0001305767falseN-2 Net asset value and market value are published in Barron's on Saturday, The Wall Street Journal on Monday and The New York Times on Monday and Saturday. Net asset value and market value are published daily on the Fund's website at www.amundi.com/us. 0001305767 2022-12-01 2023-11-30 0001305767 cik0001305767:GeneralMember 2022-12-01 2023-11-30 0001305767 cik0001305767:MarketRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:HighYieldOrjunkBondRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:CreditsRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:PrepaymentOrCallRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RiskOfIlliquidInvestmentsMember 2022-12-01 2023-11-30 0001305767 cik0001305767:PortfolioSelectionRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:ReinvestmentRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RisksOfInvestingInFloatingRateLoansMember 2022-12-01 2023-11-30 0001305767 cik0001305767:LeveragingRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:ForwardForeignCurrencyTransactionsRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:StructuredSecuritiesRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:CreditDefaultSwapRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RisksOfInvestmentInOtherFundsMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RisksOfConvertibleSecuritiesMember 2022-12-01 2023-11-30 0001305767 cik0001305767:CurrencyRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RisksOfInvestingInCollateralizedDebtObligationsMember 2022-12-01 2023-11-30 0001305767 cik0001305767:MortgagerelatedAndAssetbackedSecuritiesRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:U.s.TreasuryObligationsRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:MarketPriceOfSharesMember 2022-12-01 2023-11-30 0001305767 cik0001305767:InterestsRateRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:ExtensionRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:CollateralRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RiskOfDisadvantagedAccessToConfidentialInformationMember 2022-12-01 2023-11-30 0001305767 cik0001305767:U.s.GovernmentAgencyObligationsRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RisksOfInstrumentsThatAllowForBalloonPaymentsOrNegativeAmortizationPaymentsMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RisksOfInvestingInInsuranceLinkedSecuritiesMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RisksOfZeroCouponBondsPaymentInKindDeferredAndContingentPaymentSecuritiesMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RisksOfNonUSInvestmentsMember 2022-12-01 2023-11-30 0001305767 cik0001305767:PreferredStocksRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:DerivativesRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:CybersecurityRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RisksOfSubordinatedSecuritiesMember 2022-12-01 2023-11-30 0001305767 cik0001305767:IssuerRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:MarketSegmentRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:ValuationRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:AntitakeoverProvisionsMember 2022-12-01 2023-11-30 0001305767 cik0001305767:CashManagementRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:RepurchaseAgreementRiskMember 2022-12-01 2023-11-30 0001305767 cik0001305767:MarketValuePerShareMember 2022-12-01 2023-11-30 0001305767 cik0001305767:MarketValuePerShareMember 2023-11-30 0001305767 cik0001305767:NetAssetValuePerShareMember 2023-11-30 0001305767 cik0001305767:MarketValuePerShareMember 2022-11-30 0001305767 cik0001305767:NetAssetValuePerShareMember 2022-11-30 0001305767 cik0001305767:MarketValuePerShareMember 2021-12-01 2022-11-30 xbrli:pure iso4217:USD xbrli:shares

SECURITIES AND EXCHANGE COMMISSION

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number

811-21654

Pioneer Floating Rate Fund, Inc

(Exact name of registrant as specified in charter)

60 State Street, Boston, MA 02109

(Address of principal executive offices) (ZIP code)

Christopher J. Kelley, Amundi Asset Management, Inc.,

60 State Street, Boston, MA 02109

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617)

742-7825

Date of fiscal year end: November 30, 2023

Date of reporting period: December 1, 2022 through November 30, 2023

Form

N-CSR

is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule

30e-1

under the Investment Company Act of 1940 (17 CFR

270.30e-1). The

Commission may use the information provided on Form

N-CSR

in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form

N-CSR,

and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form

N-CSR

unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORT TO STOCKHOLDERS.

Pioneer Floating

Rate Fund, Inc.

Annual Report | November 30, 2023

visit us: www.amundi.com/us

| |

2 |

| |

11 |

| |

12 |

| |

13 |

| |

14 |

| |

41 |

| |

47 |

| |

66 |

| |

68 |

| |

69 |

| |

101 |

| |

103 |

| |

108 |

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

1

Portfolio Management Discussion | 11/30/23

In the following interview, Jonathan Sharkey discusses the factors that influenced the performance of Pioneer Floating Rate Fund, Inc. during the 12-month period ended November 30, 2023. Mr. Sharkey, a senior vice president and a portfolio manager at Amundi Asset Management US, Inc., is responsible for the day-to-day management of the Fund.

Q |

How did the Fund perform during the 12-month period ended November 30, 2023? |

A |

Pioneer Floating Rate Fund, Inc. returned 15.06% at net asset value (NAV) and 12.79% at market price during the 12-month period ended November 30, 2023, while the Fund’s benchmark, the Morningstar Loan Syndications & Trading Association Leveraged Loan Index (the Morningstar/LSTA Index), returned 11.94%. Unlike the Fund, the Morningstar/LSTA Index does not use leverage. While the use of leverage increases investment opportunity, it also increases investment risk. |

| |

During the same 12-month period, the average return at NAV of the 69 closed end funds in Morningstar’s Bank Loan Closed End Funds category (which may or may not be leveraged), was 13.53%, while the same closed end fund Morningstar category’s average return at market price was 12.88%. |

| |

The shares of the Fund were selling at a 10.90% discount to NAV on November 30, 2023. Comparatively, the shares of the Fund were selling at a 9.10% discount to NAV on November 30, 2022. |

| |

The Fund’s standardized, 30 day SEC yield was 10.45% on November 30, 2023*. |

Q |

How would you describe the environment for investing in bank loans during the 12-month period? |

A |

With inflation showing signs of modest easing, investors were anticipating a pivot by the US Federal Reserve System (Fed) to a more dovish policy stance. At the same time, the market was concerned about the potential recessionary impact of the higher fed funds target range implemented by the Fed, leading risk |

| * |

The 30-day SEC yield is a standardized formula that is based on the hypothetical annualized earning power (investment income only) of the Fund's portfolio securities during the period indicated. |

2

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

| |

assets to retreat over December 2022. The Fed implemented a more modest 50 basis point rate increase at its December meeting, leaving the fed funds target range at 4.25% to 4.50% at the end of 2022. |

| |

Entering 2023, risk assets rallied amid growing optimism that the Fed and other leading central banks were poised to stop raising interest rates. Treasury yields eased off then- recent highs in January 2023 on the prospect of easier monetary policy, boosting performance of bonds generally. In addition, the reopening of China’s economy as the government unwound its zero-Covid policy eased concerns about slowing global growth. Against this backdrop, areas of the market that had lagged during the 2022 sell-off, such as growth stocks and corporate credit outperformed. On February 1, 2023, the Fed raised its benchmark overnight lending rate by 25 basis points, to a target range of 4.50% to 4.75%. |

| |

In March 2023, the failure of two regional U.S. banks and the collapse of Credit Suisse raised fears of a financial crisis. In response, the Fed implemented a new lending program to support bank liquidity, while the market began to anticipate Fed rate cuts over the second half of 2023. The prospect of an easier monetary policy and a flight to safety spurred by the banking concerns drove Treasury yields sharply lower, supporting bond market returns. At its March 23, 2023, meeting the Fed went forward with another modest 25 basis points increase in the fed funds target to a range of 4.75%-5.0%. The increase was largely received by financial markets as an indication that the Fed believed the financial system remained sound overall. |

| |

With the unemployment rate hovering around record lows, in April 2023 the markets welcomed news of 2% first quarter growth, driven by continued consumer strength. While high inflation and the strong labor market resulted in the Fed signaling a higher terminal fed funds rate of 5.6%, markets were encouraged that the central bank was nearing the end of its hiking cycle. Corporate profits posted declines for both the first and second quarters of 2023, but investors embraced the high percentage corporate of earnings reports that came in above expectations. |

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

3

| |

Most asset classes sold off as US bond yields rose notably across September and October 2023, driven by the Fed’s “higher for longer” policy, coupled with the negative impact of higher Treasury issuance and increasing concerns about the US deficit. However, November 2023 saw longer-term Treasury yields from decrease their recent highs on weaker growth in China and Europe, declining oil prices and renewed optimism around the potential for rate cuts from the Fed. The yield on 10-year Treasury securities was 4.37% at the end of November of 2023 versus 3.68% at the end of November 2022. |

| |

Loan issuance for the 12 month period ended November 30, 2023 was well below the prior 12 months, and mostly was comprised of refinancing of existing loans, as merger and acquisition activity languished. The weak loan issuance during the 12 month period also was due to the combination of higher interest rates and recession fears, and the loan asset class actually shrunk in size over the period, bucking a trend of roughly two decades. At the same time, collateralized loan obligation (CLO) issuance during 12 month period ended November 30, 2023, although below 2022 levels, was sufficient to support demand for loans. Returns for the loan asset class were buoyed over the 12 month period by increases in the LIBOR (London Interbank Offer Rate) and SOFR (Secured Overnight Financing Rate) reference rates driven by the Fed’s rate hikes. Despite some volatility during the banking crisis during March and April 2023, the loan asset class ultimately benefited from capital appreciation as the average loan price increased while spreads tightened. As a result, loans materially outperformed both high yield and investment grade corporate bonds over the 12 months ended November 30, 2023, despite continued outflows from the asset class driven by the threat of recession. |

