determine to delist our securities. See

“Risk Factors — Trading in our securities may be prohibited under the Holding Foreign Companies Accountable Act if the

PCAOB determines that it cannot inspect or investigate completed our auditors for two consecutive years.” for more information.

Please

see “Risk Factors” starting on page 21 of this prospectus for additional information.

Neither

the Securities and Exchange Commission, British Virgin Islands, nor any state securities commission has approved or disapproved of these

securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The

date of this prospectus is [ ], 2024

Table

of Contents

ABOUT

THIS PROSPECTUS

This

prospectus describes the general manner in which the Selling Shareholders identified in this prospectus may offer from time to time up

to 2,000,000 Class A Common Shares.

You

should rely only on the information contained or incorporated by reference in this prospectus or any prospectus supplement. We have not

authorized any person to provide you with different or additional information. If anyone provides you with different or inconsistent

information, you should not rely on it. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy

securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus

or any prospectus supplement, as well as information we have previously filed with the SEC and incorporated by reference, is accurate

as of the date on the front of those documents only. Our business, financial condition, results of operations and prospects may have

changed since those dates.

If

necessary, the specific manner in which the Resale Shares may be offered and sold will be described in a supplement to this prospectus,

which supplement may also add, update or change any of the information contained in this prospectus. To the extent there is a conflict

between the information contained in this prospectus and any prospectus supplement, you should rely on the information in such prospectus

supplement, provided that if any statement in one of these documents is inconsistent with a statement in another document having a later

date—for example, a document incorporated by reference in this prospectus or any prospectus supplement—the statement in the

document having the later date modifies or supersedes the earlier statement.

Neither

the delivery of this prospectus nor any distribution of Resale Shares pursuant to this prospectus shall, under any circumstances, create

any implication that there has been no change in the information set forth or incorporated by reference into this prospectus or in our

affairs since the date of this prospectus. Our business, financial condition, results of operations and prospects may have changed since

such date.

SPECIAL

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This

prospectus, each prospectus supplement and the information incorporated by reference in this prospectus and each prospectus supplement

contain certain statements that constitute “forward-looking statements” within the meaning of Section 27A of the Securities

Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The words “anticipate,” “expect,” “believe,”

“goal,” “plan,” “intend,” “estimate,” “may,” “will,” and similar

expressions and variations thereof are intended to identify forward-looking statements, but are not the exclusive means of identifying

such statements. Any statements regarding the intent, belief or current expectations of the Company and management that are subject to

known and unknown risks, uncertainties and assumptions are considered forward-looking statements. You are cautioned that any such forward-looking

statements are not guarantees of future performance and involve risks and uncertainties, and that actual results may differ materially

from those projected in the forward-looking statements.

Because

forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified, you should

not rely upon forward-looking statements as predictions of future events. The events and circumstances reflected in the forward-looking

statements may not be achieved or occur and actual results could differ materially from those projected in the forward-looking statements.

Except as required by applicable law, including the securities laws of the United States and the rules and regulations of the SEC, we

do not plan to publicly update or revise any forward-looking statements contained herein after we distribute this prospectus, whether

as a result of any new information, future events or otherwise.

PROSPECTUS

SUMMARY

This

summary highlights information that we present more fully in the rest of this prospectus. This summary does not contain all of the information

you should consider before buying Class A Common Shares in this offering. You should read the entire prospectus carefully, including

the “Risk Factors” section and the financial statements and the notes to those statements.

Our

Company – Overview

Our

company was born from a belief that dogs and cats are important parts of many modern families and should be treated as loved family members.

We design and manufacture fashionable and high-quality leashes, collars, harnesses to complement cats’ and dogs’ appearances

and keep them safe. From our 10,292 square meter manufacturing facility in the Tongsha Industrial Zone in Dongguan, Guangdong, China,

we design eye-catching products that pet owners are proud to have their pets wear. But beautiful leashes are useless if they break when

the dog pulls or if they do not meet stringent quality standards. So we build these products to tolerances we believe they will never

need, such as making sure our products withstand at least four to seven times as much force as the dogs are expected to exert, and we

subject these products to a variety of demanding tests. Most of our products are exported, including to the United States and Europe,

and sold to major retail stores, manufacturers, and wholesalers.

