SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment

No. 1

to

SCHEDULE 13E-3

TRANSACTION STATEMENT UNDER SECTION 13(e) OF THE

SECURITIES EXCHANGE ACT OF 1934 AND

RULE 13e-3 THEREUNDER

Rule 13e-3 Transaction Statement

Under Section 13(e) of the Securities Exchange Act of 1934

HOLLY ENERGY PARTNERS, L.P.

(Name of the Issuer)

Holly Energy

Partners, L.P.

HF Sinclair Corporation

Navajo Pipeline Co., L.P.

Holly Apple Holdings LLC

Holly Logistic Services, L.L.C.

HEP Logistics Holdings, L.P.

(Names of Persons Filing Statement)

Common Units

(Title of

Class of Securities)

435763 10 7

(CUSIP Number of Class of Securities)

|

|

|

| Vaishali S. Bhatia

Executive Vice President, General Counsel and

Secretary HF Sinclair

Corporation 2828 N. Harwood St., Suite 1300

Dallas, Texas 75201 (214)

871-3555 |

|

Vaishali S. Bhatia

Executive Vice President, General Counsel and

Secretary Holly Energy

Partners, L.P. 2828 N. Harwood St., Suite 1300

Dallas, Texas 75201 (214)

871-3555 |

(Name, Address, and Telephone Numbers of Person Authorized to Receive Notices and Communications on Behalf of

the Persons Filing Statement)

With copies to

|

|

|

| Katherine Terrell Frank

E. Ramey Layne

Vinson & Elkins L.L.P.

Trammell Crow Center 2001

Ross Avenue, Suite 3900 Dallas, Texas 75201

(214) 220-7700 |

|

Hillary H. Holmes

Tull R. Florey Gibson,

Dunn & Crutcher LLP 811 Main Street, Suite 3000

Houston, Texas 77002

(346) 718-6600 |

This statement is filed in connection with (check the appropriate box):

|

|

|

|

|

| a. |

|

☒ |

|

The filing of solicitation materials or an information statement subject to Regulation 14A, Regulation 14C or Rule 13e-3(c) under the Securities Exchange Act of 1934. |

|

|

|

| b. |

|

☒ |

|

The filing of a registration statement under the Securities Act of 1933. |

|

|

|

| c. |

|

☐ |

|

A tender offer. |

|

|

|

| d. |

|

☐ |

|

None of the above. |

Check the following box if the soliciting materials or information statement referred to in checking box (a) are

preliminary copies: ☒

Check the following box if the filing is a final amendment reporting the results of the transaction: ☐

Neither the SEC nor any state securities regulatory agency has approved or disapproved the Merger, passed upon the merits or fairness of the Merger or

passed upon the adequacy or accuracy of the disclosure in this document. Any representation to the contrary is a criminal offense.

INTRODUCTION

This Amendment No. 1 to the Rule 13e-3 Transaction Statement on

Schedule 13E-3 (as originally filed on September 22, 2023, and together with the exhibits hereto and thereto, this “Amended Transaction Statement”), is being filed with the U.S. Securities

and Exchange Commission (the “SEC”) pursuant to Section 13(e) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), by: (i) Holly Energy Partners, L.P., a Delaware limited partnership

(“HEP”) and the issuer of the common units representing limited partner interests in HEP (“HEP Common Units,” and the holders of HEP Common Units, the “HEP Unitholders”) that are subject to the Rule 13e-3 transaction; (ii) HF Sinclair Corporation, a Delaware corporation (“HF Sinclair”); (iii) Navajo Pipeline Co., L.P., a Delaware limited partnership and an indirect wholly owned subsidiary of HF

Sinclair (“HoldCo”); (iv) Holly Logistic Services, L.L.C., a Delaware limited liability company, the general partner (the “General Partner”) of HEP Logistics Holdings, L.P. (“HLH”); (v) HLH, a Delaware limited

partnership and the general partner of HEP; and (vi) Holly Apple Holdings LLC, a wholly owned subsidiary of HoldCo (“Merger Sub”). Collectively, the persons filing this Amended Transaction Statement are referred to as the “filing

persons.”

This Amended Transaction Statement relates to the Agreement and Plan of Merger, dated as of August 15, 2023 (as the same may be

amended or supplemented from time to time, the “Merger Agreement”), by and among HF Sinclair, HEP, HoldCo, the General Partner, HLH and Merger Sub, pursuant to which Merger Sub will merge with and into HEP, with HEP surviving as an

indirect, wholly owned subsidiary of HF Sinclair (the “Merger”).

Under the terms of the Merger Agreement, at the effective time of the

Merger, each outstanding HEP Common Unit other than the HEP Common Units owned by HF Sinclair, HoldCo, HLH, the General Partner and their respective affiliates, will be converted into the right to receive (i) 0.315 (the “Exchange Ratio”)

shares of common stock, par value $0.01 per share, of HF Sinclair (the “HF Sinclair Common Stock” and such issuance, the “HF Sinclair Stock Issuance”) and (ii) $4.00 in cash, without interest (the “Cash Consideration”

and, together with the shares of HF Sinclair Common Stock to be issued in the Merger, the “Merger Consideration”). The receipt of Merger Consideration in exchange for HEP Common Units held by the HEP Unitholders other than HF Sinclair and

its subsidiaries pursuant to the Merger will be a taxable transaction to U.S. Holders. See “United States Federal Income Tax Consequences” in the Joint Proxy Statement/Prospectus (as defined below).

The Merger will become effective upon the filing of a properly executed certificate of merger with the Secretary of State of the State of Delaware or at such

later date and time as may be agreed by HF Sinclair and HEP in writing and set forth in the certificate of merger.

HF Sinclair will not issue any

fractional shares in the Merger. Instead, each holder of HEP Common Units that are converted pursuant to the Merger Agreement who otherwise would have received a fraction of a share of HF Sinclair Common Stock will be entitled to receive, in lieu

thereof, a cash payment (without interest and rounded to the nearest cent) in an amount equal to the product of (i) the aggregated amount of the fractional interest in shares of HF Sinclair Common Stock to which such holder would otherwise be

entitled to receive pursuant to the Merger Agreement and (ii) an amount equal to the average of the volume weighted average price per share of HF Sinclair Common Stock on the New York Stock Exchange (the “NYSE”) (as reported by

Bloomberg L.P., or, if not reported therein, in another authoritative source mutually selected by HF Sinclair and the General Partner) on each of the ten consecutive trading days ending with the complete trading day immediately prior to the closing

date of the Merger.

Holders of shares of HF Sinclair Common Stock prior to the Merger will continue to own their existing shares of HF Sinclair Common

Stock. In connection with the Merger, (i) HLH’s non-economic general partner interest in HEP, (ii) HLH’s special general partner interest in HEP (the “Special General Partner

Interest”), and (iii) the HEP Common Units owned by HF Sinclair and its subsidiaries, including HoldCo, will not be cancelled, will not be converted into the Merger Consideration and will remain outstanding following the Merger as a non-economic general partner interest in HEP, a Special General Partner Interest in HEP and as HEP Common Units, respectively.

The closing of the Merger will take place on the third business day after the satisfaction or waiver of the conditions set forth in the Merger Agreement

(other than conditions that by their nature are to be satisfied at the closing but subject to the satisfaction or waiver of those conditions), or at such other place, date and time as HF Sinclair and HEP may agree.

1

The conflicts committee (the “HF Sinclair Conflicts Committee”) of the board of directors of HF

Sinclair (the “HF Sinclair Board”) has unanimously (i) determined that the Merger Agreement and the various transactions contemplated by the Merger Agreement, including the Merger and the HF Sinclair Stock Issuance (the

“Transactions”), are advisable and in the best interests of HF Sinclair and the HF Sinclair Stockholders, (ii) approved the Merger Agreement and the Transactions, including the Merger and the HF Sinclair Stock Issuance, on the terms

and subject to the conditions set forth in the Merger Agreement, (iii) recommended that the HF Sinclair Board approve the Merger Agreement and the Transactions, including the Merger and the HF Sinclair Stock Issuance, on the terms and subject

to the conditions set forth in the Merger Agreement, and (iv) resolved and recommended that the HF Sinclair Board resolve, to (a) direct that the HF Sinclair Stock Issuance be submitted to a vote of the HF Sinclair Stockholders for

approval at the HF Sinclair Special Meeting and (b) recommend approval of the HF Sinclair Stock Issuance by the HF Sinclair Stockholders at the HF Sinclair Special Meeting (as defined below).

The HF Sinclair Board (acting, in part, based upon the recommendation of the HF Sinclair Conflicts Committee) has unanimously (i) determined that the

Merger Agreement and the Transactions, including the Merger and the HF Sinclair Stock Issuance, are advisable and in the best interests of HF Sinclair and the HF Sinclair Stockholders, (ii) approved the Merger Agreement and the Transactions,

including the Merger and the HF Sinclair Stock Issuance, on the terms and subject to the conditions set forth in the Merger Agreement, (iii) directed that the HF Sinclair Stock Issuance be submitted to a vote of the HF Sinclair Stockholders for

approval at the HF Sinclair Special Meeting and (iv) resolved to recommend approval of the HF Sinclair Stock Issuance by the HF Sinclair Stockholders at the HF Sinclair Special Meeting.

The conflicts committee (the “HEP Conflicts Committee”) of the board of directors of the General Partner (the “GP Board”) has unanimously

and in good faith (i) determined that the Merger Agreement and the transactions contemplated thereby, including the Merger, are in the best interests of HEP, including the HEP Unitholders other than HF Sinclair, HoldCo, HLH, the General Partner

and their respective Affiliates, including officers and directors of such entities and their Affiliates (the “HEP Unaffiliated Unitholders”), (ii) approved the Merger Agreement and the transactions contemplated thereby, including the

Merger (the foregoing constituting “Special Approval” for all purposes of the Second Amended and Restated Agreement of Limited Partnership of HEP, dated as of October 31, 2017, as may be further amended, modified or supplemented from

time to time, including Section 7.9(a) thereof) on the terms and subject to the conditions set forth in the Merger Agreement, (iii) recommended that the GP Board approve the Merger Agreement and the transactions contemplated thereby,

including the Merger, on the terms and subject to the conditions set forth in the Merger Agreement, and (iv) resolved and recommended that the GP Board resolve to (a) direct that the Merger Agreement and the Merger be submitted to a vote

of the HEP Unitholders for approval and (b) recommend approval of the Merger Agreement and the Merger by the HEP Unitholders at the HEP Special Meeting (as defined below).