Q |

What factors had the biggest effects on the Fund’s performance relative to the benchmark during the 12-month period? |

A |

Overall loan selection proved beneficial to the Fund’s relative performance during the 12-month period. The Fund’s allocation across loan rating categories, which tilted toward higher quality, added to performance relative to the benchmark as well. While the Fund was underweight lower-quality loans, selection within the B- ratings category detracted from relative performance. A |

4

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

| |

slight overweight to the CCC category did not have a material impact on performance, but loan selection within the category had a negative impact on the Fund's return. |

| |

In sector terms, loan selection in commercial services & supplies helped performance, along with underweights to both media and machinery. Out-of-benchmark exposure to residential mortgage-backed securities was also beneficial. On the downside, an overweight to and selection within healthcare detracted from performance, as did selection in household products and positioning in software. Out-of-benchmark exposure to high yield corporate bonds also detracted from the Fund's performance as the asset class lagged loans. |

| |

In terms of individual positions, leading detractors from the Fund's relative performance during the 12-month period included Instant Brands, as the results for the kitchenware provider suffered from a post-COVID slump in demand along with supply chain issues, leading to the structural subordination of some company assets. The loan for ScionHealth also performed poorly, as the long-term acute care provider continued to struggle with lower volumes and higher labor costs. Within software, exposure to the loan for Loyalty Ventures detracted from the Fund's relative performance, as the customer loyalty program technology provider filed for bankruptcy. Finally, exposure to the loan for Phoenix Services weighed on performance, as the steel mill servicer filed for bankruptcy. |

| |

On the positive side, off-benchmark exposure to a credit risk transfer (CRT) mortgage-backed security proved additive to performance, as the CRT market outpaced other spread sectors, including loans, during the period. Within entertainment, the Fund’s position in AMC contributed to relative performance, as the movie theater chain raised equity to improve liquidity and reduce leverage while benefiting from improved theater attendance given a number of major movie releases. Positive selection within machinery was led by a rebound in the loan price for Novae, a trailer manufacturer which saw improved demand driven by inventory restocking. The loan to Grupo Solmax, a Canada-based manufacturer of membranes for fluid containment and transportation, performed well, as the company benefited from declining labor costs. |

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

5

| |

The Fund typically maintains modest out-of-benchmark exposure to high yield corporate bonds as part of our efforts to improve the risk/reward and liquidity profile of the Fund. The allocation to high yield corporate bonds had a negative impact on return during the 12-month period, as the category underperformed loans due to the impact of rising interest rates on fixed-income assets. Exposure to insurance-linked securities issued by insurers to mitigate the cost of paying catastrophe-related claims also detracted from the Fund's relative performance during the 12-month period, as returns for the category did not keep pace with loan performance. The Fund invests in insurance-linked securities in an effort to improve the Fund’s risk/reward profile, as performance for insurance-linked securities has typically not been correlated to underlying economic fundamentals and the asset class has historically had lower default rates than loans. |

Q |

Did the Fund have any investments in derivative securities during the 12-month period? If so, did the derivatives have any material effect on results? |

A |

The Fund had exposure to forward foreign currency exchange contracts during the period, which had a negligible effect on performance. We generate return without taking market risk through foreign currency. Instead, we typically employ forward foreign currency exchange contracts to mitigate currency risk in credit exposures that are not denominated in USD, such as the Mexican Peso. |

Q |

How did the level of leverage in the Fund change over the 12-month period ended November 30, 2023? |

A |

The Fund employs leverage through a credit agreement. (See Note 9 to the Financial Statements.) |

| |

As of November 30, 2023, 32.9% of the Fund’s total managed assets were financed by leverage (or borrowed funds), compared with 32.4% of the Fund’s total managed assets financed by leverage at the start of the 12-month period on December 1, 2022. During the 12-month period, the Fund increased the absolute amount of funds borrowed by a total of $2.5 million to $61.2 million as of November 30, 2023. The percentage of the Fund’s managed assets financed by leverage increased during the 12-month period due to the increase in the amount of funds |

6

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

| |

borrowed by the Fund. The interest rate on the Fund's leverage increased by 161 basis points during the 12-month period ended November 30, 2023. |

Q |

Did the Fund’s distributions to stockholders change during the 12-month period? |

A |

The Fund's monthly distribution rate increased from $0.0775 per share/per month, to $0.0925 per share/per month over the 12-month period. The increase in the Fund's monthly distribution rate during the period reflected increases in the SOFR reference rate during the period (interest payments under most of the loans held by the Fund are tied to the SOFR reference rate). |

Q |

What is your investment outlook? |

A |

The default rate on loans (defined here as missed interest payments) for the 12 months ended November 30, 2023 was 1.48% by loan volume versus 0.73% for the 12 months ended November 30, 2022. The default rate by number of issuers for the trailing 12 month period ended November 30, 2023 was 1.94% versus the default rate by number of issuers for the trailing 12 month period ended November 30, 2022 0.69% a year ago. The default rate for loans over the 12 months compared favorably to that for high yield corporate bonds. While recovery rates for defaulted loans have been below historical norms in recent years, they slightly improved over the 12-month period, albeit based on a small sample size. |

| |

With elevated inflation proving to be sticky and the Fed committed to bringing inflation down to its 2% long-term target, the fed funds rate is likely to drop over the next 12 months but remain higher than a year ago. If this keeps financial conditions restrictive it could continue to burden the B- loan segment, which has been saddled with low interest coverage ratios. B- loans would also be more susceptible to default if conditions become recessionary over the next year. However, we expect the Fund to remain in a relatively defensive posture, with a material underweight to B- loans. By contrast, higher quality loans should continue to perform well if a recession materializes given their higher interest coverage ratios relative to the pre-pandemic era. |

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

7

| |

As always during a recession, some borrowers will end up in trouble, leading to increased defaults. However, if there is a recession, we expect it to be modest. In our view, the economy could experience a flattening in the first half of 2024. Some firms may have utilized all their cash to cover rising interest costs, so this, coupled with flat (or potentially negative) growth, could lead to loan defaults rising above the long term rate of 3%. Nevertheless, defaults are anticipated to be lower than those experienced during the Great Financial Crisis and the COVID-19 pandemic. It is worth noting that the loan asset class continued to experience positive returns during the Great Financial Crisis and the COVID-19 pandemic, even as defaults peaked during those periods. We expect higher coupons resulting from elevated SOFR rates to more than offset default losses over the next 12 months, supporting positive returns for loans. |

| |

Any tightening of spreads in the investment grade arena could provide a positive catalyst for CLO creation and help alleviate some of the technical pressure on loan demand. With loan prices in aggregate trading below their long term average, any semblance of a soft landing could bode well for capital appreciation for the asset class. By contrast, any material widening in credit spreads could put pressure on CLOs with older stressed loans approaching maturity in 2025. |

8

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

Please refer to the Schedule of Investments on pages 14 - 40 for a full listing of Fund securities.

All investments are subject to risk, including the possible loss of principal. In the past several years, financial markets have experienced increased volatility and heightened uncertainty. The market prices of securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict including Russia's military invasion of Ukraine, sanctions against Russia, other nations or individuals or companies and possible countermeasures, or adverse investor sentiment. These conditions may continue, recur, worsen or spread.

The Fund may invest in floating-rate loans. The value of collateral, if any, securing a floating-rate loan can decline or may be insufficient to meet the issuer’s obligations or may be difficult to liquidate. No active trading market may exist for many floating rate loans, and many loans are subject to restrictions on resale. Any secondary market may be subject to irregular trading activity and extended settlement periods. There is less readily available, reliable information about most floating-rate loans than is the case for many other types of securities.

Securities with floating interest rates generally are less sensitive to interest-rate changes, but may decline in value if their interest rates do not rise as much, or as quickly, as prevailing interest rates. Unlike fixed-rate securities, floating-rate securities generally will not increase in value if interest rates decline. Changes in interest rates also will affect the amount of interest income the Fund earns on its floating-rate investments.

The Fund may use derivatives, which may include futures and options, for a variety of purposes, including: in an attempt to hedge against adverse changes in the marketplace of securities, interest rates or currency exchange rates; as a substitute for purchasing or selling securities; to attempt to increase the Fund’s return as a non-hedging strategy that may be considered speculative; and to manage portfolio characteristics. Using derivatives can increase fund losses and reduce opportunities for gains when the market prices, interest rates or the derivative instruments themselves behave in a way not anticipated by the Fund. These types of instruments can increase price fluctuation.

The Fund is not limited in the percentage of its assets that may be invested in illiquid securities. Illiquid securities may be difficult to sell at a price reflective of their value at times when the Fund believes it is desirable to do so and the market price of illiquid securities is generally more volatile than that of more liquid securities. Illiquid securities may be difficult to value, and investment of

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

9

the Fund’s assets in illiquid securities may restrict the Fund’s ability to take advantage of market opportunities.

The Fund employs leverage through a revolving credit facility. Leverage creates significant risks, including the risk that the Fund’s income or capital appreciation from investments purchased with the proceeds of leverage will not be sufficient to cover the cost of leverage, which may adversely affect the return for stockholders.

The Fund is required to maintain certain regulatory and other asset coverage requirements in connection with the Fund’s use of leverage. In order to maintain required asset coverage levels, the Fund may be required to reduce the amount of leverage employed by the Fund, alter the composition of the Fund’s investment portfolio or take other actions at what might be inopportune times in the market. Such actions could reduce the net earnings or returns to stockholders over time, which is likely to result in a decrease in the market value of the Fund’s shares.