We

have developed a vertically integrated production facility, where we turn raw materials like plastic resin and metal alloys into the

fabrics, buckles and metal components of our pet products. We weave nylon threads into webbed ribbons for collars, dye and print patterns

and colors requested by our customers, machine alloy into buckles and then sew and assemble the components into final products.

Some

of our most exciting new products, the H2 smart harness and C2 smart collar, offer pet owners the ability to monitor and interact with

their pets nearly anywhere there is a cellular signal. We have worked with world-class technology companies to design the software and

hardware components that we think will help define the standard for smart collars. We have debuted our first run of these products at

pet exhibitions in the United States, Germany and China, and we are looking forward to actively marketing these products for sale to

customers.

We

believe our products can keep pets safe, and encourage owners and pets to interact more frequently and in new and interesting ways by

giving owners peace of mind that they can trust that a collar or harness is not to going to fail or that the retractable leash locking

button will lock instantly and reliably or that they can find their pet wearing a smart collar before any harm comes to it.

We

are not a Chinese operating company but a British Virgin Islands holding company with operations conducted by our Subsidiaries established

in Delaware, PRC, British Virgin Islands, and Hong Kong.

PRC

laws and regulations governing business operations will change from time to time, which may result in a material change in the operations

of our Mainland China Subsidiaries and Hong Kong Subsidiaries, significant depreciation of the value of our Class A Common Shares, or

a complete hindrance of our ability to offer or continue to offer our securities to investors and cause the value of such securities

to significantly decline or be worthless. The Chinese government may exert signification oversight on the operations of our PRC operating

entities, which could result in a material change in the operations of our PRC operating entities and/or the value of our Class A Common

Shares. Further, any actions by the Chinese government to exert more oversight and supervision over offerings that are conducted overseas

and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer

securities to investors and cause the value of such securities to significantly decline or be worthless. Recently, the PRC government

initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including

cracking down on illegal activities in the securities market, adopting new measures to extend the scope of cybersecurity reviews, and

expanding the efforts in anti-monopoly enforcement. See “Prospectus Summary — Permission Required from the PRC Authorities

for the Company’s Operation and to Issue Our Class A Common Shares to Foreign Investors”; “Risk Factor —

Our failure to obtain prior approval, if any, or to fulfill the requisite filing and reporting requirements of the China Securities

Regulatory Commission (“CSRC”) for the listing and trading of our Class A Common Shares on a foreign stock exchange could

delay this offering or could have a material adverse effect upon our business, operating results, reputation and trading price of our

Class A Common Shares”.

History

and Development of the Company

Dogness

( International ) Corporation (“Dogness”) was incorporated as a British Virgin Islands business company limited by shares

under the BVI Business Companies Act (As Revised), on July 11, 2016, as a holding company. Dogness and its subsidiaries (collectively

the “Company”) are principally engaged in the design and manufacture of pet products, including leashes and smart products,

and lanyards in China. Most products are exported to the U.S. and Europe and sold to pet stores, including major pet store chains.

Dogness

(Hongkong) Pet’s Products Co., Limited (“HK Dogness”) was incorporated in Hong Kong on March 10, 2009 as a private

company limited by shares. In a private company limited by shares — which is the most common way to establish a limited

company in Hong Kong — the liability of members is limited by the articles of association to the amount unpaid on

the shares held by such members. By comparison, in a company limited by guarantee, no share capital is required and member liability

is limited by the articles of association to the amount that the members respectively undertake to contribute in the event the company

is wound up; this type of limited company is more common for non-profit organizations.

HK

Dogness was established to operate principally as a trading company. The share capital of HK Dogness is HK$10,000, divided into 10,000

shares of HK$1.00 each. In connection with the formation of HK Dogness, all 10,000 shares were issued to Silong Chen, Dogness’

founder and Chief Executive Officer. On August 15, 2016, Silong Chen transferred his shares in HK Dogness to a third party who held on

Mr. Chen’s behalf in preparation for the subsequent transfer to Dogness; however, Silong Chen continued to control such shares.

After such interim transfer, the shares in HK Dogness were transferred to Dogness on January 9, 2017.

Jiasheng

Enterprise (Hongkong) Co., Limited (“HK Jiasheng”) was incorporated in Hong Kong on July 12, 2007 as a private company limited

by shares. HK Jiasheng was established to operate principally as a trading company. The share capital of HK Jiasheng is HK$10,000, divided

into 10,000 shares of HK$1.00 each. In connection with the formation of HK Jiasheng, all 10,000 shares were issued to Silong Chen, Dogness’

founder and Chief Executive Officer.