The GP Board (acting, in part, based upon the recommendation of the HEP Conflicts Committee) has unanimously and in good faith (i) determined that the

Merger Agreement and the transactions contemplated thereby, including the Merger, are in the best interests of HEP, including the HEP Unaffiliated Unitholders, (ii) approved the Merger Agreement and the transactions contemplated thereby,

including the Merger, on the terms and subject to the conditions set forth in the Merger Agreement, (iii) directed that the Merger Agreement and the Merger be submitted to a vote of the HEP Unitholders for approval and (iv) resolved to

recommend approval of the Merger Agreement and the Merger by the HEP Unitholders at the HEP Special Meeting.

In connection with the Merger, HF

Sinclair will hold a special meeting of its stockholders (as the same may be adjourned or postponed, the “HF Sinclair Special Meeting”), and HEP will hold a special meeting of its unitholders (as the same may be adjourned or postponed, the

“HEP Special Meeting”).

At the HF Sinclair Special Meeting, the HF Sinclair Stockholders will be asked to consider and vote on proposals to

(i) approve the issuance of shares of HF Sinclair Common Stock to HEP Unitholders pursuant to the Merger Agreement (the “HF Sinclair Stock Issuance Proposal”) and (ii) approve the adjournment of the HF Sinclair Special Meeting to

a later date or dates, if necessary or appropriate, to solicit additional proxies in the event there are not sufficient votes at the time of the HF Sinclair Special Meeting to approve the HF Sinclair Stock Issuance Proposal. The approval by the HF

Sinclair Stockholders of the HF Sinclair Stock Issuance Proposal is required by the NYSE rules relating to issuances of securities to certain related parties.

2

At the HEP Special Meeting, the HEP Unitholders will be asked to consider and vote on proposals to

(i) approve the Merger Agreement and the transactions contemplated thereby (the “Merger Proposal”) and (ii) approve the adjournment of the HEP Special Meeting to a later date or dates, if necessary or appropriate, to solicit

additional proxies in the event there are not sufficient votes at the time of the HEP Special Meeting to approve the Merger Proposal. Pursuant to the Merger Agreement, HF Sinclair has agreed that it will vote, or cause to be voted, all HEP Common

Units then owned beneficially or of record by HF Sinclair or any of its subsidiaries in favor of the Merger Proposal. HF Sinclair currently holds approximately 47% of the issued and outstanding HEP Common Units through its subsidiaries, along with

the non-economic general partner interest and the Special General Partner Interest.

Concurrently with the

filing of this Amended Transaction Statement, HF Sinclair is filing with the SEC Amendment No. 1 to its Registration Statement on Form S-4 (Registration No. 333-274655), which includes a joint

proxy statement/prospectus of HF Sinclair and HEP (the “Joint Proxy Statement/Prospectus”) in connection with the Merger Agreement and the transactions contemplated thereby. A copy of the Joint Proxy Statement/Prospectus is attached hereto

as Exhibit (a)(1). A copy of the Merger Agreement is attached as Annex A to the Joint Proxy Statement/Prospectus. All references in this Amended Transaction Statement to Items numbered 1001 to 1016 are references to Items contained in Regulation M-A under the Exchange Act.

Pursuant to General Instruction F to Schedule

13E-3, the information contained in the Joint Proxy Statement/Prospectus, including all annexes thereto, is expressly incorporated herein by reference in its entirety and responses to each item herein are

qualified in their entirety by the information contained in the Joint Proxy Statement/Prospectus and the annexes thereto. The cross-references below are being supplied pursuant to General Instruction G to Schedule

13E-3 and show the location in the Joint Proxy Statement/Prospectus of the information required to be included in response to the items of Schedule 13E-3. As of the date hereof, the Joint Proxy

Statement/Prospectus is in preliminary form and is subject to completion. Terms used but not defined in this Amended Transaction Statement have the meanings given to them in the Joint Proxy Statement/Prospectus. As of the date hereof, the Joint

Proxy Statement/Prospectus is in preliminary form and is subject to completion or amendment.

All information concerning HEP contained in, or incorporated

by reference into, this Amended Transaction Statement was supplied by HEP. Similarly, all information concerning any other filing person contained in, or incorporated by reference into, this Amended Transaction Statement was supplied by such filing

person.

| ITEM 1. |

SUMMARY TERM SHEET |

Regulation M-A Item 1001

The information set forth in the Joint Proxy Statement/Prospectus under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Questions and Answers”

| ITEM 2. |

SUBJECT COMPANY INFORMATION |

Regulation M-A Item 1002

| (a) |

Name and Address. The information set forth in the Joint Proxy Statement/Prospectus under the following

captions is incorporated herein by reference: |

“Summary Term Sheet—The Parties”

“The Parties”

| (b) |

Securities. The information set forth in the Joint Proxy Statement/Prospectus under the following

captions is incorporated herein by reference: |

“Special Meeting of HEP Unitholders”

“Special Factors—Interests of Certain Persons in the Merger”

“Special Factors—Treatment of HEP Equity Awards”

“Comparative Market Prices and Cash Dividend/Distribution Information”

| (c) |

Trading Market and Price. The information set forth in the Joint Proxy Statement/Prospectus under the

following caption is incorporated herein by reference: |

“Comparative Market Prices and Cash

Dividend/Distribution Information”

3

| (d) |

Dividends. The information set forth in the Joint Proxy Statement/Prospectus under the following caption

is incorporated herein by reference: |

“Comparative Market Prices and Cash Dividend/Distribution

Information”

| (e) |

Prior Public Offerings. The information set forth in the Joint Proxy Statement/Prospectus under the

following caption is incorporated herein by reference: |

“Prior Public Offerings”

| (f) |

Prior Stock Purchases. The information set forth in the Joint Proxy Statement/Prospectus under the

following caption is incorporated herein by reference: |

“Comparative Market Prices and Cash

Dividend/Distribution Information”

| ITEM 3. |

IDENTITY AND BACKGROUND OF FILING PERSON |

Regulation M-A Item 1003

| (a) through (b) |

Name and Address; Business and Background of Entities. HEP is the issuer of the equity securities that

are the subject of the Rule 13e-3 transaction reported hereby. |

The information

set forth in the Joint Proxy Statement/Prospectus under the following captions is incorporated herein by reference:

“Summary Term

Sheet—The Parties”

“The Parties”

“Where You Can Find More Information”

| (c) |

Business and Background of Natural Persons. The information set forth in the Joint Proxy

Statement/Prospectus under the following captions is incorporated herein by reference: |

“Business and Background

of Natural Persons”

“Where You Can Find More Information”

| ITEM 4. |

TERMS OF THE TRANSACTION |

Regulation M-A Item 1004

| (a) |

Material Terms. The information set forth in the Joint Proxy Statement/Prospectus under the following

captions is incorporated herein by reference: |

“Summary Term Sheet”

“Questions and Answers”

“Special Factors—Overview of Special Factors”

“Special Factors—Effects of the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Resolution of Conflicts of Interest; Standards of Conduct and Modification of Duties”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

“Special Factors—Primary Benefits and Detriments of the Merger”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

4

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP

Board and the Reasons for their Recommendations”

“Special Factors—No Appraisal Rights”

“Special Factors—Listing of HF Sinclair Common Stock to be Issued in the Merger; Delisting and Deregistration of HEP Common

Units”

“Special Factors—Accounting Treatment of the Merger”

“Special Factors—Interests of Certain Persons in the Merger”

“Special Factors—Treatment of HEP Equity Awards”

“The Merger Agreement”

“Comparison of the Rights of the HF Sinclair Stockholders and the HEP Unitholders”

“Special Meeting of HF Sinclair Stockholders”

“Special Meeting of HEP Unitholders”

“United States Federal Income Tax Consequences”

“Annex A: Merger Agreement”

| (c) |

Different Terms. The information set forth in the Joint Proxy Statement/Prospectus under the following

captions is incorporated herein by reference: |

“Summary Term Sheet”

“Questions and Answers”

“Special Factors—Overview of Special Factors”

“Special Factors—Interests of Certain Persons in the Merger”

“Special Factors—Provisions for HEP Unaffiliated Unitholders”

“Special Factors—No Appraisal Rights”

“The Merger Agreement”

“Annex A: Merger Agreement”

| (d) |

Appraisal Rights. The information set forth in the Joint Proxy Statement/Prospectus under the following

captions is incorporated herein by reference: |

“Summary Term Sheet—No Appraisal Rights”

“Questions and Answers”

“Special Factors—No Appraisal Rights”

| (e) |

Provisions for Unaffiliated Security Holders. The information set forth in the Joint Proxy

Statement/Prospectus under the following caption is incorporated herein by reference: |

“Special

Factors—Provisions for HEP Unaffiliated Unitholders”

| (f) |

Eligibility for Listing or Trading. The information set forth in the Joint Proxy Statement/Prospectus

under the following captions is incorporated herein by reference: |

“Summary Term Sheet—Listing of HF

Sinclair Common Stock to be Issued in the Merger; Delisting and Deregistration of HEP Common Units”

“Special

Factors—Listing of HF Sinclair Common Stock to be Issued in the Merger; Delisting and Deregistration of HEP Common Units”