Investments in high-yield or lower-rated securities are subject to greater-than-average risk. The Fund may invest in securities of issuers that are in default or that are in bankruptcy.

Investing in foreign and/or emerging markets securities involves risks relating to interest rates, currency exchange rates and economic and political conditions, which could increase volatility. These risks are magnified in emerging markets.

The Fund invests in insurance-linked securities (ILS). The return of principal and the payment of interest on ILS are contingent on the non-occurrence of a predefined “trigger” event, such as a hurricane or an earthquake of a specific magnitude.

These risks may increase share price volatility.

Any information in this stockholder report regarding market or economic trends or the factors influencing the Fund’s historical or future performance are statements of opinion as of the date of this report. Past performance is no guarantee of future results.

10

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

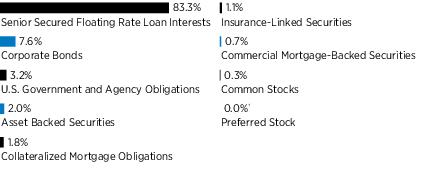

Portfolio Summary | 11/30/23

Portfolio Diversification

(As a percentage of total investments)*

| (As a percentage of total investments)* |

| 1. |

U.S. Treasury Bills, 12/19/23 |

3.26% |

| 2. |

Traverse Midstream Partners LLC, Advance, 9.24% (Term SOFR + 375 bps), 2/16/28 |

1.64 |

| 3. |

Team Health Holdings, Inc., Extended Term Loan, 10.633% (Term SOFR + 525 bps), 3/2/27 |

1.16 |

| 4. |

Upstream Newco, Inc., First Lien August 2021 Incremental Term Loan, Term Loan, 9.895% (Term SOFR + 425 bps), 11/20/26 |

1.11 |

| 5. |

Clear Channel Outdoor Holdings, Inc., Term B Loan, Term Loan, 9.145% (Term SOFR + 350 bps), 8/21/26 |

1.10 |

| 6. |

Garda World Security Corp., Term B-2 Loan, Term Loan, 9.746% (Term SOFR + 425 bps), 10/30/26 |

1.07 |

| 7. |

First Brands Group LLC, First Lien 2021 Term Loan, Term Loan, 10.881% (Term SOFR + 500 bps), 3/30/27 |

0.99 |

| 8. |

Chobani LLC., 2020 New Term Loan, Term Loan, 8.963% (Term SOFR + 350 bps), 10/25/27 |

0.93 |

| 9. |

Energy Acquisition LP, First Lien Initial Term Loan, Term Loan, 9.698% (Term SOFR + 425 bps), 6/26/25 |

0.91 |

| 10. |

Altice France S.A., USD TLB-[14] Loan, 10.894% (Term SOFR + 550 bps), 8/15/28 |

0.90 |

* Excludes short-term investments and all derivative contracts except for options purchased. The Fund is actively managed, and current holdings may be different. The holdings listed should not be considered recommendations to buy or sell any securities.

†

Amount rounds to less than 0.1%.

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

11

Prices and Distributions | 11/30/23

| |

11/30/23 |

11/30/22 |

| Market Value |

$8.99 |

$8.99 |

| Discount |

(10.90)% |

(9.10)% |

Net Asset Value per Share

^

| |

11/30/23 |

11/30/22 |

| Net Asset Value |

$10.09 |

$9.89 |

| |

Net Investment

Income |

Short-Term

Capital Gains |

Long-Term

Capital Gains |

| 12/1/22 – 11/30/23 |

$1.0725 |

$— |

$— |

| |

11/30/23 |

11/30/22 |

| 30-Day SEC Yield |

10.45% |

10.36% |

The data shown above represents past performance, which is no guarantee of future results.

^ Net asset value and market value are published in

on Saturday,

l on Monday and

on Monday and Saturday. Net asset value and market value are published daily on the Fund's website at www.amundi.com/us.

12

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

Performance Update | 11/30/23

The mountain chart on the right shows the change in market price, including reinvestment of dividends and distributions, of a $10,000 investment made in common shares of Pioneer Floating Rate Fund, Inc. during the periods shown, compared to that of the Morningstar/LSTA Leveraged Loan Index, which provides broad and comprehensive total return metrics of the U.S. universe of syndicated term loans.

Average Annual Total Return

(As of November 30, 2023) |

Period |

Net

Asset

Value

(NAV) |

Market

Price |

Morningstar/

LSTA

Leveraged

Loan Index |

| 10 Years |

4.73% |

4.07% |

4.29% |

| 5 Years |

4.71 |

5.38 |

4.91 |

| 1 Year |

15.06 |

12.79 |

11.94 |

Value of $10,000 Investment

Call 1-800-710-0935 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

Performance data shown represents past performance. Past performance is no guarantee of future results. Investment return and market price will fluctuate, and your shares may trade below NAV, due to such factors as interest rate changes, and the perceived credit quality of borrowers.

Total investment return does not reflect broker sales charges or commissions. All performance is for common shares of the Fund.

Shares of closed-end funds, unlike open-end funds, are not continuously offered. There is a one-time public offering and, once issued, shares of closed-end funds are bought and sold in the open market through a stock exchange and frequently trade at prices lower than their NAV. NAV per share is total assets less total liabilities, which include preferred shares or borrowings, as applicable, divided by the number of common shares outstanding.

When NAV is lower than market price, dividends are assumed to be reinvested at the greater of NAV or 95% of the market price. When NAV is higher, dividends are assumed to be reinvested at prices obtained through open-market purchases under the Fund’s dividend reinvestment plan.

The performance table and graph do not reflect the deduction of fees and taxes that a stockholder would pay on Fund distributions or the sale of Fund shares. Had these fees and taxes been reflected, performance would have been lower.

Index returns are calculated monthly, assume reinvestment of dividends and, unlike Fund returns, do not reflect any fees, expenses or sales charges.

The index does not use leverage.

You cannot invest directly in an index.

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

13

Schedule of Investments | 11/30/23

|

|

|

|

|

|

Value |

| |

UNAFFILIATED ISSUERS — 148.7% |

|

| |

Senior Secured Floating Rate Loan Interests — 122.3% of Net Assets(a)* |

|

| |

Advanced Materials — 1.7% |

|

| 884,174 |

Gemini HDPE LLC, 2027 Advance, 8.645% (Term SOFR + 300 bps), 12/31/27 |

$ 880,305 |

| 1,369,480 |

Groupe Solmax, Inc., Initial Term Loan, 10.402% (Term SOFR + 475 bps), 5/29/28 |

1,273,759 |

| |

Total Advanced Materials |

|

|

|

| |

Advertising Sales — 1.6% |

|

| 2,048,922 |

Clear Channel Outdoor Holdings, Inc., Term B Loan, 9.145% (Term SOFR + 350 bps), 8/21/26 |

$ 2,013,350 |

| |

Total Advertising Sales |

|

|

|

| |

Advertising Services — 1.1% |

|

| 490,000 |

Dotdash Meredith, Inc., Term Loan B, 9.42% (Term SOFR + 400 bps), 12/1/28 |

$ 477,750 |

| 980,000 |

Summer BC Bidco B LLC, USD Additional Facility B2, 10.15% (Term SOFR + 450 bps), 12/4/26 |

959,991 |

| |

Total Advertising Services |

|

|

|

| |

Aerospace & Defense — 2.9% |

|

| 831,250 |

ADS Tactical, Inc., Initial Term Loan, 11.213% (Term SOFR + 575 bps), 3/19/26 |

$ 822,937 |

| 672,942(b) |

Atlas CC Acquisition Corp., First Lien Term B Loan, 5/25/28 |

626,257 |

| 136,870(b) |

Atlas CC Acquisition Corp., First Lien Term C Loan, 5/25/28 |

127,374 |

| 497,487 |

Spirit Aerosystems, Inc., 2022 Refinancing Term Loan, 9.633% (Term SOFR + 425 bps), 1/15/27 |

498,472 |

| 1,514,942 |

WP CPP Holdings LLC, First Lien Initial Term Loan, 9.29% (Term SOFR + 375 bps), 4/30/25 |

1,498,372 |

| |

Total Aerospace & Defense |

|

|

|

| |

Airlines — 1.7% |

|

| 925,000(b) |

AAdvantage Loyality IP, Ltd. (American Airlines, Inc.), Initial Term Loan, 4/20/28 |

$ 940,754 |

| 937,500 |

Mileage Plus Holdings LLC (Mileage Plus Intellectual Property Assets, Ltd.), Initial Term Loan, 10.798% (Term SOFR + 525 bps), 6/21/27 |

967,756 |

| 272,000 |

SkyMiles IP, Ltd. (Delta Air Lines, Inc.), Initial Term Loan, 9.166% (Term SOFR + 375 bps), 10/20/27 |

278,120 |

| |

Total Airlines |

|

|

|

The accompanying notes are an integral part of these financial statements.