Dogness

Intelligent Technology (Dongguan) Co., Ltd. (“Dongguan Dogness”) was incorporated in China on October 26, 2016. Dongguan

Dogness was established to operate principally as a holding company. Dongguan Dogness has RMB 10 million in registered capital. In connection

with the formation of Dongguan Dogness, Silong Chen, Dogness’ founder and Chief Executive Officer, became the sole shareholder

of Dongguan Dogness.

Dongguan

Jiasheng Enterprise Co., Ltd. (“Dongguan Jiasheng”) was incorporated in China on May 15, 2009. Dongguan Jiasheng was established

to develop and manufacture pet leash and lanyard products. Dongguan Jiasheng has RMB 10,000,000 in registered capital. In connection

with the formation of Dongguan Jiasheng, Silong Chen, Dogness’ founder and Chief Executive Officer, became the sole shareholder

of Dongguan Dogness .

On

November 24, 2016, the Controlling Shareholder transferred his 100% ownership interest in Dongguan Jiasheng to Dongguan Dogness, which

is 100% owned by HK Dogness and considered a wholly foreign-owned entity (“WFOE”) in mainland China. On January 9, 2017,

the Controlling Shareholder transferred his 100% equity interests in HK Dogness and HK Jiasheng to Dogness. After the reorganization,

Dogness owns 100% equity interests of subsidiaries listed above.

The

reorganization of the legal structure was completed on January 9, 2017. The reorganization involved the incorporation of Dogness, a BVI

holding company, and Dongguan Dogness, a mainland China holding company; and the transfer of HK Dogness, HK Jiasheng, and Dongguan Jiasheng

(collectively, the “Transferred Entities”) from the Controlling Shareholder to Dogness and Dongguan Dogness. Prior to the

reorganization, the Transferred Entities’ equity interests were 100% controlled by the Controlling Shareholder.

In

January 2018, the Company formed a Delaware limited liability company, Dogness Group LLC (“Dogness Group”), with its operation

focusing primarily on product sales in the U.S. In February 2018, Dogness Overseas Ltd (“Dogness Overseas”) was established

in the British Virgin Islands as a holding company, which owns all of the interests in Dogness Group. All of the equity of Dogness Overseas

is owned by Dogness ( International ) Corporation.

On

March 16, 2018, the Dongguan Dogness entered into a share purchase agreement to acquire 100% of the equity interests in Zhangzhou Meijia

Metal Product Co., Ltd (“Meijia”) from its original shareholder, Long Kai (Shenzhen) Industrial Co., Ltd (“Longkai”),

for a total cash consideration of approximately $11.1 million (or RMB 71.0 million). After the acquisition, Mejia became Dongguan Dogness’

wholly-owned subsidiary. The acquisition of Meijia enabled the Company to build its own facility instead of leasing manufacturing facilities

and to expand its production capacity sustainably to meet increased customer demand. Meijia plant has reached its fully production capacity

as of June 30, 2021.

On

July 6, 2018, a new entity called Dogness Intelligence Technology Co., Ltd. (“Intelligence Guangzhou”), was incorporated

under PRC laws in Guangzhou City, Guangdong Province, China with a total registered capital of RMB 80 million (approximately $11.0 million).

One of the Company’s subsidiaries, Dongguan Jiasheng, owns 58% of Intelligence, As of the date of this report, Dongguan Jiasheng

has not yet made the payment of the registered capital. Intelligence Guangzhou will be the research and manufacturing facility for the

Company’s fast growing intelligent pet products. On August 10, 2022, the Board approved to sell the Company’s 58% ownership

interest in Dogness Intelligence Technology Co., Ltd. to a third party for a price of $0.