“The Merger Agreement—NYSE Listing, Delisting and Deregistration”

| ITEM 5. |

PAST CONTACTS, TRANSACTIONS, NEGOTIATIONS AND AGREEMENTS |

Regulation M-A Item 1005

| (a) |

Transactions. The information set forth in the Joint Proxy Statement/Prospectus under the following

captions is incorporated herein by reference: |

“Summary Term Sheet”

“The Parties”

5

“Special Factors—Interests of Certain Persons in the Merger”

“Past Contacts, Transactions, Negotiations and Agreements”

“Where You Can Find More Information”

| (b) through (c) |

Significant Corporate Events; Negotiations or Contacts. The information set forth in the Joint Proxy

Statement/Prospectus under the following captions is incorporated herein by reference: |

“Summary Term

Sheet”

“Special Factors—Overview of Special Factors”

“Special Factors—Background of the Merger”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their

Recommendations”

“Special Factors—Financing of the Merger”

“Special Factors—Interests of Certain Persons in the Merger”

“The Merger Agreement”

“Past Contacts, Transactions, Negotiations and Agreements”

“Annex A: Merger Agreement”

| (e) |

Agreements Involving the Subject Company’s Securities. The information set forth in the Joint Proxy

Statement/Prospectus under the following captions is incorporated herein by reference: |

“Summary Term

Sheet”

“Questions and Answers”

“Special Factors—Effects of the Merger”

“Special Factors—Interests of Certain Persons in the Merger”

“Special Factors—Treatment of HEP Equity Awards”

“The Merger Agreement”

“Comparative Market Prices and Cash Dividend/Distribution Information”

“Past Contacts, Transactions, Negotiations and Agreements”

“Where You Can Find More Information”

“Annex A: Merger Agreement”

| ITEM 6. |

PURPOSES OF THE TRANSACTION AND PLANS OR PROPOSALS. |

Regulation M-A Item 1006

| (b) |

Use of Securities Acquired. The information set forth in the Joint Proxy Statement/Prospectus under the

following captions is incorporated herein by reference: |

“Summary Term Sheet”

“Questions and Answers”

“Special Factors—Overview of Special Factors”

“Special Factors—Effects of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

“Special Factors—Primary Benefits and Detriments of the Merger”

“Special Factors—Financing of the Merger”

“Special Factors—Listing of HF Sinclair Common Stock to be Issued in the Merger; Delisting and Deregistration of HEP Common

Units”

“Special Factors—Interests of Certain Persons in the Merger”

“The Merger Agreement”

6

“Annex A: Merger Agreement”

| (c)(1) through (8) |

Plans. The information set forth in the Joint Proxy Statement/Prospectus under the following captions is

incorporated herein by reference: |

“Summary Term Sheet”

“Questions and Answers”

“Comparative Market Prices and Cash Dividend/Distribution Information”

“Special Factors—Effects of the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Primary Benefits and Detriments of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their

Recommendations”

“Special Factors—Interests of Certain Persons in the Merger”

“Special Factors—Financing of the Merger”

“Special Factors—Listing of HF Sinclair Common Stock to be Issued in the Merger; Delisting and Deregistration of HEP Common

Units”

“The Merger Agreement”

“Special Meeting of HF Sinclair Stockholders”

“Special Meeting of HEP Unitholders”

“Annex A: Merger Agreement”

| ITEM 7. |

PURPOSES, ALTERNATIVES, REASONS AND EFFECTS |

Regulation M-A Item 1013

| (a) |

Purposes. The information set forth in the Joint Proxy Statement/Prospectus under the following captions

is incorporated herein by reference: |

“Summary Term Sheet”

“Questions and Answers”

“Special Factors—Effects of the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Primary Benefits and Detriments of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their

Recommendations”

“Special Factors—Interests of Certain Persons in the Merger”

| (b) |

Alternatives. The information set forth in the Joint Proxy Statement/Prospectus under the following

captions is incorporated herein by reference: |

“Summary Term Sheet”

“Special Factors—Background of the Merger”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Primary Benefits and Detriments of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

7

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and

the HF Sinclair Board and their Reasons for the Merger”

“Special Factors—Recommendations of the HEP Conflicts

Committee and the GP Board and the Reasons for their Recommendations”

“Special Factors—Financial Advisor Discussion

Materials Provided to HF Sinclair”

“Special Factors—Opinion of the Financial Advisor to the HEP Conflicts

Committee”

“Annex B: Opinion of Intrepid Partners, LLC”

| (c) |

Reasons. The information set forth in the Joint Proxy Statement/Prospectus under the following captions

is incorporated herein by reference: |

“Summary Term Sheet”

“Questions and Answers”

“Special Factors—Effects of the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Primary Benefits and Detriments of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their

Recommendations”

“Special Factors—Financial Advisor Discussion Materials Provided to HF Sinclair”

“Special Factors—Opinion of the Financial Advisor to the HEP Conflicts Committee”

“Special Factors—Interests of Certain Persons in the Merger”

“Annex B: Opinion of Intrepid Partners, LLC”

| (d) |

Effects. The information set forth in the Joint Proxy Statement/Prospectus under the following captions

is incorporated herein by reference: |

“Summary Term Sheet”

“Questions and Answers”

“Special Factors—Effects of the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Primary Benefits and Detriments of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their

Recommendations”

“Special Factors—Interests of Certain Persons in the Merger”

“Special Factors—Financing of the Merger”

“Special Factors—Listing of HF Sinclair Common Stock to be Issued in the Merger; Delisting and Deregistration of HEP Common

Units”

“The Merger Agreement”

“United States Federal Income Tax Consequences”

“Annex A: Merger Agreement”

8

| ITEM 8. |

FAIRNESS OF THE TRANSACTION |

Regulation M-A Item 1014

| (a) through (b) |

Fairness; Factors Considered in Determining Fairness. Barclays Capital, Inc. (“Barclays”) was

not requested to, and it did not, provide to HF Sinclair or any other person any (i) opinion (whether as to the fairness of any consideration, including, without limitation, the Merger Consideration, or otherwise), (ii) valuation of HEP for the

purpose of assessing the fairness of the Merger Consideration to any person, or (iii) recommendation as to how to vote or act on any matters relating to the proposed Merger or otherwise. Barclay’s discussion materials dated August 14,

2023 should not be construed as creating any fiduciary duty on Barclays’ part to HF Sinclair or any other person and such materials are not intended to be, and do not constitute, a recommendation to HF Sinclair or any other person in respect of

the Merger, including as to how any HEP Unitholder should act or vote in respect of the Merger Proposal or as to how any HF Sinclair Stockholder should act or vote in respect of the HF Sinclair Stock Issuance Proposal. |

The information set forth in the Joint Proxy Statement/Prospectus under the following captions is incorporated herein by reference:

“Summary Term Sheet”

“Special Factors—Background of the Merger”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Primary Benefits and Detriments of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their

Recommendations”

“Special Factors—Opinion of the Financial Advisor to the HEP Conflicts Committee”

“Special Factors—Financial Advisor Discussion Materials Provided to HF Sinclair”

“Special Factors—Interests of Certain Persons in the Merger”

“Annex B: Opinion of Intrepid Partners, LLC”

| (c) |

Approval of Security Holders. The information set forth in the Joint Proxy Statement/Prospectus under

the following captions is incorporated herein by reference: |

“Questions and Answers”

“Special Factors—Primary Benefits and Detriments of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their Recommendations”

“The Merger Agreement—HEP Unitholder Approval”

“Special Meeting of HEP Unitholders”

| (d) |

Unaffiliated Representative. The information set forth in the Joint Proxy Statement/Prospectus under the

following captions is incorporated herein by reference: |

“Summary Term Sheet”

“Special Factors—Effects of the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and their Reasons for the Merger”

“Special Factors—Opinion of the Financial Advisor to the HEP Conflicts Committee”

“Special Factors—Interests of Certain Persons in the Merger”

“The Merger Agreement”

“Annex B: Opinion of Intrepid Partners, LLC”

9

| (e) |

Approval of Directors. The information set forth in the Joint Proxy Statement/Prospectus under the

following captions is incorporated herein by reference: |

“Summary Term Sheet”

“Questions and Answers”

“Special Factors—Background of the Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their Recommendations”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for

the Merger”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

| (f) |

Other Offers. Not Applicable. |

| ITEM 9. |

REPORTS, OPINIONS, APPRAISALS AND CERTAIN NEGOTIATIONS |

Regulation M-A Item 1015

| (a) through (b) |

Report, Opinion or Appraisal; Preparer and Summary of the Report, Opinion or Appraisal. The discussion

materials prepared by Barclays and provided to HF Sinclair, the HF Sinclair Conflicts Committee and the HF Sinclair Board, dated as of August 14, 2023, are set forth as Exhibit (c)(2) and incorporated herein by reference. The discussion

materials prepared by Intrepid Partners, LLC and provided to the HEP Conflicts Committee, dated as of June 1, 2023, June 26, 2023, July 13, 2023, July 14, 2023, July 24, 2023, July 27, 2023, August 2, 2023,

August 9, 2023, August 11, 2023 and August 15, 2023 are set forth as Exhibits (c)(3)(A) through (c)(3)(J) hereto and are incorporated herein by reference. |

The information set forth in the Joint Proxy Statement/Prospectus under the following captions is incorporated herein by reference:

“Summary Term Sheet—Effects of the Merger”

“Summary Term Sheet—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

“Summary Term Sheet—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

“Summary Term Sheet—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for

their Recommendations”

“Summary Term Sheet—Financial Advisor Discussion Materials Provided to HF Sinclair”

“Summary Term Sheet—Opinion of the Financial Advisor to the HEP Conflicts Committee”

“Special Factors—Effects of the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Opinion of the Financial Advisor to the HEP Conflicts Committee”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their

Recommendations”

“Special Factors—Financial Advisor Discussion Materials Provided to HF Sinclair”

“Special Factors—Fees and Expenses”

“Where You Can Find More Information”

“Annex B: Opinion of Intrepid Partners, LLC”

The written opinion of Intrepid Partners, LLC is attached to the Joint Proxy Statement/Prospectus as Annex B and is incorporated herein by

reference.