14

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

|

|

|

|

|

|

Value |

| |

Apparel Manufacturers — 0.8% |

|

| 961,375 |

Hanesbrands Inc., Initial Tranche B Term Loan, 9.098% (Term SOFR + 375 bps), 3/8/30 |

$ 939,744 |

| |

Total Apparel Manufacturers |

|

|

|

| |

Applications Software — 1.9% |

|

| 828,737 |

Central Parent LLC, First Lien 2023 Refinancing Term Loan, 9.406% (Term SOFR + 400 bps), 7/6/29 |

$ 830,227 |

| 544,735 |

EP Purchaser LLC, First Lien Closing Date Term Loan, 9.152% (Term SOFR + 350 bps), 11/6/28 |

535,429 |

| 872,276(c) |

Loyalty Ventures, Inc., Term B Loan, 9.96% (LIBOR + 650 bps), 11/3/27 |

8,723 |

| 996,189 |

RealPage, Inc., First Lien Initial Term Loan, 8.463% (Term SOFR + 300 bps), 4/24/28 |

973,321 |

| |

Total Applications Software |

|

|

|

| |

Athletic Equipment — 0.2% |

|

| 220,000 |

Recess Holdings, Inc., First Lien Term Loan, 9.388% (Term SOFR + 400 bps), 3/29/27 |

$ 221,100 |

| |

Total Athletic Equipment |

|

|

|

| |

Auction House & Art Dealer — 0.4% |

|

| 488,750 |

Sotheby's, 2021 Second Refinancing Term Loan, 10.155% (Term SOFR + 450 bps), 1/15/27 |

$ 477,295 |

| |

Total Auction House & Art Dealer |

|

|

|

| |

Auto Parts & Equipment — 2.8% |

|

| 412,750 |

Adient US LLC, Term B-1 Loan, 8.713% (Term SOFR + 325 bps), 4/10/28 |

$ 413,708 |

| 1,838,873 |

First Brands Group LLC, First Lien 2021 Term Loan, 10.881% (Term SOFR + 500 bps), 3/30/27 |

1,812,057 |

| 1,552,879 |

IXS Holdings, Inc., Initial Term Loan, 9.851% (Term SOFR + 425 bps), 3/5/27 |

1,321,888 |

| |

Total Auto Parts & Equipment |

|

|

|

| |

Auto-Truck Trailers — 0.8% |

|

| 985,000 |

Novae LLC, Tranche B Term Loan, 10.435% (Term SOFR + 500 bps), 12/22/28 |

$ 948,883 |

| |

Total Auto-Truck Trailers |

|

|

|

| |

Beverages — 0.5% |

|

| 164,583 |

Naked Juice LLC, First Lien Initial Term Loan, 8.74% (Term SOFR + 325 bps), 1/24/29 |

$ 154,605 |

| 496,250 |

Pegasus BidCo BV, Initial Dollar Term Loan, 9.63% (Term SOFR + 425 bps), 7/12/29 |

496,457 |

| |

Total Beverages |

|

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

15

Schedule of Investments | 11/30/23

(continued)

|

|

|

|

|

|

Value |

| |

Broadcast Service & Programing — 0.4% |

|

| 472,067 |

Univision Communications, Inc., First Lien Initial Term Loan, 8.713% (Term SOFR + 325 bps), 1/31/29 |

$ 468,674 |

| |

Total Broadcast Service & Programing |

|

|

|

| |

Building & Construction — 1.1% |

|

| 500,000 |

DG Investment Intermediate Holdings 2, Inc., Second Lien Initial Term Loan, 12.213% (Term SOFR + 675 bps), 3/30/29 |

$ 447,500 |

| 976,441 |

Service Logic Acquisition, Inc., First Lien Closing Date Initial Term Loan, 9.645% (Term SOFR + 400 bps), 10/29/27 |

977,051 |

| |

Total Building & Construction |

|

|

|

| |

Building & Construction Products — 2.3% |

|

| 1,443,940 |

Cornerstone Building Brands, Inc., Tranche B Term Loan, 8.673% (Term SOFR + 325 bps), 4/12/28 |

$ 1,413,257 |

| 561,655 |

CP Atlas Buyer, Inc., Term B Loan, 9.198% (Term SOFR + 375 bps), 11/23/27 |

530,483 |

| 446,574 |

Jeld-Wen, Inc., Replacement Term Loan, 7.713% (Term SOFR + 225 bps), 7/28/28 |

447,132 |

| 492,460 |

LHS Borrower LLC, Initial Term Loan, 10.199% (Term SOFR + 475 bps), 2/16/29 |

434,186 |

| |

Total Building & Construction Products |

|

|

|

| |

Building Production — 1.8% |

|

| 491,250 |

Chariot Buyer LLC, First Lien Initial Term Loan, 8.698% (Term SOFR + 325 bps), 11/3/28 |

$ 482,073 |

| 748,125 |

Koppers, Inc., Term Loan B, 8.93% (Term SOFR + 350 bps), 4/10/30 |

751,866 |

| 132,000(b) |

Summit Materials LLC, Incremental Term Loan B, 11/30/28 |

131,670 |

| 835,125 |

Vector WP MidCo, Inc. (Vector Canada Acquisition ULC), Initial Term B Loan, 10.463% (Term SOFR + 500 bps), 10/12/28 |

828,861 |

| |

Total Building Production |

|

|

|

| |

Building-Air & Heating — 0.3% |

|

| 333,945 |

Emerald Borrower LP, Initial Term Loan B, 8.348% (Term SOFR + 300 bps), 5/31/30 |

$ 334,541 |

| |

Total Building-Air & Heating |

|

|

|

| |

Building-Heavy Construction — 0.6% |

|

| 740,554 |

Osmose Utilities Services, Inc., First Lien Initial Term Loan, 8.713% (Term SOFR + 325 bps), 6/23/28 |

$ 733,766 |

| |

Total Building-Heavy Construction |

|

|

|

The accompanying notes are an integral part of these financial statements.

16

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

|

|

|

|

|

|

Value |

| |

Building-Maintenance & Service — 0.7% |

|

| 935,000 |

ArchKey Holdings, Inc., First Lien Initial Term Loan, 10.713% (Term SOFR + 525 bps), 6/29/28 |

$ 911,625 |

| |

Total Building-Maintenance & Service |

|

|

|

| |

Cable & Satellite Television — 3.1% |

|

| 1,922,142 |

Altice France S.A., USD TLB-[14] Loan, 10.894% (Term SOFR + 550 bps), 8/15/28 |

$ 1,648,717 |

| 498,743(b) |

CSC Holdings LLC (fka CSC Holdings, Inc. (Cablevision)), 2022 Refinancing Term Loan, 1/18/28 |

481,702 |

| 492,000 |

DIRECTV Financing LLC, Closing Date Term Loan, 10.463% (Term SOFR + 500 bps), 8/2/27 |

485,082 |

| 1,031,748 |

Radiate Holdco LLC, Amendment No. 6 Term Loan B, 8.713% (Term SOFR + 325 bps), 9/25/26 |

807,711 |

| 500,000 |

Virgin Media Bristol LLC, Facility Q, 8.687% (Term SOFR + 325 bps), 1/31/29 |

496,181 |

| |

Total Cable & Satellite Television |

|

|

|

| |

Casino Hotels — 0.8% |

|

| 992,500(b) |

Century Casinos, Inc., Term B Facility Loan, 4/2/29 |

$ 958,383 |

| |

Total Casino Hotels |

|

|

|

| |

Casino Services — 0.5% |

|

| 535,799 |

Everi Holdings, Inc., Term B Loan, 7.963% (Term SOFR + 250 bps), 8/3/28 |

$ 537,324 |

| 33,872 |

Lucky Bucks LLC, Priority First Out Exit Term Loan, 13.033% (Term SOFR + 750 bps), 10/2/28 |

32,856 |

| 67,947 |

Lucky Bucks LLC, Priority Second Out Term Loan, 13.033% (Term SOFR + 750 bps), 10/2/29 |

59,454 |

| |

Total Casino Services |

|

|

|

| |

Cellular Telecom — 1.6% |

|

| 540,302 |

CCI Buyer, Inc., First Lien Initial Term Loan, 9.39% (Term SOFR + 400 bps), 12/17/27 |

$ 537,544 |

| 842,741 |

Gogo Intermediate Holdings LLC, Initial Term Loan, 9.213% (Term SOFR + 375 bps), 4/30/28 |

844,453 |

| 735,000 |

Xplore Inc., First Lien Refinancing Term Loan, 9.652% (Term SOFR + 400 bps), 10/2/28 |

465,531 |

| 350,000 |

Xplore, Inc., Second Lien Initial Term Loan, 12.652% (Term SOFR + 700 bps), 10/1/29 |

107,990 |

| |

Total Cellular Telecom |

|

|

|

| |

Chemicals-Diversified — 2.6% |

|

| 1,000,000 |

ARC Falcon I, Inc., Second Lien Initial Term Loan, 12.449% (Term SOFR + 700 bps), 9/30/29 |

$ 895,000 |

| 439,437 |

Hexion Holdings Corp., First Lien Initial Term Loan, 10.022% (Term SOFR + 450 bps), 3/15/29 |

409,409 |

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

17

Schedule of Investments | 11/30/23

(continued)

|

|

|

|

|

|

Value |

| |

Chemicals-Diversified — (continued) |

|

| 299,250 |

Ineos US Finance LLC, 2030 Dollar Term Loan, 8.948% (Term SOFR + 350 bps), 2/18/30 |

$ 297,219 |

| 812,094 |

LSF11 A5 Holdco LLC, Fourth Amendment Incremental Term Loan, 9.698% (Term SOFR + 425 bps), 10/15/28 |

