| (20%)

(10%)

0%

10%

20%

30%

40%

Baseline NBH Outperformance

$0.54

$0.75 $0.80

$0.87

$0.94 $1.04

2018 2019 2020 2021 2022 2023

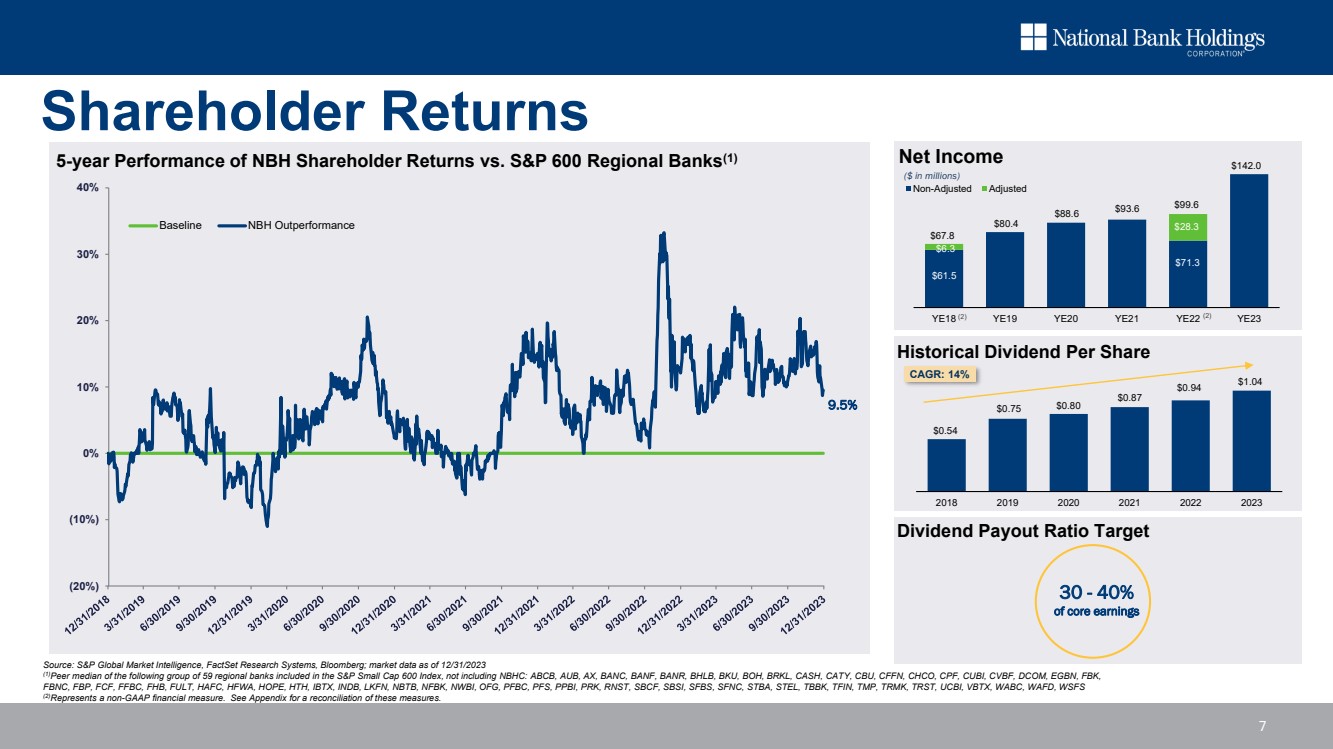

Shareholder Returns

Source: S&P Global Market Intelligence, FactSet Research Systems, Bloomberg; market data as of 12/31/2023

(1)Peer median of the following group of 59 regional banks included in the S&P Small Cap 600 Index, not including NBHC: ABCB, AUB, AX, BANC, BANF, BANR, BHLB, BKU, BOH, BRKL, CASH, CATY, CBU, CFFN, CHCO, CPF, CUBI, CVBF, DCOM, EGBN, FBK,

FBNC, FBP, FCF, FFBC, FHB, FULT, HAFC, HFWA, HOPE, HTH, IBTX, INDB, LKFN, NBTB, NFBK, NWBI, OFG, PFBC, PFS, PPBI, PRK, RNST, SBCF, SBSI, SFBS, SFNC, STBA, STEL, TBBK, TFIN, TMP, TRMK, TRST, UCBI, VBTX, WABC, WAFD, WSFS

(2)Represents a non-GAAP financial measure. See Appendix for a reconciliation of these measures.

5-year Performance of NBH Shareholder Returns vs. S&P 600 Regional Banks(1)

Historical Dividend Per Share

Dividend Payout Ratio Target

30 - 40%

of core earnings

CAGR: 14%

9.5%

$80.4 $28.3

$142.0

YE18 YE19 YE20 YE21 YE22 YE23

Net Income

Non-Adjusted Adjusted

($ in millions)

$88.6 $93.6

$61.5

$67.8

(2)

$6.3

$71.3

$99.6

(2)

7 |