10

| (c) |

Availability of Documents. The reports, opinions or appraisals referenced in this Item 9 are filed

herewith and will be made available for inspection and copying at the principal executive offices of HF Sinclair and HEP during its regular business hours by any interested equity security holder of HEP Common Units or by any representative who has

been so designated in writing upon written request and at the expense of the requesting security holder. |

| ITEM 10. |

SOURCE AND AMOUNTS OF FUNDS OR OTHER CONSIDERATION |

Regulation M-A Item 1007

| (a) through (b),(d) |

Source of Funds; Conditions; Borrowed Funds. The information set forth in the Joint Proxy

Statement/Prospectus under the following captions is incorporated herein by reference: |

“Summary Term

Sheet—The Merger Consideration”

“Summary Term Sheet—The Merger Agreement”

“Summary Term Sheet—Fees and Expenses”

“Summary Term Sheet—Financing of the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their Recommendations”

“Special Factors—Interests of Certain Persons in the Merger”

“Special Factors—Fees and Expenses”

“Special Factors—Financing of the Merger”

| (c) |

Expenses. The information set forth in the Joint Proxy Statement/Prospectus under the following captions

is incorporated herein by reference: |

“Summary Term Sheet—Fees and Expenses”

“Summary Term Sheet—Financing of the Merger”

“Special Factors—Fees and Expenses”

“Special Factors—Financing of the Merger”

“Special Meeting of HF Sinclair Stockholders—Solicitation of Proxies”

“Special Meeting of HEP Unitholders—Solicitation of Proxies”

“The Merger Agreement—Effect of Termination; Termination Expenses”

| ITEM 11. |

INTEREST IN SECURITIES OF THE SUBJECT COMPANY |

Regulation M-A Item 1008

| (a) through (b) |

Securities Ownership; Securities Transactions. The information set forth in the Joint Proxy

Statement/Prospectus under the following captions is incorporated herein by reference: |

“Summary Term

Sheet—The Parties”

“Summary Term Sheet—The Merger”

“The Parties”

“Special Factors—Effects of the Merger”

“Special Factors—Interests of Certain Persons in the Merger”

“Special Factors—Treatment of HEP Equity Awards”

“Special Factors—Certain Beneficial Owners of HEP Common Units”

“The Merger Agreement”

“Comparative Market Prices and Cash Dividend/Distribution Information”

| ITEM 12. |

THE SOLICITATION OR RECOMMENDATION |

Regulation M-A Item 1012

| (d) |

Intent to Tender or Vote in a Going-Private Transaction. The information set forth in the Joint Proxy

Statement/Prospectus under the following captions is incorporated herein by reference: |

11

“Questions and Answers”

“Special Meeting of HEP Unitholders”

| (e) |

Recommendations of Others. The information set forth in the Joint Proxy Statement/Prospectus under the

following captions is incorporated herein by reference: |

“Summary Term Sheet”

“Questions and Answers”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Purpose and Reasons of the Parent Entities for the Merger”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their

Recommendations”

“Special Factors—Interests of Certain Persons in the Merger”

“The Merger Agreement—Conditions to Completion of the Merger”

| ITEM 13. |

FINANCIAL INFORMATION |

Regulation M-A Item 1010

| (a) |

Financial Statements. The information set forth in the Joint Proxy Statement/Prospectus under the

following captions is incorporated herein by reference: |

“Special Factors—Effects of the Merger”

“Selected Historical Consolidated Financial Data of HEP”

“Where You Can Find More Information”

HEP’s Annual Report on Form 10-K for the year ended December 31, 2022 and Quarterly Report

on Form 10-Q for the quarterly period ended June 30, 2023 are incorporated herein by reference.

| (b) |

Pro Forma Information. Not applicable. |

| ITEM 14. |

PERSONS/ASSETS, RETAINED, EMPLOYED, COMPENSATED OR USED |

Regulation M-A Item 1009

| (a) through (b) |

Solicitations or Recommendations; Employees and Corporate Assets. The information set forth in the Joint

Proxy Statement/Prospectus under the following captions is incorporated herein by reference: |

“Summary Term

Sheet”

“Questions and Answers”

“Special Factors—Background of the Merger”

“Special Factors—Position of HF Sinclair, HoldCo and Merger Sub as to the Fairness of the Merger”

“Special Factors—Recommendations of the HF Sinclair Conflicts Committee and the HF Sinclair Board and their Reasons for the

Merger”

“Special Factors—Recommendations of the HEP Conflicts Committee and the GP Board and the Reasons for their

Recommendations”

“Special Factors—Interests of Certain Persons in the Merger”

“Special Factors—Fees and Expenses”

12

| ITEM 15. |

ADDITIONAL INFORMATION |

Regulation M-A Item 1011

| (c) |

Golden Parachute Compensation. The information set forth in the Joint Proxy Statement/Prospectus under

the following caption is incorporated herein by reference. |

“Special Factors—Interests of Certain Persons

in the Merger”

“Special Factors—No Golden Parachute Compensation Payable to the HEP Named Executive Officers in

Connection with the Merger”

| (c) |

Other Material Information. The information set forth in the Joint Proxy Statement/Prospectus, including

all annexes thereto, is incorporated herein by reference. |

Regulation M-A Item 1016

|

|

|

| Exhibit No. |

|

Description |

|

|

| (a)(1) |

|

Joint Proxy Statement/Prospectus of HF Sinclair Corporation and Holly Energy Partners, L.P. (incorporated herein by reference to Amendment No. 1

to the Registration Statement on Form S-4 of HF Sinclair Corporation filed with the SEC concurrently with this Amended Transaction Statement). |

|

|

| (a)(2) |

|

Joint Letter to the Stockholders of HF Sinclair Corporation and the Unitholders of Holly Energy Partners, L.P. (incorporated herein by reference

to the Joint Proxy Statement/Prospectus). |

|

|

| (a)(4) |

|

Form of Proxy Card and Voting Instructions for the HF Sinclair Special Meeting (incorporated herein by reference to the Joint Proxy Statement/Prospectus).

|

|

|

| (a)(5) |

|

Form of Proxy Card and Voting Instructions for the HEP Special Meeting (incorporated herein by reference to the Joint Proxy Statement/Prospectus).

|

|

|

| (a)(6)* |

|

Notice of Special Meeting of Unitholders of Holly Energy Partners, L.P. (incorporated herein by reference to the Joint Proxy Statement/Prospectus).

|

|

|

| (a)(7)* |

|

Press Release of Holly Energy Partners, L.P. dated May

4, 2023 (incorporated herein by reference to Exhibit 99.1 to Holly Energy Partners, L.P.’s Current Report on Form 8-K filed with the SEC on May 4, 2023 (File No.

001-32225)). |

|

|

| (a)(8)* |

|

Press Release of HF Sinclair Corporation dated May

4, 2023 (incorporated herein by reference to Exhibit 99.1 to HF Sinclair Corporation’s Current Report on Form 8-K filed with the SEC on May 4, 2023 (File No.

001-41325)). |

|

|

| (a)(9)* |

|

Earnings Release of HF Sinclair Corporation dated May

4, 2023 (incorporated herein by reference to Exhibit 99.1 to HF Sinclair Corporation’s Current Report on Form 8-K filed with the SEC on May 4, 2023 (File No.

001-41325)). |

|

|

| (a)(10)* |

|

Communication to Employees of Holly Energy Partners, L.P. from the Chief Executive Officer and President of Holly Energy Partners, L.P., dated

May 4, 2023 (incorporated herein by reference to Holly Energy Partners, L.P.’s Communication pursuant to Rule 425 of the Securities Act filed with the SEC on May 4, 2023 (File

No. 001-32225)). |

|

|

| (a)(11)* |

|

Communication to Employees of HF Sinclair Corporation from HF Sinclair Corporation, dated May

4, 2023 (incorporated herein by reference to HF Sinclair Corporation’s Communication pursuant to Rule 425 of the Securities Act filed with the SEC on May 4, 2023 (File No. 001-32225)).

|

|

|

| (a)(12)* |

|

Excerpt of the Joint Earnings Call Transcript held on May

4, 2023 (incorporated herein by reference to Holly Energy Partners, L.P.’s Communication pursuant to Rule 425 of the Securities Act filed with the SEC on May 5, 2023 (File No. 001-32225)).

|

|

|

| (a)(13)* |

|

Letter to certain employees of Holly Energy Partners, L.P., dated August

16, 2023 (incorporated herein by reference to Exhibit 99.1 to Holly Energy Partners, L.P.’s Current Report on Form 8-K filed with the SEC on August

16, 2023 (File No. 001-32225)). |

|

|

| (a)(14)* |

|

Letter to certain employees of HF Sinclair Corporation and Holly Energy Partners, L.P., dated August

16, 2023 (incorporated herein by reference to Exhibit 99.1 to HF Sinclair Corporation’s Current Report on Form 8-K filed with the SEC on August 16, 2023 (File No.

001-41325)). |

|

|

| (a)(15)* |

|

Joint Press Release of HF Sinclair Corporation and Holly Energy Partners, L.P., dated August

16, 2023 (incorporated herein by reference to Exhibit 99.1 to HF Sinclair Corporation’s Current Report on Form 8-K filed with the SEC on August 16, 2023 (File No.