804,311 |

| 496,222 |

LSF11 A5 HoldCo LLC, Term Loan, 8.963% (Term SOFR + 350 bps), 10/15/28 |

489,399 |

| 373,125 |

Momentive Performance Materials Inc., Initial Term Loan, 9.848% (Term SOFR + 450 bps), 3/29/28 |

357,734 |

| |

Total Chemicals-Diversified |

|

|

|

| |

Chemicals-Specialty — 3.0% |

|

| 351,016 |

Avient Corp., Term B-7 Loan, 7.89% (Term SOFR + 250 bps), 8/29/29 |

$ 352,354 |

| 248,750 |

H.B. Fuller Co., Term Loan B, 7.598% (Term SOFR + 225 bps), 2/15/30 |

249,838 |

| 299,250 |

Ineos Quattro Holdings UK Limited, 2030 Tranche B Dollar Term Loan, 9.199% (Term SOFR + 375 bps), 3/14/30 |

289,898 |

| 977,500 |

Mativ Holdings, Inc., Term B Loan, 9.213% (Term SOFR + 375 bps), 4/20/28 |

967,725 |

| 399,000 |

Nouryon Finance B.V., 2023 Term Loan, 9.423% (Term SOFR + 400 bps), 4/3/28 |

396,673 |

| 448,875 |

Nouryon Finance B.V., Extended Dollar Term Loan, 9.467% (Term SOFR + 400 bps), 4/3/28 |

446,350 |

| 400,000 |

Olympus Water US Holding Corp., 2023 Incremental Term Loan, 10.39% (Term SOFR + 500 bps), 11/9/28 |

401,650 |

| 648,388 |

Olympus Water US Holding Corp., Initial Dollar Term Loan, 9.402% (Term SOFR + 375 bps), 11/9/28 |

645,065 |

| |

Total Chemicals-Specialty |

|

|

|

| |

Commercial Services — 1.3% |

|

| 430,250 |

Corporation Service Company, Initial Tranche B USD Term Loan, 8.698% (Term SOFR + 325 bps), 11/2/29 |

$ 430,788 |

| 227,230 |

Pre-Paid Legal Services, Inc., First Lien Initial Term Loan, 8.963% (Term SOFR + 350 bps), 12/15/28 |

225,752 |

| 947,139 |

Verscend Holding Corp., Term B-1 Loan, 9.463% (Term SOFR + 400 bps), 8/27/25 |

948,545 |

| |

Total Commercial Services |

|

|

|

| |

Computer Data Security — 1.1% |

|

| 1,127,000 |

Magenta Buyer LLC, First Lien Initial Term Loan, 10.645% (Term SOFR + 500 bps), 7/27/28 |

$ 726,915 |

| 609,825 |

Precisely Software, Inc., First Lien Third Amendment Term Loan, 9.64% (Term SOFR + 400 bps), 4/24/28 |

597,502 |

| |

Total Computer Data Security |

|

|

|

The accompanying notes are an integral part of these financial statements.

18

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

|

|

|

|

|

|

Value |

| |

Computer Services — 2.2% |

|

| 1,109,463 |

Ahead DB Holdings LLC, First Lien Term B Loan, 9.24% (Term SOFR + 375 bps), 10/18/27 |

$ 1,099,755 |

| 711,760 |

MAG DS Corp., Initial Term Loan, 10.99% (Term SOFR + 550 bps), 4/1/27 |

654,819 |

| 954,345 |

Peraton Corp., First Lien Term B Loan, 9.198% (Term SOFR + 375 bps), 2/1/28 |

949,573 |

| |

Total Computer Services |

|

|

|

| |

Computer Software — 2.1% |

|

| 1,231,250 |

Cornerstone OnDemand, Inc., First Lien Initial Term Loan, 9.213% (Term SOFR + 375 bps), 10/16/28 |

$ 1,189,696 |

| 988,517 |

Help/Systems Holdings, Inc., Term Loan, 9.483% (Term SOFR + 400 bps), 11/19/26 |

935,878 |

| 489,950 |

Idera, Inc., First Lien Term B-1 Loan, 9.277% (Term SOFR + 375 bps), 3/2/28 |

485,295 |

| |

Total Computer Software |

|

|

|

| |

Computers-Integrated Systems — 0.3% |

|

| 420,000 |

NCR Atleos LLC, Term Loan B, 10.198% (Term SOFR + 475 bps), 3/27/29 |

$ 412,300 |

| |

Total Computers-Integrated Systems |

|

|

|

| |

Consulting Services — 0.8% |

|

| 1,026,741 |

Ankura Consulting Group LLC, First Lien Closing Date Term Loan, 9.963% (Term SOFR + 450 bps), 3/17/28 |

$ 1,025,886 |

| |

Total Consulting Services |

|

|

|

| |

Containers-Paper & Plastic — 1.7% |

|

| 487,469 |

Charter Next Generation, Inc., First Lien 2021 Initial Term Loan, 9.213% (Term SOFR + 375 bps), 12/1/27 |

$ 486,119 |

| 185,650 |

Pactiv Evergreen, Inc., Tranche B-2 U.S. Term Loan, 8.713% (Term SOFR + 325 bps), 2/5/26 |

186,129 |

| 773,248 |

Pregis TopCo LLC, First Lien Initial Term Loan, 9.098% (Term SOFR + 375 bps), 7/31/26 |

772,282 |

| 686,438 |

Trident TPI Holdings, Inc., Tranche B-3 Initial Term Loan, 9.652% (Term SOFR + 400 bps), 9/15/28 |

672,341 |

| |

Total Containers-Paper & Plastic |

|

|

|

| |

Cruise Lines — 0.9% |

|

| 1,162,088 |

Carnival Corp., Initial Advance, 8.321% (Term SOFR + 300 bps), 8/9/27 |

$ 1,157,730 |

| |

Total Cruise Lines |

|

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

19

Schedule of Investments | 11/30/23

(continued)

|

|

|

|

|

|

Value |

| |

Diagnostic Equipment — 0.3% |

|

| 494,937 |

Curia Global, Inc., First Lien 2021 Term Loan, 9.233% (Term SOFR + 375 bps), 8/30/26 |

$ 415,128 |

| |

Total Diagnostic Equipment |

|

|

|

| |

Dialysis Centers — 1.0% |

|

| 1,715,154 |

U.S. Renal Care, Inc., Closing Date Term Loan, 10.463% (Term SOFR + 500 bps), 6/20/28 |

$ 1,243,486 |

| |

Total Dialysis Centers |

|

|

|

| |

Disposable Medical Products — 0.4% |

|

| 498,734 |

Medline Borrower LP, Initial Dollar Term Loan, 8.463% (Term SOFR + 300 bps), 10/23/28 |

$ 499,409 |

| |

Total Disposable Medical Products |

|

|

|

| |

Distribution & Wholesale — 1.2% |

|

| 498,750 |

AIP RD Buyer Corp., 2023 First Lien Incremental Term Loan, 10.349% (Term SOFR + 500 bps), 12/22/28 |

$ 497,815 |

| 591,000 |

AIP RD Buyer Corp., First Lien Term Loan B, 9.598% (Term SOFR + 425 bps), 12/22/28 |

587,306 |

| 406,250 |

Windsor Holdings III LLC, Dollar Term B Loan, 9.82% (Term SOFR + 450 bps), 8/1/30 |

407,915 |

| |

Total Distribution & Wholesale |

|

|

|

| |

E-Commerce — 0.8% |

|

| 487,500 |

CNT Holdings I Corp., First Lien Initial Term Loan, 8.926% (Term SOFR + 350 bps), 11/8/27 |

$ 488,769 |

| 495,000 |

TA TT Buyer LLC, First Lien Initial Term Loan, 10.39% (Term SOFR + 500 bps), 4/2/29 |

493,763 |

| |

Total E-Commerce |

|

|

|

| |

Electric-Generation — 2.3% |

|

| 871,414 |

Compass Power Generation LLC, Tranche B-2 Term Loan, 9.713% (Term SOFR + 425 bps), 4/14/29 |

$ 873,282 |

| 966,655(b) |

Eastern Power LLC (Eastern Covert Midco LLC), Term Loan, 10/2/25 |

951,350 |

| 219,199 |

Generation Bridge Northeast LLC, Term Loan B, 9.598% (Term SOFR + 425 bps), 8/22/29 |

220,021 |

| 802,286 |

Hamilton Projects Acquiror LLC, Term Loan, 9.963% (Term SOFR + 450 bps), 6/17/27 |

805,223 |

| |

Total Electric-Generation |

|

|

|

| |

Electric-Integrated — 2.7% |

|

| 1,087,433 |

Constellation Renewables LLC, Loan, 8.15% (Term SOFR + 250 bps), 12/15/27 |

$ 1,086,499 |

| 1,407,713 |

PG&E Corp., Term Loan, 8.463% (Term SOFR + 300 bps), 6/23/25 |

1,410,352 |

The accompanying notes are an integral part of these financial statements.