Dogness

Pet Culture (Dongguan) Co., Ltd. (“Dogness Culture”) was incorporated on December 14, 2018 with registered capital of RMB

10 million (approximately $1.5 million). The capital was not paid and there were no active business operations. On January 15, 2020,

the Company’s subsidiary, Dongguan Dogness, entered into an agreement with one of the original shareholders of Dogness Culture,

who is related to Mr. Silong Chen, the Chief Executive Officer, to acquire 51.2% ownership interest of Dogness Culture for a nominal

fee. Dongguan Dogness thereafter contributed cash consideration of RMB 5.12 million (approximately $0.79 million) on April 16, 2020 along

with other shareholders’ capital contributions of RMB 4.88 million (approximately $0.67 million). Dogness Culture is focusing on

developing and expanding pet food market in China in the near future. On July 19, 2023, the Board approved the liquidation, dissolution,

and termination of Dogness culture following the signing of a termination agreement among Dogness’s Culture’s shareholders

on May 8, 2023. As of the date of this prospectus, Dogness Culture is in the process of being liquidated.

On

February 5, 2019, in order to expand into the Japanese market and expedite the development of new smart pet products, Dogness Japan Co.

Ltd. (“Dogness Japan”) was incorporated in Japan. The Company invested $142,000 for 51% ownership interest in Dogness Japan,

with the remaining 49% owned by an unrelated individual. Due to the negative impact of COVID-19 and because no material revenue was generated

since its inception, on November 28, 2020, the Board approved to the sale of the Company’s 51% ownership interest to the remaining

shareholder of Dogness Japan.

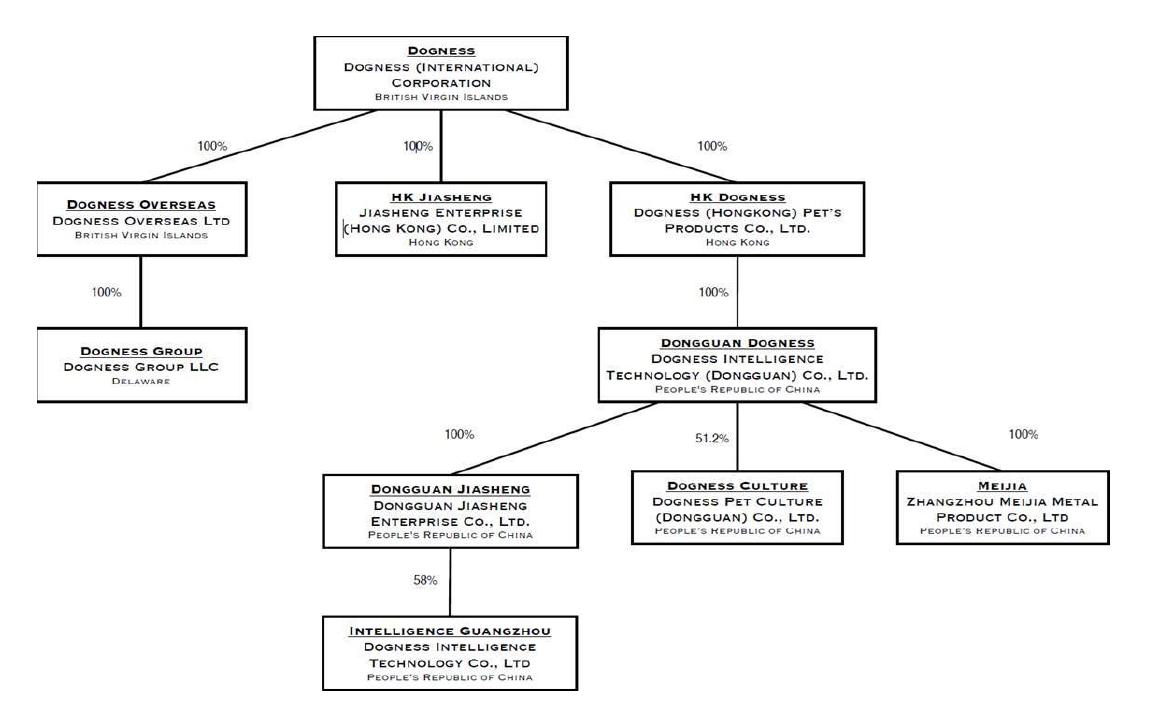

At

the completion of these transactions, (i) Dogness holds 100% of the equity of each of Dogness Overseas, HK Jiasheng and HK Dogness; (ii)

Dogness Overseas owns 100% of the equity of Dogness Group; (iii) HK Dogness holds 100% of the equity of Dongguan Dogness; (iv) Dongguan

Dogness holds 100% of the equity of Dongguan Jiasheng, Meijia and 51.2% of the equity of Dogness Culture; and (v) Dongguan Jiasheng owns

58% of the equity of Intelligence and. By virtue of these ownership relationships, Dogness is the parent, directly or indirectly, of

each of Meijia, HK Jiasheng, HK Dogness, Dongguan Dogness, Dogness Group, and Dongguan Jiasheng, and such entities’ financial results

are consolidated with those of Dogness; provided that only 58% of the equity of Intelligence Guangzhou is so consolidated.

On

November 6, 2023, Dogness ( International ) Corporation, a British Virgin Islands business company (the “Company”), announced

(i) a share consolidation of the Company’s issued and outstanding Class A Common Shares at the ratio of one-for-twenty (the “Share

Consolidation”) and (ii) an amendment of the Company’s Memorandum and Articles of Association (the “Amended and Restated

M&A”) to change its authorized shares from 90,931,000 Class A Common Shares with $0.002 par value per share and 19,069,000

Class B Common Shares with $0.002 par value per share to an unlimited number of authorized Class A Common Shares and Class B Common Shares,

each without par value. In connection with the Share Consolidation, the aggregate number of warrant shares underlying the respective

offerings of the Company which closed on July 19, 2021 (the “July 2021 Placement Agent Warrants”) and registered offering

of the Company with certain institutional investors which closed on June 3, 2022 (the “June 2022 Investors Warrants”) have

decreased from 174,249 to 8,713, and the aggregate number of warrant shares underlying the June 2022 Investors Warrants have decreased

from 2,181,820 to 109,092, respectively.

On

December 6, 2023, the Company announced that following the Company’s Share Consolidation, The Nasdaq Stock Market staff determined

that for the 10 consecutive business days, from November 7, 2023, to November 20, 2023, the closing bid price of the Company’s

Class A Common Shares had been at $1.00 per share or greater. Accordingly, the Company regained compliance with Listing Rule 5550(a)(2).

Our

Corporate Structure

| |

● |

Dogness

( International ) Corporation, a British Virgin Islands business company (“Dogness” when individually referenced), which

is the parent holding company issuing securities hereby); |

| |

|

|

| |

● |

Dogness

Overseas Ltd (“Dogness Overseas”), a British Virgin Islands business company, which is a wholly owned subsidiary of Dogness. |

| |

|

|

| |

● |

Dogness

Group LLC (“Dogness Group”), a Delaware limited company, which is a wholly owned subsidiary of Dogness Overseas; and |

| |

|

|

| |

● |

Jiasheng

Enterprise (Hongkong) Co., Limited, a Hong Kong company (“HK Jiasheng” when individually referenced), which is a wholly

owned subsidiary of Dogness; |

| |

|

|

| |

● |

Dogness

(Hongkong) Pet’s Products Co., Limited, a Hong Kong company (“HK Dogness” when individually referenced), which

is a wholly owned subsidiary of Dogness; |

| |

|

|

| |

● |

Dogness

Intelligent Technology (Dongguan) Co., Ltd., a PRC company (“Dongguan Dogness”), which is a wholly owned subsidiary of

HK Dogness; |

| |

|

|

| |

● |

Dongguan

Jiasheng Enterprise Co., Ltd., a PRC company (“Dongguan Jiasheng”), which is a wholly owned subsidiary of Dongguan Dogness; |

| |

|

|

| |

● |

Zhangzhou

Meijia Metal Product Co., Ltd, a PRC company (“Meijia”), which is a Wholly owned subsidiary of Dongguan Dogness; |

| |

|

|

| |

● |

Dogness

Intelligence Technology Co., Ltd. (“Intelligence Guangzhou”), a PRC company, and Dongguan Jiasheng owns 58% of the equity

of Intelligence Guangzhou ; and |

| |

|

|

| |

● |

Dogness

Pet Culture (Dongguan) Co., Ltd. (“Dogness Culture”), a British Virgin Islands business company, and Dongguan Dogness

owns 51.2% of the equity of Dogness Culture. |

Permission

Required from the PRC Authorities for the Company’s Operation and to Issue Our Class A Common Shares to Foreign Investors

As

of the date of this prospectus, we and our Subsidiaries have obtained all permits and licenses that are required by Chinese authorities

for our Subsidiaries to operate in China and for us to offer the securities being registered to foreign investors. Except for the potential

uncertainties disclosed below, we and our Subsidiaries have not received any requirements to obtain permissions from any PRC authorities

to operate in China or to issue our Class A Common Shares to foreign investors, and recent statements and regulatory actions by the Chinese

government indicating an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment

in China-based issuers, such as those related to anti-monopoly concerns, have not impacted the ability of Dogness or our Subsidiaries

to conduct business, accept foreign investments, or list on a U.S. or other foreign exchange.

Below

is a list of the required permits and licenses of us and our Subsidiaries in the PRC:

| |

● |

Business

Licenses |

| |

● |

Food

Distribution License |

| |

● |

Pollutant

Discharge Permit |

| |

● |

License

for the Discharge of Sewage into Drainage Pipelines |

As

of the date of this prospectus, all our Subsidiaries in the PRC have obtained the required business licenses from the State Administration

for Market Regulation for their operations, and all such licenses are currently in effect. Further, Meijia obtained a Food Distribution

License from the Zhangpu County Administration for Market Regulation on December 23, 2019, with a term of five years till December 22,

2024, for its catering services provided to its workers at the cafeteria, and a Pollutant Discharge Permit for the operation of the Meijia

plant from the Zhangpu Ecological Environment Bureau of Zhangzhou City on November 16, 2023, with a term of five years till November

15, 2028. Dongguan Jiasheng completes its filing for fixed-source pollutant on April 30, 2020, with a term for five year until April

29, 2025, and obtained a License for the Discharge of Sewage into Drainage Pipelines from the Ecological Environment Bureau of Dongguan

City on May 21, 2021, effective till May 20, 2026, for its manufacture.

Pursuant

to the Food Safety Law of the PRC and the Administrative Measures for Food Distribution Licensing, a permit is required for vendors engaging

in the sale of food and catering services. Meijia provides catering services to its workers at its cafeteria and has obtained the Food

Distribution License. In the event that Meijia could not maintain or renew such license but continues to engage in catering services,

it would be subject to the confiscation of the illegal income, the illegally distributed food, and the tools, equipment, raw materials

and other items that are used in the illegal distribution activities, as well as a fine of no less than RMB 50,000 but no more than RMB

100,000 if the illegally distributed food worth no more than RMB 10,000, or a fine of no less than ten times but no more than twenty

times of the value of the goods if such value is no less than RMB 10,000.

Pursuant

to the Environmental Protection Law of the PRC and the Regulation on the Permit Administration of Pollutant Discharge, a business operator

which is subject to the permit administration of pollutant discharge, such as Meijia, shall obtain a pollutant discharge permit. If Meijia

fails to maintain or renew such permit and continues to discharge pollutant, it would be subject to an order of rectification, restriction

on production, or suspension of production for rectification, and a fine of no less than RMB 2 million and no more than RMB 10 million;

in case of serious violation, upon the approval of the competent people’s government, it may be ordered to suspend or cease its

business. Further, pollutant discharging entities that produce and discharge a relatively small amount of pollutants or have a relatively

little impact on the environment, such as Dongguan Jiasheng, they shall be subject to a simplified management for their pollutant

discharge, and are only required to complete the filing for stationary sources of pollution. Dongguan Jiasheng has completed such

filing which is currently in effect.

Pursuant

to the Regulations on Urban Drainage and Sewage Treatment and the Administrative Measures for the Licensing of Discharge of Urban Sewage

into the Drainage Pipelines, any person or entity engaging in industry, construction, catering, medical services and other activities

(the “drainage entity”) that discharges sewage into municipal drainage facilities shall apply to the competent authority

for a license authorizing the sewage being discharged into drainage pipelines (the “Sewage Discharge License”), the violation

of which could subject the drainage entity to (i) an order to cease the illegal act and take measures to remedy within the prescribed

time, (ii) an obligation to apply for the Sewage Discharge License, and (iii) potentially, a fine of no more than RMB 500,000. Further,

if the drainage entity does not discharge sewage in accordance with the requirements specified by the Sewage Discharge License, it shall

be ordered to cease the illegal act and rectify within the prescribed time, and may be subject to a fine of no more than RMB 50,000;

in case of serious violations, its Sewage Discharge License shall be revoked, and it shall be subject to a fine of more than RMB 50,000

but less than RMB 500,000, and the public can be informed of its violations. In the event of violations that cause damages, the drainage

entity shall bear the compensation liability, and if a violation constitutes a criminal act, the drainage entity shall bear the relevant

criminal liability. Dongguan Jiasheng has obtained the Sewage Discharge License and it is currently effective.

As

of the date of this prospectus, except for the potential uncertainties disclosed below, we and our Subsidiaries have not received any

requirements to obtain permissions from any PRC authorities, including the China Securities Regulatory Commission (“CSRC”)

and the Cyberspace Administration of China (“CAC”), to operate in China or to issue our Class A Common Shares to foreign

investors. In reaching this conclusion, we relied on an opinion of our PRC counsel, and a consent from the PRC counsel has been filed

with this registration statement as Exhibit 23.4.

On

August 8, 2006, six Chinese regulatory agencies, including the Ministry of Commerce of China (“MOFCOM”), jointly issued the

Regulations on Mergers and Acquisitions of Domestic Enterprises by Foreign Investors (the “M&A Rules”), which became

effective on September 8, 2006 and amended on June 22, 2009. The M&A Rules contain provisions that require that an offshore special

purpose vehicle (“SPV”) formed for listing purposes and controlled directly or indirectly by Chinese companies or individuals

shall obtain the approval of CSRC prior to the listing and trading of such SPV’s securities on an overseas stock exchange. On September

21, 2006, CSRC published procedures specifying documents and materials required to be submitted to it by an SPV seeking CSRC approval

of overseas listings. However, the application of the M&A Rules remains unclear with no consensus currently existing among leading

Chinese law firms regarding the scope and applicability of the CSRC approval requirement. We have not chosen to voluntarily request approval

under the M&A Rules. Based on the understanding of the current PRC law, rules and regulations, given that Dogness was not established

by a merger with or an acquisition of any PRC domestic companies as defined under the M&A Rules, we believe that, as of the date

of this prospectus, CSRC’s approval under the M&A Rules is not required for the listing and trading of our Class A Common Shares

on Nasdaq in the context of this offering. However, our PRC legal counsel has advised us that there remains some uncertainty as to how

the M&A Rules will be interpreted or implemented, and our understanding summarized above is subject to any new laws, rules and regulations

or detailed implementations and interpretations in any form relating to the M&A Rules. We cannot assure you that relevant Chinese

government agencies, including the CSRC, would reach the same conclusion.

On

February 7, 2021, the Anti-Monopoly Committee of the State Council promulgated the Anti-Monopoly Guidelines for the Platform Economy

Sector, or the Anti-Monopoly Guideline, aiming to improve anti-monopoly administration on online platforms. The Anti-Monopoly Guideline,

operating as the compliance guidance under the then-existing PRC anti-monopoly regulatory regime for platform economy operators, specifically

prohibits certain acts of the platform economy operators that may have the effect of eliminating or limiting market competition, such

as concentration of undertakings. The Anti-Monopoly Guideline requires that the Ministry of Commerce, or MOC, shall be notified in advance

of any concentration of undertaking if certain thresholds are triggered. In addition, the security review rules issued by the MOC that

became effective in September, 2011 specify that mergers and acquisitions by foreign investors that raise “national defense and

security” concerns and mergers and acquisitions through which foreign investors may acquire de facto control over domestic enterprises

that raise “national security” concerns are subject to strict review by the MOC, and the rules prohibit any activities attempting

to bypass a security review, including by structuring the transaction through a proxy or contractual control arrangement. As of the date

of this prospectus, the Chinese government’s recent statements and regulatory actions related to anti-monopoly concerns have not

impacted our ability to conduct business, accept foreign investments, or list on a U.S. or other foreign exchange because neither the

Company nor our Mainland China Subsidiaries engage in monopolistic behaviors that are subject to these statements or regulatory actions.

In the future, however, we may grow our business by acquiring complementary businesses, and complying with the requirements of the above-mentioned

regulations and other relevant rules to complete such transactions could be time consuming, and any required approval processes, including

obtaining approval from the MOC or its local counterparts, may delay or inhibit our ability to complete such transactions, which could

affect our ability to expand our business or maintain our market share.