001-41325)). |

13

|

|

|

| Exhibit No. |

|

Description |

|

|

| (c)(1) |

|

Opinion of Intrepid Partners, LLC (incorporated herein by reference to Annex B of the Joint Proxy Statement/Prospectus).

|

|

|

| (c)(2)* |

|

Discussion materials prepared by Barclays Capital, Inc., dated August

14, 2023, for the Board of Directors of HF Sinclair Corporation. |

|

|

| (c)(2)(A) |

|

Discussion materials prepared by Barclays Capital, Inc., dated May 1, 2023, for the Board of Directors of HF Sinclair Corporation and the Conflicts Committee of the Board of Directors of HF Sinclair Corporation.

|

|

|

| (c)(2)(B) |

|

Discussion materials prepared by Barclays Capital, Inc., dated July 19, 2023, for the Conflicts Committee of the Board of Directors of HF Sinclair Corporation. |

|

|

| (c)(2)(C) |

|

Discussion materials prepared by Barclays Capital, Inc., dated July 21, 2023, for the Conflicts Committee of the Board of Directors of HF Sinclair Corporation. |

|

|

| (c)(2)(D) |

|

Discussion materials prepared by Barclays Capital, Inc., dated August 1, 2023, for the Conflicts Committee of the Board of Directors of HF Sinclair Corporation. |

|

|

| (c)(2)(E) |

|

Discussion materials prepared by Barclays Capital, Inc., dated August 11, 2023, for the Conflicts Committee of the Board of Directors of HF Sinclair Corporation. |

|

|

| (c)(3)(A)* |

|

Discussion materials prepared by Intrepid Partners, LLC, dated June

1, 2023, for the Conflicts Committee of the Board of Directors of Holly Logistic Services, L.L.C. |

|

|

| (c)(3)(B)* |

|

Discussion materials prepared by Intrepid Partners, LLC, dated June

26, 2023, for the Conflicts Committee of the Board of Directors of Holly Logistic Services, L.L.C. |

|

|

| (c)(3)(C)* |

|

Discussion materials prepared by Intrepid Partners, LLC, dated July

13, 2023, for the Conflicts Committee of the Board of Directors of Holly Logistic Services, L.L.C. |

|

|

| (c)(3)(D)* |

|

Discussion materials prepared by Intrepid Partners, LLC, dated July

14, 2023, for the Conflicts Committee of the Board of Directors of Holly Logistic Services, L.L.C. |

|

|

| (c)(3)(E)* |

|

Discussion materials prepared by Intrepid Partners, LLC, dated July

24, 2023, for the Conflicts Committee of the Board of Directors of Holly Logistic Services, L.L.C. |

|

|

| (c)(3)(F)* |

|

Discussion materials prepared by Intrepid Partners, LLC, dated July

27, 2023, for the Conflicts Committee of the Board of Directors of Holly Logistic Services, L.L.C. |

|

|

| (c)(3)(G)* |

|

Discussion materials prepared by Intrepid Partners, LLC, dated August

2, 2023, for the Conflicts Committee of the Board of Directors of Holly Logistic Services, L.L.C. |

|

|

| (c)(3)(H)* |

|

Discussion materials prepared by Intrepid Partners, LLC, dated August

9, 2023, for the Conflicts Committee of the Board of Directors of Holly Logistic Services, L.L.C. |

|

|

| (c)(3)(I)* |

|

Discussion materials prepared by Intrepid Partners, LLC, dated August

11, 2023, for the Conflicts Committee of the Board of Directors of Holly Logistic Services, L.L.C. |

|

|

| (c)(3)(J)* |

|

Presentation prepared by Intrepid Partners, LLC, dated August

15, 2023, for the Conflicts Committee of the Board of Directors of Holly Logistic Services, L.L.C. |

|

|

| (d)(1) |

|

Agreement and Plan of Merger, dated August 15, 2023, by and among HF Sinclair Corporation, Navajo Pipeline Co., L.P., Holly Apple Holdings

LLC, Holly Energy Partners, L.P., HEP Logistics Holdings, L.P., and Holly Logistic Services, L.L.C. (included as Annex A to the Joint Proxy Statement/Prospectus and incorporated herein by reference). |

|

|

| (d)(2)* |

|

Unitholders Agreement, dated as of August

2, 2021, by and among Holly Energy Partners, L.P., Holly Logistic Services, L.L.C., Navajo Pipeline Co., L.P., The Sinclair Companies, and the unitholders set forth on Schedule I thereto, as may be amended from time to time (incorporated herein by reference

to Exhibit 10.1 to Holly Energy Partners, L.P.’s Current Report on Form 8-K (File No. 001-32225) filed with the SEC on August 3, 2021). |

|

|

| (f)(1)* |

|

Second Amended and Restated Agreement of the Limited Partnership of Holly Energy Partners, L.P. (incorporated herein by reference

to Exhibit 3.1 to Holly Energy Partners, L.P.’s Current Report on Form 8-K (File No. 001-32225) filed with the SEC on November 1, 2017). |

|

|

| (f)(2)* |

|

Delaware Code Title 6 § 17-212. |

|

|

| (g) |

|

None. |

|

|

| 107* |

|

Filing Fee Table. |

14

SIGNATURES

After due inquiry and to the best of each of the undersigned’s knowledge and belief, each of the undersigned certifies that the

information set forth in this statement is true, complete and correct.

Dated as of October 16, 2023

|

|

|

| HF SINCLAIR CORPORATION |

|

|

| By: |

|

/s/ Atanas H. Atanasov |

| Name: |

|

Atanas H. Atanasov |

| Title: |

|

Executive Vice President and Chief Financial Officer |

|

| NAVAJO PIPELINE CO., L.P. |

|

|

| By: |

|

/s/ Atanas H. Atanasov |

| Name: |

|

Atanas H. Atanasov |

| Title: |

|

Executive Vice President and Chief Financial Officer |

|

| HOLLY APPLE HOLDINGS LLC |

|

|

| By: |

|

/s/ Atanas H. Atanasov |

| Name: |

|

Atanas H. Atanasov |

| Title: |

|

Executive Vice President and Chief Financial Officer |

|

| HOLLY ENERGY PARTNERS, L.P. |

|

|

| By: |

|

HEP LOGISTICS HOLDINGS, L.P., |

|

|

its General Partner |

|

|

| By: |

|

HOLLY LOGISTIC SERVICES, L.L.C., |

|

|

its General Partner |

|

|

| By: |

|

/s/ Michael C. Jennings |

| Name: |

|

Michael C. Jennings |

| Title: |

|

Chief Executive Officer and President |

|

| HOLLY LOGISTIC SERVICES, L.L.C. |

|

|

| By: |

|

/s/ Michael C. Jennings |

| Name: |

|

Michael C. Jennings |

| Title: |

|

Chief Executive Officer and President |

|

| HEP LOGISTICS HOLDINGS, L.P. |

|

|

| By: |

|

HOLLY LOGISTIC SERVICES, L.L.C., |

|

|

its General Partner |

|

|

| By: |

|

/s/ Michael C. Jennings |

| Name: |

|

Michael C. Jennings |

| Title: |

|

Chief Executive Officer and President |

15

Exhibit (c)(2)(A) BOARD PRESENTATION May 1, 2023 NYSE: DINO

Important Notice This presentation (this “Presentation”) was

prepared by Barclays Capital Inc. (“we” or “Barclays”), at the request of HF Sinclair Corporation (the “Company”) in the context of an evaluation of the potential acquisition by the Company of the equity interests

of Holly Energy Partners L.P. (the “Target”) not currently owned by the Company (the “Potential Transaction”). This Presentation is the intellectual property of Barclays and was prepared exclusively by Barclays in order to

assist the Company in the context of an evaluation of the Potential Transaction. The effective date of this Presentation is May 1, 2023 and it is valid only for the date specified herein. In connection with the Presentation Barclays has reviewed (a)

a comparison of the historical financial results and present financial condition of the Target and the Company with those of other companies that we deemed relevant, (b) a comparison of the financial terms of the proposed transaction with the

financial terms of certain other transactions that we deemed relevant, and (c) published estimates of independent research analysts with respect to the future financial performance and price targets of the Company and the Target. Barclays may also

have obtained information not made available by the Company, including, among other items, demographic, macroeconomic, regulatory, and market information related to the Target and its business mentioned in this Presentation from acknowledged and

reliable public sources or from sources that to Barclays’ best knowledge were considered reliable. Barclays did not conduct any independent verification of any such information or any other information received from the Company or the Target

involved in the execution of this Presentation. Barclays does not assume liability or responsibility for the precision, accuracy, or completeness of such information, nor does it express any opinion about the reliability of the information supplied

and highlights that any errors or changes in such information could significantly affect Barclays’ analysis. In addition, in preparing this Presentation, we have not conducted a physical inspection of the properties and facilities of the

Company or the Target and have not made or obtained any evaluations or appraisals of the assets or liabilities of the Company or the Target. Barclays’ work does not intend to be an audit of financial statements or any other information

supplied to us by the Company or the Target. Our work took into account the relevance of each item, and therefore assets, rights, and obligations of low relative relevance may not have been the object of detailed analysis. During the preparation of

this Presentation, Barclays has adopted as an assumption, with the express consent of the Company, the reliability, accuracy, veracity, completeness, sufficiency, and integrity of all data which was prepared or discussed, and Barclays has not made

or obtained any independent evaluation or appraisal of the assets or liabilities of the Company or the Target or their solvency and has further relied upon the assurances of the management of the Company that they are not aware of any facts or

circumstances that would make any such information inaccurate or misleading. The estimates and forecasts contained in this Presentation are inherently subject to uncertainties and various events or factors that are beyond the control of the Company

and the Target, as well as of Barclays, especially those whose occurrence depend on future and uncertain events. There is no guarantee that the estimates and projections used in this Presentation will be effectively achieved. The information herein

contained relating to the accounting and financial position of the Company, the Target and their markets, are those available as of May 1, 2023 unless otherwise stated herein. Any changes in those positions can affect the results of this