20

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

|

|

|

|

|

|

Value |

| |

Electric-Integrated — (continued) |

|

| 479,452 |

Pike Corp., 2028 Initial Term Loan, 8.463% (Term SOFR + 300 bps), 1/21/28 |

$ 479,826 |

| 262,437 |

Talen Energy Supply LLC, Initial Term Loan B, 9.869% (Term SOFR + 450 bps), 5/17/30 |

263,832 |

| 111,905 |

Talen Energy Supply LLC, Initial Term Loan C, 9.869% (Term SOFR + 450 bps), 5/17/30 |

112,499 |

| |

Total Electric-Integrated |

|

|

|

| |

Electronic Composition — 2.0% |

|

| 1,682,383 |

Energy Acquisition LP, First Lien Initial Term Loan, 9.698% (Term SOFR + 425 bps), 6/26/25 |

$ 1,665,560 |

| 1,018,983 |

Natel Engineering Co., Inc., Initial Term Loan, 11.699% (Term SOFR + 625 bps), 4/30/26 |

886,515 |

| |

Total Electronic Composition |

|

|

|

| |

Engines — 1.8% |

|

| 1,300,000 |

Arcline FM Holdings LLC, Second Lien Initial Term Loan, 13.902% (Term SOFR + 825 bps), 6/25/29 |

$ 1,241,500 |

| 1,021,000 |

LSF12 Badger Bidco LLC, Term Loan B, 11.348% (Term SOFR + 600 bps), 8/30/30 |

1,019,724 |

| |

Total Engines |

|

|

|

| |

Enterprise Software & Services — 1.8% |

|

| 248,750 |

Applied Systems, Inc., 2026 First Lien Term Loan, 9.89% (Term SOFR + 450 bps), 9/18/26 |

$ 249,883 |

| 500,000 |

First Advantage Holdings LLC, First Lien Term B-1 Loan, 8.213% (Term SOFR + 275 bps), 1/31/27 |

500,859 |

| 279,268 |

Open Text Corp., 2023 Replacement Term Loan, 8.198% (Term SOFR + 275 bps), 1/31/30 |

279,842 |

| 635,000 |

Project Alpha Intermediate Holding, Inc., Initial Term Loan, 10.093% (Term SOFR + 475 bps), 10/28/30 |

625,361 |

| 400,000 |

Quartz Acquireco LLC, Term Loan, 8.848% (Term SOFR + 350 bps), 6/28/30 |

401,000 |

| 211,306 |

Skopima Consilio Parent LLC, First Lien Initial Term Loan, 9.463% (Term SOFR + 400 bps), 5/12/28 |

208,962 |

| |

Total Enterprise Software & Services |

|

|

|

| |

Finance-Credit Card — 0.4% |

|

| 497,375 |

Blackhawk Network Holdings, Inc., First Lien Term Loan, 8.138% (Term SOFR + 275 bps), 6/15/25 |

$ 497,064 |

| |

Total Finance-Credit Card |

|

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

21

Schedule of Investments | 11/30/23

(continued)

|

|

|

|

|

|

Value |

| |

Finance-Investment Banker — 0.5% |

|

| 693,397 |

Hudson River Trading LLC, Term Loan, 8.463% (Term SOFR + 300 bps), 3/20/28 |

$ 689,443 |

| |

Total Finance-Investment Banker |

|

|

|

| |

Finance-Leasing Company — 0.7% |

|

| 415,193 |

Castlelake Aviation One Designated Activity Company, 2023 Incremental Term Loan, 8.421% (Term SOFR + 275 bps), 10/22/27 |

$ 415,600 |

| 498,242 |

Fly Funding II S.a r.l., Replacement Loan, 7.38% (LIBOR + 175 bps), 8/11/25 |

468,348 |

| |

Total Finance-Leasing Company |

|

|

|

| |

Food-Dairy Products — 1.4% |

|

| 1,697,500 |

Chobani LLC., 2020 New Term Loan, 8.963% (Term SOFR + 350 bps), 10/25/27 |

$ 1,702,009 |

| |

Total Food-Dairy Products |

|

|

|

| |

Footwear & Related Apparel — 0.3% |

|

| 375,000 |

Crocs, Inc., 2023 Refinancing Term Loan, 8.54% (Term SOFR + 300 bps), 2/20/29 |

$ 376,797 |

| |

Total Footwear & Related Apparel |

|

|

|

| |

Gambling (Non-Hotel) — 0.5% |

|

| 166,209 |

Flutter Entertainment Plc, Third Amendment 2028-B Term Loan, 8.902% (Term SOFR + 325 bps), 7/22/28 |

$ 166,645 |

| 494,987 |

Light and Wonder International, Inc., Initial Term B Loan, 8.421% (Term SOFR + 300 bps), 4/14/29 |

496,431 |

| |

Total Gambling (Non-Hotel) |

|

|

|

| |

Golf — 0.6% |

|

| 696,500 |

Topgolf Callaway Brands Corp , Intial Term Loan, 8.948% (Term SOFR + 350 bps), 3/15/30 |

$ 695,443 |

| |

Total Golf |

|

|

|

| |

Hazardous Waste Disposal — 0.6% |

|

| 720,000 |

JFL-Tiger Acquisition Co., Inc., Initial Term Loan, 10.403% (Term SOFR + 500 bps), 10/17/30 |

$ 717,000 |

| |

Total Hazardous Waste Disposal |

|

|

|

| |

Healthcare Services — 0.4% |

|

| 498,731 |

AEA International Holdings (Luxembourg) S.a.r.l., First Lien Initial Term Loan, 9.402% (Term SOFR + 375 bps), 9/7/28 |

$ 498,731 |

| |

Total Healthcare Services |

|

|

|

The accompanying notes are an integral part of these financial statements.

22

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

|

|

|

|

|

|

Value |

| |

Hotels & Motels — 1.1% |

|

| 928,993(b) |

Playa Resorts Holding B.V., 2022 Term Loan, 1/5/29 |

$ 931,149 |

| 496,250 |

Travel + Leisure Co., 2022 Incremental Term Loan, 9.655% (Term SOFR + 400 bps), 12/14/29 |

497,491 |

| |

Total Hotels & Motels |

|

|

|

| |

Human Resources — 0.7% |

|

| 975,000 |

Ingenovis Health, Inc., First Lien Initial Term Loan, 9.213% (Term SOFR + 375 bps), 3/6/28 |

$ 923,813 |

| |

Total Human Resources |

|

|

|

| |

Independent Power Producer — 0.4% |

|

| 496,869 |

EFS Cogen Holdings I LLC, Term B Advance, 9.16% (Term SOFR + 350 bps), 10/1/27 |

$ 496,426 |

| |

Total Independent Power Producer |

|

|

|

| |

Insurance Brokers — 0.3% |

|

| 380,000 |

USI, Inc. , 2023 First Funding New Term Loan, 8.64% (Term SOFR + 325 bps), 9/27/30 |

$ 380,238 |

| |

Total Insurance Brokers |

|

|

|

| |

Internet Content — 0.7% |

|

| 873,625 |

MH Sub I LLC (Micro Holding Corp.), 2023 May Incremental First Lien Term Loan, 9.598% (Term SOFR + 425 bps), 5/3/28 |

$ 847,202 |

| |

Total Internet Content |

|

|

|

| |

Investment Management & Advisory Services — 1.4% |

|

| 247,487 |

Allspring Buyer LLC, Initial Term Loan, 8.949% (Term SOFR + 325 bps), 11/1/28 |

$ 244,549 |

| 587,989 |

Edelman Financial Engines Center LLC, First Lien 2021 Initial Term Loan, 8.963% (Term SOFR + 350 bps), 4/7/28 |

583,064 |

| 992,179 |

Russell Investments US Institutional Holdco, Inc., 2025 Term Loan, 8.847% (Term SOFR + 350 bps), 5/30/25 |

933,062 |

| |

Total Investment Management & Advisory Services |

|

|

|

| |

Lottery Services — 0.6% |

|

| 792,000 |

Scientific Games Holdings LP, First Lien Initial Dollar Term Loan, 8.914% (Term SOFR + 325 bps), 4/4/29 |

$ 789,340 |

| |

Total Lottery Services |

|

|

|

| |

Medical Diagnostic Imaging — 0.6% |

|

| 829,598 |

US Radiology Specialists, Inc. (US Outpatient Imaging Services, Inc.), Closing Date Term Loan, 10.74% (Term SOFR + 525 bps), 12/15/27 |

$ 797,106 |

| |

Total Medical Diagnostic Imaging |

|

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

23

Schedule of Investments | 11/30/23

(continued)

|

|

|

|

|

|

Value |

| |

Medical Information Systems — 2.4% |

|

| 792,309 |

athenahealth Group, Inc., Initial Term Loan, 8.598% (Term SOFR + 325 bps), 2/15/29 |

$ 779,598 |

| 487,528 |

Azalea TopCo, Inc., First Lien 2021 Term Loan, 9.213% (Term SOFR + 375 bps), 7/24/26 |

474,527 |

| 939,900 |

Gainwell Acquisition Corp., First Lien Term B Loan, 9.49% (Term SOFR + 400 bps), 10/1/27 |

908,766 |

| 977,500 |

One Call Corp., First Lien Term B Loan, 11.14% (Term SOFR + 550 bps), 4/22/27 |

836,985 |

| |

Total Medical Information Systems |

|

|

|

| |

Medical Labs & Testing Services — 2.7% |

|

| 987,406 |

eResearchTechnology, Inc., First Lien Initial Term Loan, 9.963% (Term SOFR + 450 bps), 2/4/27 |