On

July 6, 2021, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council

jointly released the Opinions on Severely Cracking Down on Illegal Securities Activities According to Law, or the Opinions. The Opinions

emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over

overseas listings by Chinese companies. Effective measures, such as promoting the construction of relevant regulatory systems will be

taken to deal with the risks and incidents of China-concept overseas listed companies, and cybersecurity and data privacy protection

requirements, etc. As of the date of this prospectus, we have not received any inquiry, notice, warning, sanctions or regulatory objection

to this offering from the CSRC or other PRC governmental authorities.

On

February 17, 2023, with the approval of the State Council, China Securities Regulatory Commission (the “CSRC”) issued the

relevant system and rules for the management of overseas listing records, which has been implemented from March 31, 2023. A total of

six institutional rules (the “Listing Records Rules”) have been issued this time, including the Trial Measures for the Administration

of Overseas Issuance and Listing of Securities by Domestic Enterprises (hereinafter referred to as the “Trial Measures”)

and five supporting guidelines. Under the Listing Records Rules, a company established in mainland China seeking securities offering

and listing, by both direct or indirect means, in an overseas market is required to undertake filing procedures with the CSRC for its

overseas offering and listing activities. The Trial Measures also set forth a list of circumstance under which overseas offering and

listing by domestic companies established in mainland China is prohibit, including: (i) where such securities offering and listing is

explicitly prohibited by the PRC laws; (ii) where the intended securities offering and listing may endanger national security as reviewed

and determined by competent PRC authorities under the State Council in accordance with PRC laws; (iii) where the domestic company established

in mainland China, or its controlling shareholders and the actual controller, have committed crimes such as corruption, bribery, embezzlement,

misappropriation of property or undermining the order of the socialist market economy during the latest three (3) years; (iv) where the

domestic company established in mainland China seeking securities offering and listing is suspected of committing crimes or major violations

of laws and regulations, and is under investigation according to law, and no conclusion has yet been made thereof; and (v) where there

are material ownership disputes over equity held by the controlling shareholder of the company established in mainland China or by other

shareholders that are controlled by the controlling shareholder and/or actual controller. In accordance with the Trial Measures, the

listing and trading of our Class A Common Shares on Nasdaq is deemed as an indirect overseas offering and listing by domestic companies

established in mainland China, and thus, we are subject to the Listing Records Rules and the relevant filing procedures as required.

Further, we believe, as of the date of this prospectus, none of the circumstances prohibiting the overseas offering and listing by domestic

companies established in mainland China as listed above applies to us, and we can offer and continue to offer our Class A Common Shares

on Nasdaq.

In

accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC

along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we had been listed overseas

before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall

carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-up offerings on Nasdaq,

dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control,

investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing

status or transfer of listing segment, and voluntary or mandatory delisting. If we or our Mainland China Subsidiaries in future fail

to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of

the Trial Measures, the CSRC may order rectification, issue warnings to us and/or our Mainland China Subsidiaries, and impose a fine

of between RMB 1,000,000 yuan and RMB 10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions,

such as the SEC, via cross-border securities regulatory cooperation mechanisms. As of the date of this prospectus, we have submitted

the relevant reports regarding our private placements to certain investors to the CSRC.

Further,

on February 24, 2023, the CSRC, together with Ministry of Finance, National Administration of State Secrets Protection, and National

Archives Administration of China, released the Provisions on Strengthening the Confidentiality and Archives Administration Related to

the Overseas Securities Offering and Listing by Domestic Enterprises (the “Confidentiality Provisions”), which has come into

effect on March 31, 2023 with the Trial Measures. Under the Confidentiality Provisions, domestic companies established in mainland China

seeking overseas offering and listing, by both direct and indirect means, are required to institute a sound confidentiality and archives

system. If such domestic companies established in mainland China intend to, either directly or through its overseas listed entity, publicly

disclose or provide to relevant individuals or entities including securities companies, securities service providers and overseas regulators,

any documents and materials that contain state secrets or working secrets of government agencies, they shall obtain approval from competent

authorities and complete the relevant filing procedure with the competent secrecy administrative department prior to their disclosure

or provision of such documents and materials. Further, if they provide or publicly disclose documents and materials which may adversely

affect national security or public interests, they shall strictly follow the corresponding procedures in accordance with relevant laws

and regulations. Any failure or perceived failure by us or our subsidiaries to comply with the above confidentiality and archives administration