Presentation. Barclays does not assume any obligation of updating, reviewing, reaffirming or amending this Presentation, as a result of disclosure of any subsequent information after the date hereof or as result of any other subsequent event or

circumstances that may occur after the date of this Presentation. This Presentation was generated according to the economic and market conditions, among others, existing on the date of its preparation, so the conclusion presented is subject to

variations of several factors, over which Barclays does not have any control. There is no guarantee that the assumptions, estimates, forecasts, partial or total results, or conclusions used or presented in this Presentation will be effectively

reached or verified, in part or in whole. The future results of the Company and the Target may be different from the results included in the projections, and differences may be significant, as a result of several factors, including, but not limited

to, changes in the market conditions. This Presentation was prepared to assist the Company in evaluating the Target, but it does not intend to be the only reference for such evaluation, and is not in any way a guarantee in relation to the past or

future performance of the Company or the Target nor a formal appraisal, and therefore, it does not contain all the information necessary for such objective, and consequently does not represent nor constitute a proposal, solicitation, suggestion,

advice, recommendation, fairness opinion or solvency opinion by Barclays in connection with the proposed transaction referred to herein or any other transaction related to such transaction, as such decision is the sole responsibility of the Company,

and Barclays does not assume any responsibility for such decision. The Company shall make its own analysis in relation to any transaction involving the Target, and shall consult its own accounting, tax, and legal advisors before making its own

decision about such transaction. This Presentation is confidential and cannot be circulated, copied, published, reproduced or used in any form, neither can it be archived, included or referenced, in whole or in part, in any document, without the

previous written consent of Barclays. Barclays highlights that its services do not include advisory services of any nature, such as legal, tax or accounting. Barclays accepts no liability whatsoever for any losses arising from the use of this

Presentation or reliance on information contained herein. This Presentation shall be read and interpreted according to the restrictions and qualifications previously mentioned. The reader shall take into account the restrictions and characteristics

of the information sources utilized. 1

Executive Summary

Simplified Organizational Structure HF Sinclair (“DINO”)

will acquire unaffiliated units of Holly Energy Partners (“HEP”), and HEP will become an indirect, wholly owned subsidiary of DINO DINO Status Quo DINO Pro Forma DINO DINO Shareholders Shareholders HF Sinclair HF Sinclair Corporation

Corporation (DINO) (DINO) General Partner (GP) General Partner (GP) REH + Public Holly Logistics Holly Logistics Unitholders Services L.L.C. Services L.L.C. 47% 53% 100% Holly Holly Energy Energy Partners, L.P. Partners, L.P. (HEP) (HEP) $ in

millions $ in millions (1) Ownership Units $ Value Ownership Units $ Value HF Sinclair 59.6 $993 HF Sinclair 126.6 $2,109 REH Company 21.0 350 REH Company - - Pubic Unitholders 46.0 766 Pubic Unitholders - - Total 126.6 $2,109 Total 126.6 $2,109

Source: Company filing. Market data as of 4/28/2023. 1. Pro Forma $ Value assumes buy-in completed at current market price. 2

Transaction Rationale and Considerations DINO HEP ✓ Continues the

strategic imperative to integrate (Puget ✓ Potential for upfront premium creates possibility of Sound, Sinclair, HEP) immediate upside for HEP unitholders Benefits ✓ Provides flexibility in capital allocation to maximize ✓

Opportunity to participate in future growth without shareholder value reliance on 3rd party M&A and need for external funding ✓ Strong cash flow profile of combined entity would enable the company to fund growth, reduce leverage, ✓

Simplified structure provides more streamlined and/or improve shareholder returns corporate governance ✓ Synergies for interest expense✓ Larger, more diversified entity ✓ Simplifies DINO’s corporate structure and reduces

✓ Higher trading liquidity public company costs ✓ Unitholders benefit from enhanced governance rights in ✓ Simplifies and streamlines current intercompany corporate structure operations (refining units, refinery tankage),

commercial (shortfall fees, new deal structuring) and project execution ✓ Potential for DINO to receive a “step-up” and accelerated bonus depreciation to shield a portion of future taxable income at the pro forma entity ✓

No expected change to DINO credit rating O Buy-in potentially at a premium to current unit priceO Taxable transaction to HEP unitholders ConsiderationsO Loss of MLP strategic optionalityO C-corp shares received for MLP may be less

desirable for HEP investors O Potential DINO share price volatility if HEP unitholders sell DINO shares received after closeO Exposure to integrated refiner rather than midstream company O Securities law limitations on share repurchases

by DINO during pendency of transaction 3

HEP / DINO | Historical Exchange Ratio Analysis Number of DINO shares

per HEP unit “Heads-Up” Exchange Ratio (HEP / DINO) 5-Year Average 0.4435x 2-Year Average 0.4356x Current 0.3777x 1-Year Average 0.3469x Implied Premium Analysis Implied Premium / Discount to Heads-Up Historical Prices / Heads-Up

Exchange Ratio HEP DINO Exchange - 5% 10% 15% 20% 25% - 5% 10% 15% 20% 25% (1) Period ($/unit) ($/share) Ratio $16.66 $17.49 $18.33 $19.16 $19.99 $20.83 0.3777x 0.3966x 0.4155x 0.4343x 0.4532x 0.4721x Current (4/28/2023) $16.66 $44.11 0.3777x - 5.0%

10.0% 15.0% 20.0% 25.0% - 5.0% 10.0% 15.0% 20.0% 25.0% 5-Day VWAP $16.97 $44.01 0.3856x (1.8%) 3.1% 8.0% 12.9% 17.8% 22.7% (2.1%) 2.8% 7.7% 12.6% 17.5% 22.4% 10-Day VWAP $17.04 $44.40 0.3838x (2.2%) 2.6% 7.5% 12.4% 17.3% 22.2% (1.6%) 3.3% 8.2% 13.2%

18.1% 23.0% 20-Day VWAP $17.10 $45.37 0.3770x (2.6%) 2.3% 7.1% 12.0% 16.9% 21.7% 0.2% 5.2% 10.2% 15.2% 20.2% 25.2% 30-Day VWAP $17.21 $46.38 0.3711x (3.2%) 1.6% 6.5% 11.3% 16.1% 21.0% 1.8% 6.9% 11.9% 17.0% 22.1% 27.2% 60-Day VWAP $17.63 $47.94

0.3676x (5.5%) (0.8%) 4.0% 8.7% 13.4% 18.1% 2.7% 7.9% 13.0% 18.1% 23.3% 28.4% 1-Year VWAP $17.78 $51.26 0.3469x (6.3%) (1.6%) 3.1% 7.8% 12.4% 17.1% 8.9% 14.3% 19.8% 25.2% 30.7% 36.1% 2-Year VWAP $18.40 $42.25 0.4356x (9.5%) (4.9%) (0.4%) 4.1% 8.6%

13.2% (13.3%) (9.0%) (4.6%) (0.3%) 4.1% 8.4% 5-Year VWAP $19.38 $43.68 0.4435x (14.0%) (9.7%) (5.4%) (1.1%) 3.2% 7.5% (14.8%) (10.6%) (6.3%) (2.1%) 2.2% 6.4% 52-Week High $20.00 $66.19 0.3022x (16.7%) (12.5%) (8.4%) (4.2%) (0.0%) 4.1% 25.0% 31.2%

37.5% 43.7% 50.0% 56.2% Research Analyst Target $19.50 $57.00 0.3421x (14.6%) (10.3%) (6.0%) (1.7%) 2.5% 6.8% 10.4% 15.9% 21.4% 27.0% 32.5% 38.0% Source: FactSet as of 4/28/2023. 1. Calculations based on calendar days. 4 Better for HEP Better for

DINO

HEP | Relative Valuation EV / EBITDA Debt / EBITDA 2022A 2023E

2023E-2025E Debt / 2022A EBITDA 1.8% 2.5% 8.7% 3.2% 2.0% EBITDA CAGR Median: 4.0x 3.8x 6.0x Debt / 2023E EBITDA 5.4x 2023E 2024E 2025E EV / 2023E EBITDA Median: 8.9x 8.2x 8.0x 5.0x EV / 2024E EBITDA 12.0x 4.3x 4.5x 4.3x 10.5x 10.2x 10.0x EV / 2025E

EBITDA 9.6x 4.0x 10.0x 3.8x 3.5x 3.5x 3.2x 3.4x 8.5x 8.2x 8.4x 8.3x 8.1x 7.9x 8.1x 3.2x 8.1x 7.6x 7.8x 7.8x 8.0x 3.0x 6.0x 2.0x 4.0x 1.0x 2.0x 0.0x 0.0x Latest Quarterly Distribution Yield Levered FCF Yield LQA DCF 2023E Levered FCF Yield 2023E

2024E 2025E 1.9x 2.0x 1.2x 2.2x 1.6x Coverage Median: 11.7% 14.9% 15.0% 2024E Levered FCF Yield 20% 12.0% Median: 8.5% 17.0% 2025E Levered FCF Yield 16.6% 16.4% 10.0% 15.4% 15.1% 14.7% 15.0% 15.1% 15.0% 15% 8.7% 8.4% 9.0% 8.3% 12.9% 7.5% 10.8% 10.4%

10.6% 9.6% 10% 6.0% 5% 3.0% NA 0.0% 0% Source: Public filings, FactSet, and Wall Street research as of 4/28/2023. 5

DINO | Relative Valuation EV / EBITDA (EV / EBITDA) 2023E 2024E 2025E EV

/ 2023E EBITDA EV / 2024E EBITDA Median: 4.3x 5.3x 6.5x EV / 2025E EBITDA 7.6x 7.0x 7.0x 8.0x 6.6x 6.5x 6.0x 5.8x 5.7x 5.7x 5.3x 5.2x 5.1x 6.0x 4.9x 4.9x 4.6x 4.4x 4.5x 4.3x 3.8x 3.7x 3.5x 4.0x 3.0x 2.4x 1.8x 2.0x 0.0x (1) (2) Price / Parent CFPS

(Price / Parent CFPS) 2023E 2024E 2025E Price / 2023E Parent CFPS Median: 3.2x 3.4x 4.5x Price / 2024E Parent CFPS Price / 2025E Parent CFPS 7.2x 8.0x 6.2x 6.0x 5.7x 5.5x 5.4x 5.3x 6.0x 5.1x 4.7x 4.5x 4.6x 4.5x 4.4x 4.3x 4.2x 3.9x 3.7x 3.3x 3.4x