$ 974,816 |

| 1,444,162 |

FC Compassus LLC, Term B-1 Loan, 9.895% (Term SOFR + 425 bps), 12/31/26 |

1,398,582 |

| 496,183 |

Phoenix Guarantor Inc., First Lien Tranche B-3 Term Loan, 8.963% (Term SOFR + 350 bps), 3/5/26 |

495,757 |

| 500,000(b) |

U.S. Anesthesia Partners, Inc., First Lien Initial Term Loan, 10/1/28 |

449,305 |

| |

Total Medical Labs & Testing Services |

|

|

|

| |

Medical Products — 1.1% |

|

| 1,229,763 |

NMN Holdings III Corp., First Lien Closing Date Term Loan, 8.963% (Term SOFR + 350 bps), 11/13/25 |

$ 1,190,820 |

| 212,485 |

NMN Holdings III Corp., First Lien Delayed Draw Term Loan, 8.963% (Term SOFR + 350 bps), 11/13/25 |

205,757 |

| |

Total Medical Products |

|

|

|

| |

Medical-Biomedical & Generation — 0.8% |

|

| 978,530 |

ANI Pharmaceuticals, Inc., Initial Term Loan, 11.463% (Term SOFR + 600 bps), 11/19/27 |

$ 980,977 |

| |

Total Medical-Biomedical & Generation |

|

|

|

| |

Medical-Drugs — 2.1% |

|

| 1,477,992 |

Endo Luxembourg Finance Company I S.a r.l., 2021 Term Loan, 14.50% (LIBOR + 400 bps), 3/27/28 |

$ 971,779 |

| 530,000 |

Financiere Mendel, Facility B, 9.616% (Term SOFR + 425 bps), 11/12/30 |

530,000 |

| 440,363 |

Jazz Pharmaceuticals Public Limited Company, Initial Dollar Term Loan, 8.963% (Term SOFR + 350 bps), 5/5/28 |

441,709 |

| 705,882 |

Padagis LLC, Term B Loan, 10.434% (Term SOFR + 475 bps), 7/6/28 |

665,294 |

| |

Total Medical-Drugs |

|

|

|

The accompanying notes are an integral part of these financial statements.

24

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

|

|

|

|

|

|

Value |

| |

Medical-Generic Drugs — 0.7% |

|

| 425,000 |

Amneal Pharmaceuticals LLC, Initial Term Loan, 10.822% (Term SOFR + 550 bps), 5/4/28 |

$ 405,875 |

| 500,000 |

Perrigo Company Plc, Initial Term B Loan, 7.698% (Term SOFR + 225 bps), 4/20/29 |

499,375 |

| |

Total Medical-Generic Drugs |

|

|

|

| |

Medical-Hospitals — 1.5% |

|

| 982,500 |

Knight Health Holdings LLC, Term B Loan, 10.713% (Term SOFR + 525 bps), 12/23/28 |

$ 280,012 |

| 1,415,324 |

Quorum Health Corp., Exit Term Loan, 13.756% (Term SOFR + 825 bps), 4/29/25 |

884,577 |

| 488,750 |

Sound Inpatient Physicians, Inc., First Lien 2021 Incremental Term Loan, 8.645% (Term SOFR + 300 bps), 6/27/25 |

168,008 |

| 586,966 |

Surgery Center Holdings, Inc., 2021 New Term Loan, 9.205% (Term SOFR + 375 bps), 8/31/26 |

587,934 |

| |

Total Medical-Hospitals |

|

|

|

| |

Medical-Outpatient & Home Medicine — 0.8% |

|

| 372,187 |

Charlotte Buyer, Inc., First Lien Initial Term Loan B, 10.571% (Term SOFR + 525 bps), 2/11/28 |

$ 372,453 |

| 372,188 |

EyeCare Partners LLC, Incremental First Lien Term Loan, 9.983% (Term SOFR + 450 bps), 11/15/28 |

195,398 |

| 492,896 |

Medical Solutions Holdings, Inc., First Lien Initial Term Loan, 8.698% (Term SOFR + 325 bps), 11/1/28 |

450,590 |

| |

Total Medical-Outpatient & Home Medicine |

|

|

|

| |

Medical-Wholesale Drug Distribution — 0.4% |

|

| 447,750 |

CVET Midco 2 LP, First Lien Initial Term Loan, 10.39% (Term SOFR + 500 bps), 10/13/29 |

$ 443,312 |

| |

Total Medical-Wholesale Drug Distribution |

|

|

|

| |

Metal Processors & Fabrication — 1.9% |

|

| 988,728 |

Grinding Media, Inc. (Molycop, Ltd.), First Lien Initial Term Loan, 9.684% (Term SOFR + 400 bps), 10/12/28 |

$ 961,538 |

| 733,125 |

Tiger Acquisition LLC, First Lien Initial Term Loan, 8.698% (Term SOFR + 325 bps), 6/1/28 |

726,099 |

| 729,697 |

WireCo WorldGroup, Inc., Initial Term Loan, 9.696% (Term SOFR + 425 bps), 11/13/28 |

732,434 |

| |

Total Metal Processors & Fabrication |

|

|

|

| |

Metal-Aluminum — 0.8% |

|

| 944,000 |

Arsenal AIC Parent LLC, Term Loan B, 9.848% (Term SOFR + 450 bps), 8/18/30 |

$ 946,006 |

| |

Total Metal-Aluminum |

|

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

25

Schedule of Investments | 11/30/23

(continued)

|

|

|

|

|

|

Value |

| |

Mining Services — 0.1% |

|

| 172,148 |

Flame NewCo LLC, First Lien New Money Exit Term Loan, 11.448% (Term SOFR + 600 bps), 6/30/28 |

$ 160,958 |

| |

Total Mining Services |

|

|

|

| |

Multimedia — 0.4% |

|

| 470,625 |

The E.W. Scripps Company, Tranche B-3 Term Loan, 8.463% (Term SOFR + 300 bps), 1/7/28 |

$ 457,830 |

| |

Total Multimedia |

|

|

|

| |

Non-hazardous Waste Disposal — 0.7% |

|

| 859,779 |

Patriot Container Corp. (aka Wastequip), First Lien Closing Date Term Loan, 9.198% (Term SOFR + 375 bps), 3/20/25 |

$ 819,298 |

| |

Total Non-hazardous Waste Disposal |

|

|

|

| |

Office Automation & Equipment — 0.7% |

|

| 877,500 |

Pitney Bowes, Inc., Refinancing Tranche B Term Loan, 9.463% (Term SOFR + 400 bps), 3/17/28 |

$ 859,950 |

| |

Total Office Automation & Equipment |

|

|

|

| |

Oil&Gas Drilling — 0.2% |

|

| 210,000 |

GIP Pilot Acquisition Partners LP, Initial Term Loan, 8.388% (Term SOFR + 300 bps), 10/4/30 |

$ 210,000 |

| |

Total Oil&Gas Drilling |

|

|

|

| |

Oil-Field Services — 0.2% |

|

| 240,845 |

ProFrac Holdings II LLC, Delayed Draw Term A Loan, 12.902% (Term SOFR + 725 bps), 3/4/25 |

$ 241,448 |

| 42,892 |

ProFrac Holdings II LLC, Term Loan, 12.926% (Term SOFR + 725 bps), 3/4/25 |

43,106 |

| |

Total Oil-Field Services |

|

|

|

| |

Pastoral & Agricultural — 0.5% |

|

| 638,625 |

Alltech, Inc., Term B Loan, 9.463% (Term SOFR + 400 bps), 10/13/28 |

$ 631,440 |

| |

Total Pastoral & Agricultural |

|

|

|

| |

Pharmacy Services — 0.3% |

|

| 343,875 |

Option Care Health, Inc., First Lien 2021 Refinancing Term Loan, 8.213% (Term SOFR + 275 bps), 10/27/28 |

$ 345,293 |

| |

Total Pharmacy Services |

|

|

|

| |

Physical Practice Management — 1.7% |

|

| 2,922,088 |

Team Health Holdings, Inc., Extended Term Loan, 10.633% (Term SOFR + 525 bps), 3/2/27 |

$ 2,137,507 |

| |

Total Physical Practice Management |

|

|

|

The accompanying notes are an integral part of these financial statements.

26

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

|

|

|

|

|

|

Value |

| |

Physical Therapy & Rehabilitation Centers — 2.4% |

|

| 919,333 |

Summit Behavioral Healthcare LLC, First Lien Initial Term Loan, 10.40% (Term SOFR + 475 bps), 11/24/28 |

$ 920,099 |

| 2,173,771 |

Upstream Newco, Inc., First Lien August 2021 Incremental Term Loan, 9.895% (Term SOFR + 425 bps), 11/20/26 |

2,036,824 |

| |

Total Physical Therapy & Rehabilitation Centers |

|

|

|

| |

Pipelines — 4.4% |

|

| 597,000 |

Brazos Delaware II LLC, Initial Term Loan, 9.08% (Term SOFR + 375 bps), 2/11/30 |

$ 597,870 |

| 249,954(b) |

Buckeye Partners LP, 2023 Tranche B-2 Term Loan, 11/22/30 |

250,188 |

| 692,716 |

GIP III Stetson I LP (GIP III Stetson II LP), 2023 Initial Term Loan, 9.698% (Term SOFR + 425 bps), 10/31/28 |

692,024 |

| 471,000(b) |

M6 ETX Holdings II MidCo LLC, Initial Term Loan, 9/19/29 |

471,343 |

| 500,000 |

NorthRiver Midstream Finance LP, First Lien Initial Term Loan B, 8.395% (Term SOFR + 300 bps), 8/16/30 |

500,591 |

| 3,002,478 |

Traverse Midstream Partners LLC, Advance, 9.24% (Term SOFR + 375 bps), 2/16/28 |

3,004,979 |

| |

Total Pipelines |

|

|

|

| |

Professional Sports — 0.4% |

|

| 500,000 |

Formula One Management Ltd., First Lien Facility B Loan, 7.598% (Term SOFR + 225 bps), 1/15/30 |

$ 501,172 |

| |

Total Professional Sports |

|

|

|

| |

Property & Casualty Insurance — 2.7% |

|

| 222,750 |

Asurion LLC, New B-10 Term Loan, 9.448% (Term SOFR + 400 bps), 8/19/28 |

$ 218,295 |

| 246,172 |

Asurion LLC, New B-11 Term Loan, 9.699% (Term SOFR + 425 bps), 8/19/28 |

242,480 |

| 487,500 |

Asurion LLC, New B-9 Term Loan, 8.713% (Term SOFR + 325 bps), 7/31/27 |

477,489 |

| 1,250,000 |

Asurion LLC, Second Lien New B-4 Term Loan, 10.713% (Term SOFR + 525 bps), 1/20/29 |

1,108,202 |

| 1,358,620 |

Sedgwick Claims Management Services, Inc. (Lightning Cayman Merger Sub, Ltd.), 2023 Term Loan, 9.098% (Term SOFR + 375 bps), 2/24/28 |

1,361,244 |

| |

Total Property & Casualty Insurance |

|

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

27

Schedule of Investments | 11/30/23

(continued)

|

|

|

|

|

|

Value |

| |

Protection-Safety — 1.4% |

|

| 1,470,000 |

APX Group, Inc., Initial Term Loan, 8.924% (Term SOFR + 325 bps), 7/10/28 |

$ 1,471,838 |

| 270,000 |

Prime Security Services Borrower LLC, First Lien 2023 Refinancing Term B-1 Loan, 7.829% (Term SOFR + 250 bps), 10/13/30 |

270,405 |

| |

Total Protection-Safety |

|

|

|

| |

Publishing — 2.1% |

|

| 839,203 |

Cengage Learning, Inc., First Lien Term B Loan, 10.406% (Term SOFR + 475 bps), 7/14/26 |

$ 839,832 |

| 792,000 |

Houghton Mifflin Harcourt Co., First Lien Term Loan B, 10.698% (Term SOFR + 525 bps), 4/9/29 |

768,116 |

| 983,731 |

McGraw-Hill Education, Inc., Initial Term Loan, 10.213% (Term SOFR + 475 bps), 7/28/28 |

969,453 |

| |

Total Publishing |

|

|

|

| |

Publishing-Periodicals — 0.3% |

|

| 369,375 |

MJH Healthcare Holdings LLC, Initial Term B Loan, 8.948% (Term SOFR + 350 bps), 1/28/29 |

$ 367,759 |

| |

Total Publishing-Periodicals |

|

|

|

| |

Recreational Centers — 0.4% |

|

| 500,000 |

Fitness International LLC, Term B Loan, 8.698% (Term SOFR + 325 bps), 4/18/25 |

$ 498,750 |

| |

Total Recreational Centers |

|

|

|

| |

Recycling — 0.6% |

|

| 831,612 |

LTR Intermediate Holdings, Inc., Initial Term Loan, 9.963% (Term SOFR + 450 bps), 5/5/28 |

$ 769,241 |

| |

Total Recycling |

|

|

|

| |

Retail — 5.5% |

|

| 534,958 |

Great Outdoors Group LLC, Term B-2 Loan, 9.402% (Term SOFR + 375 bps), 3/6/28 |

$ 531,651 |

| 985,078(b) |

Harbor Freight Tools USA, Inc., 2021 Initial Term Loan, 10/19/27 |

979,481 |

| 1,007,500 |

Highline Aftermarket Acquisition LLC, First Lien Initial Term Loan, 9.949% (Term SOFR + 450 bps), 11/9/27 |

1,001,203 |

| 1,026,375 |

Michaels Cos, Inc., Term Loan B, 9.902% (Term SOFR + 425 bps), 4/15/28 |

814,685 |

| 469,191 |

Petco Health & Wellness Co., Inc., First Lien Initial Term Loan, 8.902% (Term SOFR + 325 bps), 3/3/28 |

445,145 |

| 1,026,375 |

PetSmart LLC, Initial Term Loan, 9.198% (Term SOFR + 375 bps), 2/11/28 |

1,019,319 |

| 1,231,348(b) |

RVR Dealership Holdings LLC, Term Loan, 2/8/28 |

998,418 |

The accompanying notes are an integral part of these financial statements.

28

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

|

|

|

|

|

|

Value |

| |

Retail — (continued) |

|

| 450,000 |

Torrid LLC, Closing Date Term Loan, 11.265% (Term SOFR + 550 bps), 6/14/28 |

$ 307,687 |

| 740,578 |

White Cap Supply Holdings LLC, Initial Closing Date Term Loan, 9.098% (Term SOFR + 375 bps), 10/19/27 |

741,167 |

| |

Total Retail |

|

|

|

| |

Retail-Misc/Diversified — 0.3% |

|

| 400,000(b) |

Peer Holding III B.V., Term Loan B4, 10/19/30 |

$ 400,083 |

| |

Total Retail-Misc/Diversified |

|

|

|

| |

Rubber & Plastic Products — 0.9% |

|

| 1,121,404 |

Gates Global LLC, Initial B-3 Dollar Term Loan, 7.948% (Term SOFR + 250 bps), 3/31/27 |

$ 1,122,338 |

| |

Total Rubber & Plastic Products |

|

|

|

| |

Schools — 0.3% |

|

| 425,855 |

Fugue Finance LLC (Bach Finance), Existing Term Loan, 9.388% (Term SOFR + 400 bps), 1/31/28 |

$ 427,917 |

| |

Total Schools |

|

|

|

| |

Security Services — 1.8% |

|

| 347,342 |

Allied Universal Holdco LLC (f/k/a USAGM Holdco LLC), Initial U.S. Dollar Term Loan, 9.198% (Term SOFR + 375 bps), 5/12/28 |

$ 338,810 |

| 1,964,719 |

Garda World Security Corp., Term B-2 Loan, 9.746% (Term SOFR + 425 bps), 10/30/26 |

1,964,446 |

| |

Total Security Services |

|

|

|

| |

Semiconductor Equipment — 0.9% |

|

| 1,113,286 |

Ultra Clean Holdings, Inc., Second Amendment Term B Loan, 9.213% (Term SOFR + 375 bps), 8/27/25 |

$ 1,116,938 |

| |

Total Semiconductor Equipment |

|

|

|

| |

Shipbuilding — 0.4% |

|

| 473,813 |

LSF11 Trinity Bidco, Inc., Initial Term Loan, 9.823% (Term SOFR + 450 bps), 6/14/30 |

$ 474,997 |

| |

Total Shipbuilding |

|

|

|

| |

Telecom Services — 0.8% |

|

| 1,016,676 |

Windstream Services, LLC, Initial Term Loan, 11.698% (Term SOFR + 625 bps), 9/21/27 |

$ 957,370 |

| |

Total Telecom Services |

|

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Fund, Inc. |

Annual Report

|

11/30/23

29

Schedule of Investments | 11/30/23

(continued)

|

|

|

|

|

|

Value |

| |

Telephone-Integrated — 0.7% |

|

| 1,000,000 |

Level 3 Financing, Inc., Tranche B 2027 Term Loan, 7.213% (Term SOFR + 175 bps), 3/1/27 |

$ 933,250 |

| |

Total Telephone-Integrated |

|

|

|

| |

Television — 0.4% |

|

| 475,000 |

Gray Television, Inc., Term Loan E, 7.935% (Term SOFR + 250 bps), 1/2/26 |

$ 474,788 |

| |

Total Television |

|

|

|

| |

Textile-Home Furnishings — 0.3% |

|

| 492,500 |

Runner Buyer, Inc., Initial Term Loan, 11.003% (Term SOFR + 550 bps), 10/20/28 |

$ 389,075 |

| |

Total Textile-Home Furnishings |

|

|

|

| |

Theaters — 1.2% |

|

| 519,533 |

AMC Entertainment Holdings, Inc. (fka AMC Entertainment, Inc.), Term B-1 Loan, 8.436% (Term SOFR + 300 bps), 4/22/26 |

$ 422,932 |

| 597,000 |

Cinemark USA, Inc., Term Loan, 9.14% (Term SOFR + 375 bps), 5/24/30 |

598,567 |

| 447,750 |

Cirque du Soleil Canada Inc., Initial Term Loan, 9.64% (Term SOFR + 425 bps), 3/8/30 |

442,853 |

| |

Total Theaters |

|

|

|

| |

Transportation - Trucks — 0.4% |

|

| 490,000 |

Carriage Purchaser, Inc., Term B Loan, 9.713% (Term SOFR + 425 bps), 10/2/28 |

$ 479,077 |

| |

Total Transportation - Trucks |

|

|

|

| |

Transportation Services — 2.0% |

|

| 1,176,000 |