3.4x 4.0x 3.2x 3.0x 1.9x 2.0x 2.0x 0.0x (1) Consolidated Debt / 1.1x 1.7x 1.7x 3.3x 1.6x 0.8x 1.1x 0.6x (3) 2023E EBITDA Consolidated Net Debt / 2023E 0.6x 1.2x 1.0x 2.4x 1.1x 0.5x 0.7x (0.1)x (4) EBITDA Source: Company filings, FactSet, and Wall

Street research as of 4/28/2023. Reflects median Wall Street research consensus estimates. 1. PSX / DCP PF for DCP shares acquisition funded by cash and debt; assume $2bn of cash and $1.8bn of debt used to maintain investment grade credit rating;

PSX financials consolidate DCP Midstream Class A segment. 2. Adj. CFPS is adjusted to remove third-party distributions to unaffiliated MLP public unitholders. Adj. CFPS based on Adj. CFFO per share based on shares outstanding from Management

projections. Remaining peers calculated from median consensus. 3. Calculated as current Consolidated Debt / Projected Consolidated EBITDA. 4. Calculated as Consolidated Debt less Cash / Projected Consolidated EBITDA. 6

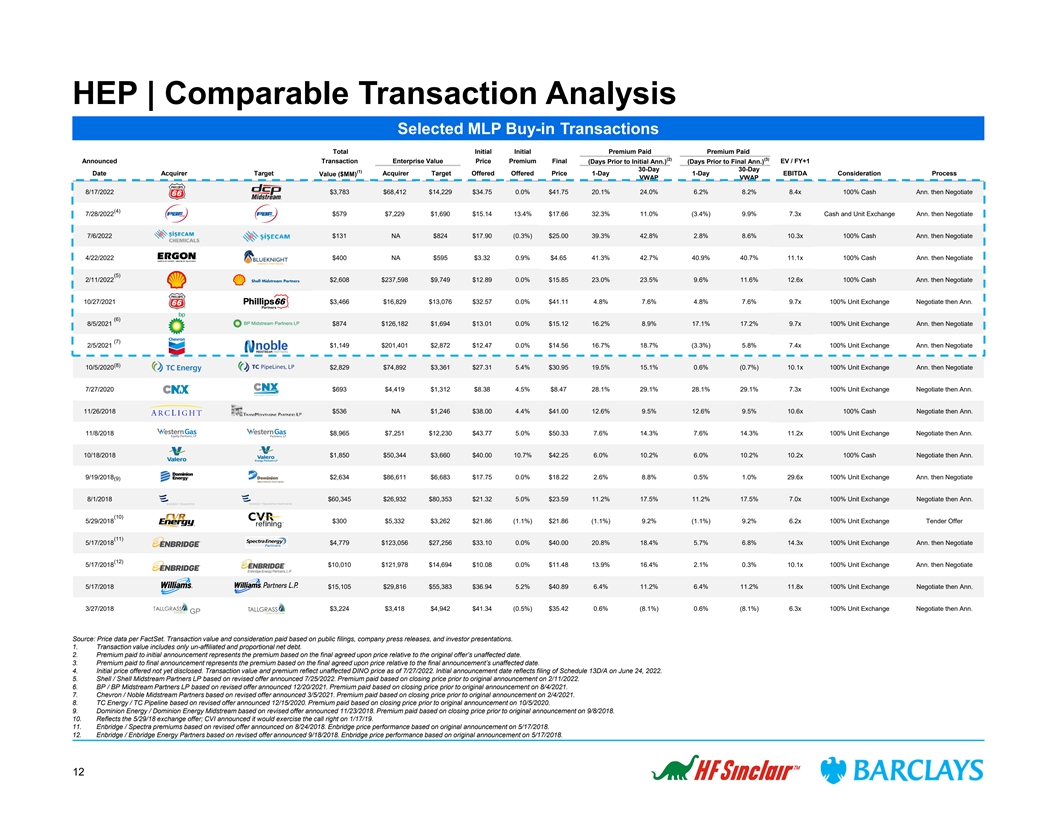

Selected Precedent Transactions Selected MLP Buy-in Transactions Total

Initial Initial Premium Paid Premium Paid - (2) (3) Announced Transaction Enterprise Value Price Premium Final (Days Prior to Initial Ann.) (Days Prior to Final Ann.) EV / FY+1 30-Day 30-Day (1) Date Acquirer Target Value ($MM) Acquirer Target

Offered Offered Price 1-Day 1-Day EBITDA Consideration Process VWAP VWAP 8/17/2022 $3,783 $68,412 $14,229 $34.75 0.0% $41.75 20.1% 24.0% 6.2% 8.2% 8.4x 100% Cash Ann. then Negotiate (4) 7/28/2022 $579 $7,229 $1,690 $15.14 13.4% $17.66 32.3% 11.0%

(3.4%) 9.9% 7.3x Cash and Unit Exchange Ann. then Negotiate 7/6/2022 $131 NA $824 $17.90 (0.3%) $25.00 39.3% 42.8% 2.8% 8.6% 10.3x 100% Cash Ann. then Negotiate 4/22/2022 $400 NA $595 $3.32 0.9% $4.65 41.3% 42.7% 40.9% 40.7% 11.1x 100% Cash Ann.

then Negotiate (5) 2/11/2022 $2,608 $237,598 $9,749 $12.89 0.0% $15.85 23.0% 23.5% 9.6% 11.6% 12.6x 100% Cash Ann. then Negotiate 10/27/2021 $3,466 $16,829 $13,076 $32.57 0.0% $41.11 4.8% 7.6% 4.8% 7.6% 9.7x 100% Unit Exchange Negotiate then Ann.

(6) 8/5/2021 $874 $126,182 $1,694 $13.01 0.0% $15.12 16.2% 8.9% 17.1% 17.2% 9.7x 100% Unit Exchange Ann. then Negotiate (7) 2/5/2021 $1,149 $201,401 $2,872 $12.47 0.0% $14.56 16.7% 18.7% (3.3%) 5.8% 7.4x 100% Unit Exchange Ann. then Negotiate (8)

10/5/2020 $2,829 $74,892 $3,361 $27.31 5.4% $30.95 19.5% 15.1% 0.6% (0.7%) 10.1x 100% Unit Exchange Ann. then Negotiate 7/27/2020 $693 $4,419 $1,312 $8.38 4.5% $8.47 28.1% 29.1% 28.1% 29.1% 7.3x 100% Unit Exchange Negotiate then Ann. 11/26/2018 $536

NA $1,246 $38.00 4.4% $41.00 12.6% 9.5% 12.6% 9.5% 10.6x 100% Cash Negotiate then Ann. 11/8/2018 $8,965 $7,251 $12,230 $43.77 5.0% $50.33 7.6% 14.3% 7.6% 14.3% 11.2x 100% Unit Exchange Negotiate then Ann. 10/18/2018 $1,850 $50,344 $3,660 $40.00

10.7% $42.25 6.0% 10.2% 6.0% 10.2% 10.2x 100% Cash Negotiate then Ann. 9/19/2018 $2,634 $86,611 $6,683 $17.75 0.0% $18.22 2.6% 8.8% 0.5% 1.0% 29.6x 100% Unit Exchange Ann. then Negotiate (9) 8/1/2018 $60,345 $26,932 $80,353 $21.32 5.0% $23.59 11.2%

17.5% 11.2% 17.5% 7.0x 100% Unit Exchange Negotiate then Ann. (10) 5/29/2018 $300 $5,332 $3,262 $21.86 (1.1%) $21.86 (1.1%) 9.2% (1.1%) 9.2% 6.2x 100% Unit Exchange Tender Offer (11) 5/17/2018 $4,779 $123,056 $27,256 $33.10 0.0% $40.00 20.8% 18.4%

5.7% 6.8% 14.3x 100% Unit Exchange Ann. then Negotiate (12) 5/17/2018 $10,010 $121,978 $14,694 $10.08 0.0% $11.48 13.9% 16.4% 2.1% 0.3% 10.1x 100% Unit Exchange Ann. then Negotiate 5/17/2018 $15,105 $29,816 $55,383 $36.94 5.2% $40.89 6.4% 11.2% 6.4%

11.2% 11.8x 100% Unit Exchange Negotiate then Ann. 3/27/2018 $3,224 $3,418 $4,942 $41.34 (0.5%) $35.42 0.6% (8.1%) 0.6% (8.1%) 6.3x 100% Unit Exchange Negotiate then Ann. Source: Price data per FactSet. Transaction value and consideration paid based

on public filings, company press releases, and investor presentations. 1. Transaction value includes only un-affiliated and proportional net debt. 2. Premium paid to initial announcement represents the premium based on the final agreed upon price

relative to the original offer’s unaffected date. 3. Premium paid to final announcement represents the premium based on the final agreed upon price relative to the final announcement’s unaffected date. 4. Initial price offered not yet

disclosed. Transaction value and premium reflect unaffected DINO price as of 7/27/2022. Initial announcement date reflects filing of Schedule 13D/A on June 24, 2022. 5. Shell / Shell Midstream Partners LP based on revised offer announced 7/25/2022.

Premium paid based on closing price prior to original announcement on 2/11/2022. 6. BP / BP Midstream Partners LP based on revised offer announced 12/20/2021. Premium paid based on closing price prior to original announcement on 8/4/2021. 7. Chevron

/ Noble Midstream Partners based on revised offer announced 3/5/2021. Premium paid based on closing price prior to original announcement on 2/4/2021. 8. TC Energy / TC Pipeline based on revised offer announced 12/15/2020. Premium paid based on

closing price prior to original announcement on 10/5/2020. 9. Dominion Energy / Dominion Energy Midstream based on revised offer announced 11/23/2018. Premium paid based on closing price prior to original announcement on 9/8/2018. 10. Reflects the

5/29/18 exchange offer; CVI announced it would exercise the call right on 1/17/19. 11. Enbridge / Spectra premiums based on revised offer announced on 8/24/2018. Enbridge price performance based on original announcement on 5/17/2018. 12. Enbridge /

Enbridge Energy Partners based on revised offer announced 9/18/2018. Enbridge price performance based on original announcement on 5/17/2018. 7

Selected Precedent Transactions (Cont’d) Selected MLP Buy-in

Transactions Total Initial Initial Premium Paid Premium Paid (2) (3) Announced Transaction Enterprise Value Price Premium Final EV / FY+1 (Days Prior to Initial Ann.) (Days Prior to Final Ann.) 30-Day 30-Day (1) Date Acquirer Target Value ($MM)

Acquirer Target Offered Offered Price 1-Day 1-Day EBITDA Consideration Process VWAP VWAP 11/8/2017 $173 $3,189 $845 $11.80 3.0% $13.92 3.0% 11.5% 3.0% 11.5% 4.6x 100% Unit Exchange Negotiate then Ann. 8/29/2017 $736 NA $736 $14.50 0.4% $16.50 15.2%

12.4% 15.2% 12.4% 12.3x 100% Cash Negotiate then Ann. 5/18/2017 $651 NA $963 $20.00 20.1% $20.00 20.1% 20.4% 20.1% 20.4% 12.3x 100% Cash Tender Offer 4/4/2017 $157 NA $594 $16.80 5.8% $17.30 5.8% 5.6% 5.8% 5.6% 9.1x 100% Cash Tender Offer 3/2/2017

$781 NA $1,470 $18.75 1.9% $19.50 6.0% 5.6% 4.3% 3.4% 9.3x 100% Cash Ann. then Negotiate 1/27/2017 $1,656 $77,129 $1,656 $6.25 (4.6%) $8.00 (8.6%) 1.8% (8.6%) 1.8% 11.0x 100% Cash Negotiate then Ann. 11/1/2016 $5,180 $77,381 $9,684 $15.75 2.9%

$17.00 11.1% 16.0% 6.3% 5.2% 18.0x 100% Cash Ann. then Negotiate Selected MLP Transactions From 2016 - 2023 YTD Mean 3.0% 13.9% 15.0% 7.5% 10.0% 10.7x Median 0.9% 12.6% 12.4% 5.8% 9.2% 10.1x High 20.1% 41.3% 42.8% 40.9% 40.7% 29.6x Low (4.6%) (8.6%)

(8.1%) (8.6%) (8.1%) 4.6x Selected 100% Stock MLP Transactions From 2016 - 2023 YTD Mean 1.9% 10.8% 12.8% 6.0% 8.8% 10.4x Median 0.0% 9.4% 12.9% 3.9% 8.4% 9.7x High 5.4% 28.1% 29.1% 28.1% 29.1% 29.6x Low (1.1%) (1.1%) (8.1%) (3.3%) (8.1%) 4.6x

Source: Price data per FactSet. Transaction value and consideration paid based on public filings, company press releases, and investor presentations. 1. Transaction value includes only un-affiliated and proportional net debt. 2. Premium paid to

initial announcement represents the premium based on the final agreed upon price relative to the original offer’s unaffected date. 8

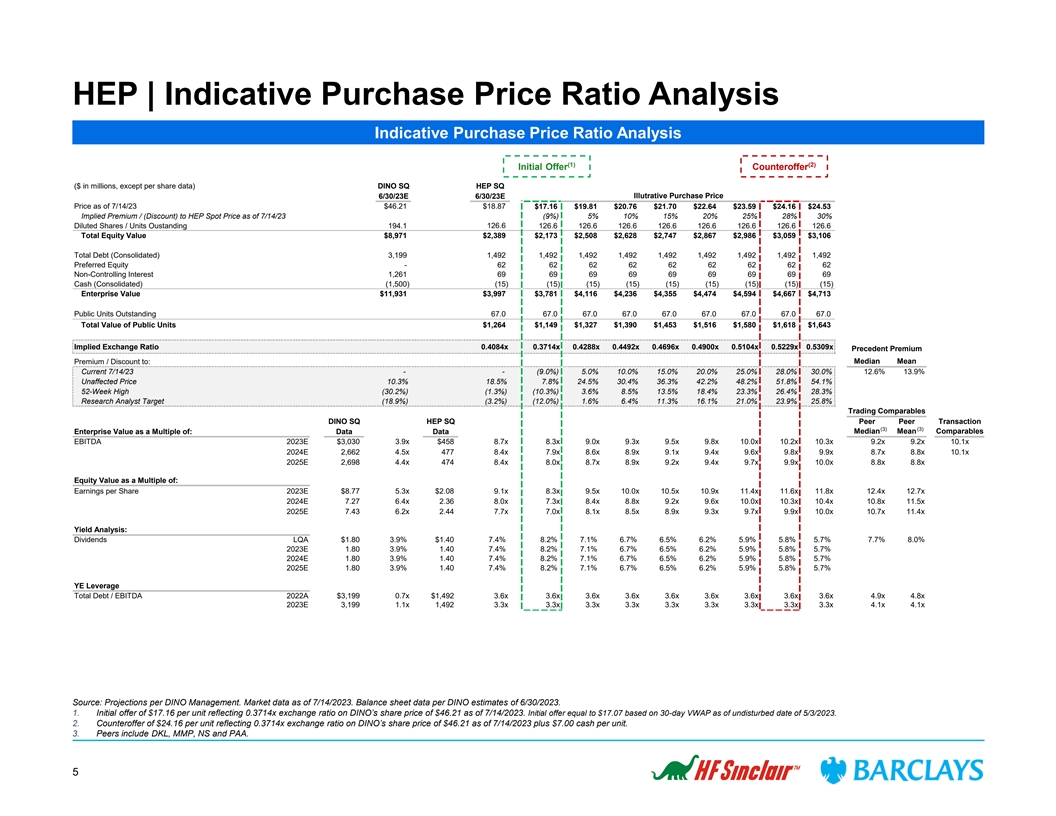

HEP | Indicative Purchase Price Ratio Analysis Indicative Purchase

Price Ratio Analysis (1) DINO SQ ($ in millions, except per share data) HEP SQ Premium to HEP 12/31/22 12/31/22 5% 10% 15% 20% 25% Price as of 4/28/23 $44.11 $16.66 $17.49 $18.33 $19.16 $19.99 $20.83 Common Shares / Units Outstanding 196.0 126.6

126.6 126.6 126.6 126.6 126.6 Total Equity Value $8,648 $2,109 $2,215 $2,320 $2,426 $2,531 $2,636 Total Debt (Consolidated) 3,276 1,568 1,568 1,568 1,568 1,568 1,568 Preferred Equity - 61 61 61 61 61 61 Non-Controlling Interest 1,113 70 70 70 70 70

70 Cash (Consolidated) (1,565) (11) (11) (11) (11) (11) (11) Enterprise Value $11,471 $3,796 $3,902 $4,007 $4,113 $4,218 $4,324 REH Owned Units 21.0 21.0 21.0 21.0 21.0 21.0 Total Value of REH Owned Units $350 $367 $385 $402 $420 $437 Public Units

Outstanding 46.0 46.0 46.0 46.0 46.0 46.0 Total Value of Public Units $766 $804 $842 $881 $919 $957 Total Value of Unaffiliated Units $1,116 $1,171 $1,227 $1,283 $1,339 $1,395 Implied Exchange Ratio 0.3777x 0.3966x 0.4155x 0.4343x 0.4532x 0.4721x

Precedent Premium Median Mean Premium / Discount to: Current (4/20/2023) - - 5.0% 10.0% 15.0% 20.0% 25.0% 12.6% 13.9% 52-Week High (33.4%) (16.7%) (12.5%) (8.4%) (4.2%) (0.0%) 4.1% Research Analyst Target (22.6%) (14.6%) (10.3%) (6.0%) (1.7%) 2.5%

6.8% Trading Comparables (1) (2) (2) DINO SQ HEP SQ Peer Peer Transaction Median Mean Comparables Enterprise Value as a Multiple of: Data Data EBITDA 2023E 3,007 3.8x $446 8.5x 8.7x 9.0x 9.2x 9.5x 9.7x 8.9x 9.1x 10.1x 2024E 2,513 4.6x 471 8.1x 8.3x

8.5x 8.7x 8.9x 9.2x 8.2x 8.6x 2025E 2,338 4.9x 463 8.2x 8.4x 8.7x 8.9x 9.1x 9.3x 8.0x 8.4x Equity Value as a Multiple of: Earnings per Share 2023E $8.32 5.3x $2.04 8.2x 8.6x 9.0x 9.4x 9.8x 10.2x 10.7x 11.3x 2024E 6.92 6.4x 2.26 7.4x 7.7x 8.1x 8.5x

8.8x 9.2x 9.6x 10.3x 2025E 5.25 8.4x 2.15 7.7x 8.1x 8.5x 8.9x 9.3x 9.7x 9.9x 10.5x Yield Analysis: Dividends LQA $1.80 4.1% $1.40 8.4% 8.0% 7.6% 7.3% 7.0% 6.7% 8.5% 8.6% 2023E 1.80 4.1% 1.55 9.3% 8.9% 8.5% 8.1% 7.8% 7.4% 2024E 1.89 4.3% 1.75 10.5%

10.0% 9.5% 9.1% 8.8% 8.4% 2025E 1.98 4.5% 1.86 11.2% 10.6% 10.1% 9.7% 9.3% 8.9% YE Leverage Total Debt / EBITDA 2022A $3,276 0.7x $1,568 3.8x 3.8x 3.8x 3.8x 3.8x 3.8x 4.0x 4.2x 2023E 3,276 1.1x 1,568 3.5x 3.5x 3.5x 3.5x 3.5x 3.5x 3.8x 3.8x Source: