Filed by Apollo Tactical Income Fund Inc.

pursuant to Rule 425 under the Securities Act of 1933

Subject Company: Apollo Tactical Income Fund Inc.

Commission File No. 811-22591

Date: March 4, 2024

MidCap Financial Investment Corporation Investor Presentation March 2024

Unless otherwise noted, information as of December 31, 2023. Confidential and Proprietary - Not for distribution, in whole or in part, without the express written consent of Apollo Global Management, Inc. It should not be assumed that investments

made in the future will be profitable or will equal the performance of the investments shown in this document.

Disclaimers, Definitions and Important Notes Forward-Looking Statements

statements, whether as a result of new information, future events or otherwise, you are advised to consult any additional disclosures that they may make directly to you or through reports that MFIC, AFT, and/or AIF Some of the statements in this

presentation constitute forward-looking statements because they relate to in the future may file with the Securities and Exchange Commission (“SEC”), including the Joint Proxy future events, future performance or financial condition. The

forward-looking statements may include Statement and the Registration Statement (in each case, as defined below), annual reports on Form 10-K, statements as to: future operating results of MidCap Financial Investment Corporation (the

“Corporation”, the annual reports on Form N-CSR, quarterly reports on Form 10-Q, semi-annual reports on Form N-CSRS and “Company” or “MFIC”, Apollo Senior Floating Rate Fund Inc. (“AFT”), and Apollo

Tactical Income Fund Inc. current reports on Form 8-K. (“AIF”), and distribution projections; business prospects of MFIC, AFT, and AIF, and the prospects of their portfolio companies, if applicable; and the impact of the investments that

MFIC, AFT, and AIF expect to make. In addition, words such as “anticipate,” “believe,” “expect,” “seek,” “plan,” “should,” “estimate,” “project” and Past

Performance “intend” indicate forward-looking statements, although not all forward-looking statements include these words. The forward-looking statements contained in this presentation involve risks and uncertainties. Certain Past

performance is not indicative nor a guarantee of future returns, the realization of which is dependent on many factors, many of which are beyond the control of Apollo Global Management, Inc., MFIC Adviser, Apollo factors could cause actual results

and conditions to differ materially from those projected, including the Credit Management LLC, MFIC, AFT, and AIF. There can be no assurances that future dividends will match or uncertainties associated with (i) the ability of the parties to

consummate one or both of the Mergers (as exceed historic ones, or that they will be made at all. Net returns give effect to all fees and expenses. Unless defined below) contemplated by the Merger Agreement among MFIC, AFT and certain other parties

thereto otherwise noted, information included herein is presented as of the date indicated on the cover page and and the Merger Agreement among MFIC, AIF and certain other parties thereto on the expected timeline, or at all; (ii) the expected

synergies and savings associated with the Mergers; (iii) the ability to realize the may change at any time without notice. MFIC, AFT and AIF are subject to certain significant risks relating to their businesses and investment objectives. For more

detailed information on risks relating to MFIC, AFT and anticipated benefits of the Mergers, including the expected elimination of certain expenses and costs due to AIF, see the latest annual reports on Form 10-K, annual reports on Form N-CSR,

quarterly reports on Form the Mergers; (iv) the percentage of the stockholders of MFIC, AFT, and AIF voting in favor of the applicable 10-Q, semi-annual reports on Form N-CSRS and current reports on Form 8-K, as applicable. Proposals (as defined

below); (v) the possibility that competing offers or acquisition proposals will be made; (vi) the possibility that any or all of the various conditions to the consummation of the Mergers may not be satisfied or waived; (vii) risks related to

diverting management’s attention from ongoing business operations; Financial Data (viii) the combined company’s plans, expectations, objectives and intentions, as a result of the Mergers; (ix) any potential termination of one or both

merger agreements; (x) the future operating results and net Financial data used in this presentation for the periods shown is from MFIC's, AFT's and AIF's Form 10-K, investment income projections of MFIC, AIF, AFT or, following the closing of one or

both of the Mergers, the Form N-CSR, Form 10-Q and Form N-CSRS filings, as applicable, with the SEC during such periods. Unless combined company; (xi) the ability of Apollo Investment Management L.P. (“MFIC Adviser”) to implement

otherwise indicated, the numbers shown herein are rounded and unaudited. Quarterly, semi-annual, and MFIC Adviser’s future plans with respect to the combined company; (xii) the ability of MFIC Adviser and its annual financial information for

MFIC, AFT, and AIF refers to fiscal periods. All share and per share data affiliates to attract and retain highly talented professionals; (xiii) the business prospects of MFIC, AIF, AFT or, shown herein is adjusted for the one-for-three reverse

stock split of MFIC’s common stock which took effect following the closing of one or both of the Mergers, the combined company and the prospects of their at the close of business on November 30, 2018. portfolio companies; (xiv) the impact of

the investments that MFIC, AIF, AFT or, following the closing of one or both of the Mergers, the combined company expect to make; (xv) the ability of the portfolio companies of MFIC, AIF, AFT or, following the closing of one or both of the Mergers,

the combined company to achieve Additional Important Disclosure their objectives; (xvi) the expected financings and investments and additional leverage that MFIC, AIF, AFT or, This presentation is confidential and may not be distributed, transmitted

or otherwise communicated to following the closing of one or both of the Mergers, the combined company may seek to incur in the future; others, in whole or in part, without the express written consent of Apollo Global Management, Inc. (together

(xvii) the adequacy of the cash resources and working capital of MFIC, AIF, AFT or, following the closing of with its subsidiaries, “Apollo”) and is intended solely for the use of the persons to whom it has been one or both of the

Mergers, the combined company; (xviii) the timing of cash flows, if any, from the delivered. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any operations of the portfolio companies of MFIC, AIF, AFT

or, following the closing of one or both of the security, product or service. This presentation and the transactions, investments, products, services, securities Mergers, the combined company; (xix) future changes in laws or regulations (including

the interpretation of or other financial instruments referred to in this presentation are not directed to, or intended for distribution these laws and regulations by regulatory authorities); and (xx) the risk that stockholder litigation in to or use

by, any person or entity who is a citizen or resident of or located in any locality, state, country or connection with one or both of the Mergers may result in significant costs of defense and liability. MFIC, AFT, other jurisdiction where such

distribution, publication, availability or use would be contrary to any laws or and AIF have based the forward-looking statements included in this press release on information available to regulations. Recipients may only use this presentation to

the extent permitted by the applicable laws and them on the date hereof, and they assume no obligation to update any such forward-looking statements. 2 regulations and should be aware of and observe all such applicable laws and regulations. Although

MFIC, AFT, and AIF undertake no obligation to revise or update any forward-looking

Disclaimers, Definitions and Important Notes “Assets Under

Management”, or “AUM”, refers to the assets of the funds, partnerships and accounts to No Offer or Solicitation which Apollo provides investment management, advisory, or certain other investment-related services, This Presentation

is not, and under no circumstances is it to be construed as, a prospectus or an including, without limitation, capital that such funds, partnerships and accounts have the right to call from advertisement and the communication of this Presentation is

not, and under no circumstances is it to be investors pursuant to capital commitments. AUM equals the sum of: construed as, an offer to sell or a solicitation of an offer to purchase any securities in MFIC, AFT or AIF or in 1. The net asset value

(“NAV”), plus used or available leverage and/or capital commitments, or gross assets any fund or other investment vehicle managed by Apollo or any of its affiliates. plus capital commitments, of the yield and certain hybrid funds,

partnerships and accounts for which we Additional Information and Where to Find It provide investment management or advisory services, other than certain collateralized loan obligations (“CLOs”), collateralized debt obligations

(“CDOs”), and certain perpetual capital vehicles, which have a fee- This presentation relates to the proposed Mergers (as defined below) and certain related matters (the generating basis other than the mark-to-market value of the

underlying assets; for certain perpetual “Proposals”). In connection with the Proposals, MFIC, AFT, and AIF will file with the SEC and mail to their capital vehicles in yield, gross asset value plus available financing capacity;

respective stockholders a joint proxy statement on Schedule 14A (the “Joint Proxy Statement”), and MFIC will file with the SEC a registration statement that includes the Joint Proxy Statement and a prospectus of MFIC 2. The fair value of

the investments of equity and certain hybrid funds, partnerships and accounts Apollo manages or advise, plus the capital that such funds, partnerships and accounts are entitled to call from (the “Registration Statement”). The Joint Proxy

Statement and the Registration Statement will each contain investors pursuant to capital commitments, plus portfolio level financings; important information about MFIC, AFT, AIF and the Proposals. This communication does not constitute an offer to

sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. No 3. The gross asset value associated with the reinsurance investments of the portfolio company assets Apollo offer of securities shall be made

except by means of a prospectus meeting the requirements of Section 10 of manages or advises; and the Securities Act. STOCKHOLDERS OF MFIC, AFT, and AIF ARE URGED TO READ THE JOINT PROXY 4. The fair value of any other assets that Apollo manages or

advises for the funds, partnerships and accounts STATEMENT AND REGISTRATION STATEMENT, AND OTHER DOCUMENTS THAT ARE FILED OR WILL to which Apollo provides investment management, advisory, or certain other investment-related services, BE FILED WITH

THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, plus unused credit facilities, including capital commitments to such funds, partnerships and accounts for CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY

WILL CONTAIN investments that may require pre-qualification or other conditions before investment plus any other IMPORTANT INFORMATION ABOUT MFIC, AFT, and AIF AND THE PROPOSALS. Investors and security capital commitments to such funds, partnerships

and accounts available for investment that are not holders will be able to obtain the documents filed with the SEC free of charge at the SEC’s website, otherwise included in the clauses above. http://www.sec.gov or, for documents filed by

MFIC, from MFIC’s website at https://www.midcapfinancialic.com, and, for documents filed by AFT, from AFT’s website at Apollo’s AUM measure includes Assets Under Management for which Apollo charges either nominal or zero

https://www.apollofunds.com/apollo-senior-floating-rate-fund, and, for documents filed by AIF, from AIF’s fees. Apollo’s AUM measure also includes assets for which Apollo does not have investment discretion, website at

https://www.apollofunds.com/apollo-tactical-income-fund#shareholders. including certain assets for which Apollo earns only investment-related service fees, rather than management or advisory fees. Apollo’s definition of AUM is not based on any

definition of Assets Under Management contained in its governing documents or in any management agreements of the funds Apollo manages. Participants in the Solicitation Apollo considers multiple factors for determining what should be included in its

definition of AUM. Such factors include but are not limited to (1) Apollo’s ability to influence the investment decisions for existing and MFIC, its directors, certain of its executive officers and certain employees and officers of MFIC

Adviser and its available assets; (2) Apollo’s ability to generate income from the underlying assets in funds it manages; and affiliates may be deemed to be participants in the solicitation of proxies in connection with the Proposals. (3) the

AUM measures that Apollo uses internally or believe are used by other investment managers. Given Information about the directors and executive officers of MFIC is set forth in its proxy statement for its 2023 the differences in the investment

strategies and structures among other alternative investment managers, Annual Meeting of Stockholders, which was filed with the SEC on May 1, 2023. AFT, AIF, their directors, Apollo’s calculation of AUM may differ from the calculations

employed by other investment managers and, as certain of their executive officers and certain employees and officers of Apollo Credit Management, LLC and a result, this measure may not be directly comparable to similar measures presented by other

investment its affiliates may be deemed to be participants in the solicitation of proxies in connection with the Proposals. managers. Apollo’s calculation also differs from the manner in which its affiliates registered with the SEC Information

about the directors and executive officers of AFT and AIF is set forth in the proxy statement for report “Regulatory Assets Under Management” on Form ADV Part I and Form PF in various ways. Apollo uses their 2023 Annual Meeting of

Stockholders, which was filed with the SEC on April 21, 2023. Information AUM, Gross capital deployed and Dry powder as performance measurements of its investment activities, as regarding the persons who may, under the rules of the SEC, be

considered participants in the solicitation of well as to monitor fund size in relation to professional resource and infrastructure needs. the MFIC, AFT, and AIF stockholders in connection with the Proposals is contained in the Joint Proxy

Statement. These documents may be obtained free of charge from the sources indicated above. 3

Introduction MFIC Investment Highlights Table of Contents MFIC

Accomplishment and Portfolio Review Proposed Mergers of MFIC, AFT, and AIF Conclusion Appendix 4

Introduction 5

INTRODUCTION MidCap Financial Investment Corporation (“MFIC”)

Positioned to be a Pure Play Senior Secured Middle Market BDC MFIC is a publicly traded (NASDAQ: Apollo is a high growth MFIC) business development company 1 MidCap Financial is a global alternative asset (“BDC”) treated as a regulated

investment leading lender to middle manager with approximately company (“RIC”) for tax purposes focused market companies 2 $651 billion of AUM and on investing primarily in senior secured manages both MidCap loans to middle market

companies 3 Financial and MFIC sourced from MidCap Financial’s portfolio and investments Strong Alignment of Interest % Equity Ownership in MFIC ü Apollo Global Management 3.8% 2 ü MidCap Financial 3.0% 4 ü MFIC Directors and

Officers 1.2% 1. MidCap Financial refers to MidCap FinCo Designated Activity Company, a designated activity company limited by shares incorporated under the laws of Ireland, and its subsidiaries, including MidCap Financial Services, LLC. MidCap

Financial is managed by Apollo Capital Management, L.P., a subsidiary of Apollo Global Management, Inc., pursuant to an investment management agreement between Apollo Capital Management, L.P. and MidCap FinCo Designated Activity Company. MidCap

Financial is not an investment adviser, subadviser or fiduciary to the Corporation or to the Corporation's Investment Adviser. MidCap Financial is not obligated to take into account the Corporation’s interests (or those of other potential

participants in assets sourced) when sourcing loans across its platform. 2. As of December 31, 2023. Please refer to the beginning of the presentation for the definition of AUM. 3. MidCap Financial is managed by Apollo Capital Management, L.P., a

subsidiary of Apollo Global Management, Inc. MidCap Financial Investment Corporation (“MFIC”) is managed by Apollo Investment Management, L.P., an affiliate of Apollo Global Management, Inc. 4. 6 Not Ee xc : N lud o g es u uar nves antte

ed e r thes att rtia cr ted ge s tst w ocill k b ue n a itsc.hieved.

INTRODUCTION MFIC Snapshot General Corporate Information Investment

Portfolio MFIC $2.33 billion Ticker Investment Portfolio NASDAQ Global Select 152 Exchange # of Portfolio Companies Net Assets $1.01 billion # of Industries 23 2 1 Kroll Bond Rating Agency BBB- / Stable Corporate Lending and Other % 92% Note: Past

performance is not indicative nor a guarantee of future results. Information as of December 31, 2023. At fair value, unless otherwise noted. 1. Kroll Bond Rating Agency rating affirmed in June 2023. 2. Corporate lending includes leveraged lending,

life sciences, franchise finance, asset based and lender finance. Excludes Merx Aviation and other select investments. 7

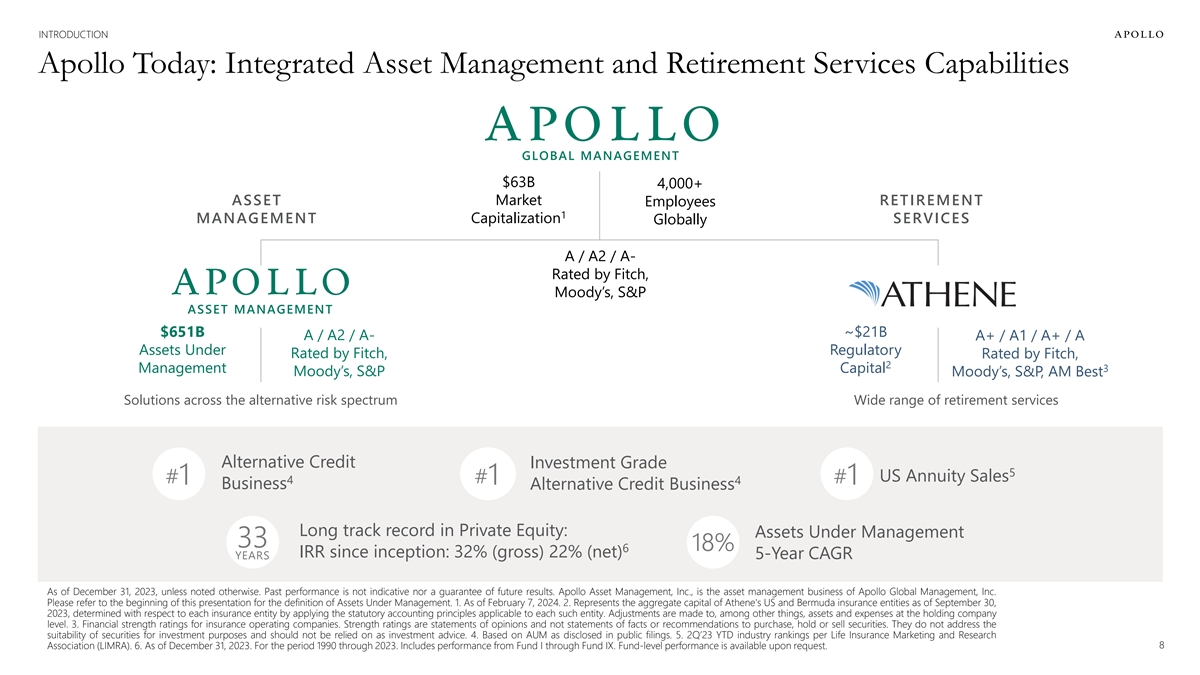

INTRODUCTION Apollo Today: Integrated Asset Management and Retirement

Services Capabilities GLOBAL MANAGEMENT $63B 4,000+ ASSET Market RETIREMENT Employees 1 MANAGEMENT Capitalization SERVICES Globally A / A2 / A- Rated by Fitch, Moody’s, S&P ASSET MANAGEMENT $651B ~$21B A / A2 / A- A+ / A1 / A+ / A Assets

Under Regulatory Rated by Fitch, Rated by Fitch, 2 Management Capital 3 Moody’s, S&P Moody’s, S&P, AM Best Solutions across the alternative risk spectrum Wide range of retirement services Alternative Credit Investment Grade 5 US

Annuity Sales 4 #1 #1 4 #1 Business Alternative Credit Business Long track record in Private Equity: Assets Under Management 33 18% 6 IRR since inception: 32% (gross) 22% (net) 5-Year CAGR YEARS As of December 31, 2023, unless noted otherwise. Past

performance is not indicative nor a guarantee of future results. Apollo Asset Management, Inc., is the asset management business of Apollo Global Management, Inc. Please refer to the beginning of this presentation for the definition of Assets Under

Management. 1. As of February 7, 2024. 2. Represents the aggregate capital of Athene's US and Bermuda insurance entities as of September 30, 2023, determined with respect to each insurance entity by applying the statutory accounting principles

applicable to each such entity. Adjustments are made to, among other things, assets and expenses at the holding company level. 3. Financial strength ratings for insurance operating companies. Strength ratings are statements of opinions and not

statements of facts or recommendations to purchase, hold or sell securities. They do not address the suitability of securities for investment purposes and should not be relied on as investment advice. 4. Based on AUM as disclosed in public filings.

5. 2Q’23 YTD industry rankings per Life Insurance Marketing and Research Association (LIMRA). 6. As of December 31, 2023. For the period 1990 through 2023. Includes performance from Fund I through Fund IX. Fund-level performance is available

upon request. 8

INTRODUCTION 1 MidCap Financial is a Leading Middle Market Lender Key

Members of Management Team Working Together Full-Service Finance Company Scaled Platform with Strong Credit Track Record 25+ Years • Founded in 2008 • Well-established provider of senior debt • Focused on senior debt solutions to

middle 2 Annual Originations solutions to middle market companies and market companies across multiple industries has what we believe to be an exceptionally • Extensive coverage of middle market strong track record through multiple ~ $15 Bn

sponsors economic cycles • Lead / sole lender on most transactions 3 • Privately-held by institutional investors and Commitments Managed / Serviced managed by a subsidiary of Apollo ~ $50 Bn Experienced Leadership Team Managed by Apollo

Employees • Headquartered in Bethesda, MD • Hub of Apollo’s private middle market credit ~ 300 business • Senior leadership of MidCap Financial has • Sources assets for its own balance sheet and deep industry expertise

-MidCap Financial & other blue chip lenders including Merrill for other Apollo-managed capital, including Global Offices MFIC Lynch Capital, GE Capital, and Heller Financial 12 Information as of December 31, 2023. 1. MidCap Financial refers to

MidCap FinCo Designated Activity Company, a designated activity company limited by shares incorporated under the laws of Ireland, and its subsidiaries, including MidCap Financial Services, LLC. MidCap Financial is managed by Apollo Capital

Management, L.P., a subsidiary of Apollo Global Management, Inc., pursuant to an investment management agreement between Apollo Capital Management, L.P. and MidCap FinCo Designated Activity Company. MidCap Financial is not an investment adviser,

subadviser or fiduciary to the Corporation or to the Corporation's Investment Adviser. MidCap Financial is not obligated to take into account the Corporation’s interests (or those of other potential participants in assets sourced) when

sourcing loans across its platform. 2. Based on last twelve months through December 31, 2023. 3. Includes commitments managed by MidCap Financial Services Capital 9 9 Management LLC, a registered investment adviser, as reported under Item 5.F on

Part 1 of its Form ADV. For more information about MidCap Financial, please visit http://www.midcapfinancial.com.

MFIC Investment Highlights 10

MFIC INVESTMENT HIGHLIGHTS MFIC Investment Highlights § Bank

retrenchment from lending expands opportunity set for non-bank lenders resulting in attractive environment for private credit origination Secular Tailwinds 1 § Value proposition for direct lending in terms of flexibility and reliability have

continued to drive increased market share for direct lending 1 1 § Primarily focused on senior secured middle market loans sourced from Midcap Financial’s portfolio and investments; MidCap Financial is a leading middle market lender with

a broad suite of financing solutions Robust Origination 2 Capabilities § Affiliation with Apollo provides significant benefits; Ability to co-invest with broader Apollo platform enhances ability to win deals on the 2 basis of size and certainty

of execution § Emphasis on first lien, cash pay, and diversification by sponsor, industry and end market Prudent Portfolio 3 Construction § Ability to participate in large commitments while maintaining granular positions

Shareholder-Friendly § Industry leading fee structure among listed BDCs supports MFIC’s senior secured investment strategy 4 Fee Structure 1. MidCap Financial refers to MidCap FinCo Designated Activity Company, a designated activity

company limited by shares incorporated under the laws of Ireland, and its subsidiaries, including MidCap Financial Services, LLC. MidCap Financial is managed by Apollo Capital Management, L.P., a subsidiary of Apollo Global Management, Inc.,

pursuant to an investment management agreement between Apollo Capital Management, L.P. and MidCap FinCo Designated Activity Company. MidCap Financial is not an investment adviser, subadviser or fiduciary to the Corporation or to the

Corporation’s Investment Adviser. MidCap Financial is not obligated to take into account the Corporation’s interests (or those of other potential participants in assets sourced) when sourcing loans across its platform. 2. On December 29,

2021, the Corporation received an exemptive order from the SEC, which was amended on January 10, 2023 (the “Order”), permitting greater flexibility to participate in co-investment transactions with certain of its affiliates where terms

other than price and quantity are negotiated, subject to the conditions included therein. The Order superseded a prior exemptive order received from the SEC on March 29, 2016. 11

MFIC INVESTMENT HIGHLIGHTS: SECULAR TAILWINDS Bank Continued Retrenchment

from Middle Market Lending Expands the 1 Opportunity for Non-Bank Lenders 1 2, 3 Total Number of U.S. Banks Continues to Decline Banks’ Reduced Participation in Loan Market 12,000 100% ~ 65%+ reduction in bank share of the loan market since

1994 50%+ decline since 2000 90% 10,000 80% 72% 70% 75% 8,000 60% 50% 6,000 40% 30% 25% 4,000 28% 20% 10% 2,000 0% 0 Banks & Securities Firms Non-banks 1. Source: FDIC as of September 30, 2023. FDIC-Insured commercial banks and savings

institutions. 2. Source: PitchBook LCD Quarterly Leveraged Lending Review 4Q 2023. Due to a significant decline in loan issuance in the last 12 months, LCD did not track enough observations to compile meaningful averages for investor analysis for

2023. 3. Non-banks includes institutional investors and finance companies. 12 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

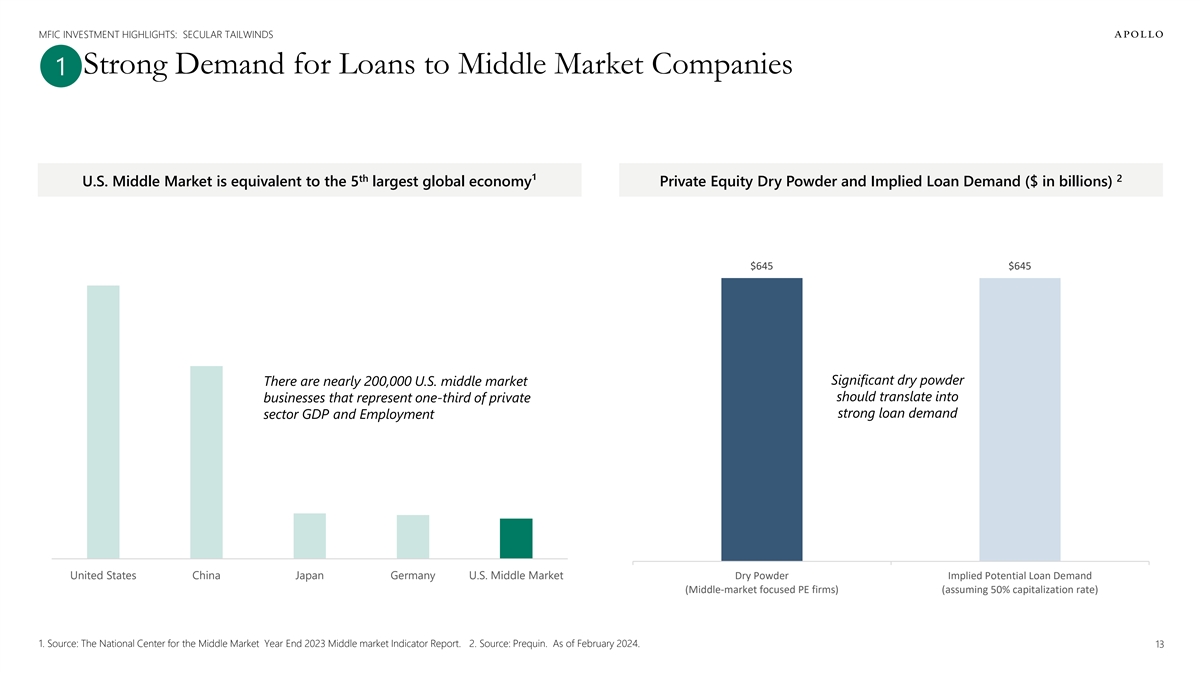

MFIC INVESTMENT HIGHLIGHTS: SECULAR TAILWINDS Strong Demand for Loans to

Middle Market Companies 1 th 2 U.S. Middle Market is equivalent to the 5 largest global economy¹ Private Equity Dry Powder and Implied Loan Demand ($ in billions) $645 $645 Significant dry powder Significant dry powder should translate into

Significant dry powder There are nearly 200,000 U.S. middle market should translate into strong loan demand should translate into businesses that represent one-third of private strong loan demand strong loan demand sector GDP and Employment United

States China Japan Germany U.S. Middle Market Dry Powder Implied Potential Loan Demand (Middle-market focused PE firms) (assuming 50% capitalization rate) 1. Source: The National Center for the Middle Market Year End 2023 Middle market Indicator

Report. 2. Source: Prequin. As of February 2024. 13

MFIC INVESTMENT HIGHLIGHTS: SECULAR TAILWINDS How Private Credit Produces

Better Outcomes for Lenders 1 Broadly Syndicated Direct Origination Loans Credit Documentation Control Due Diligence Access Partial Full Relationship with Borrower Limited Comprehensive Origination and Spread Economics Syndication Control Recurring

Flow and Allocation Control Direct origination makes it possible to control the structure, the process and documentation Reflects the views and opinions of Apollo Analysts. Subject to change at any time without notice. 14

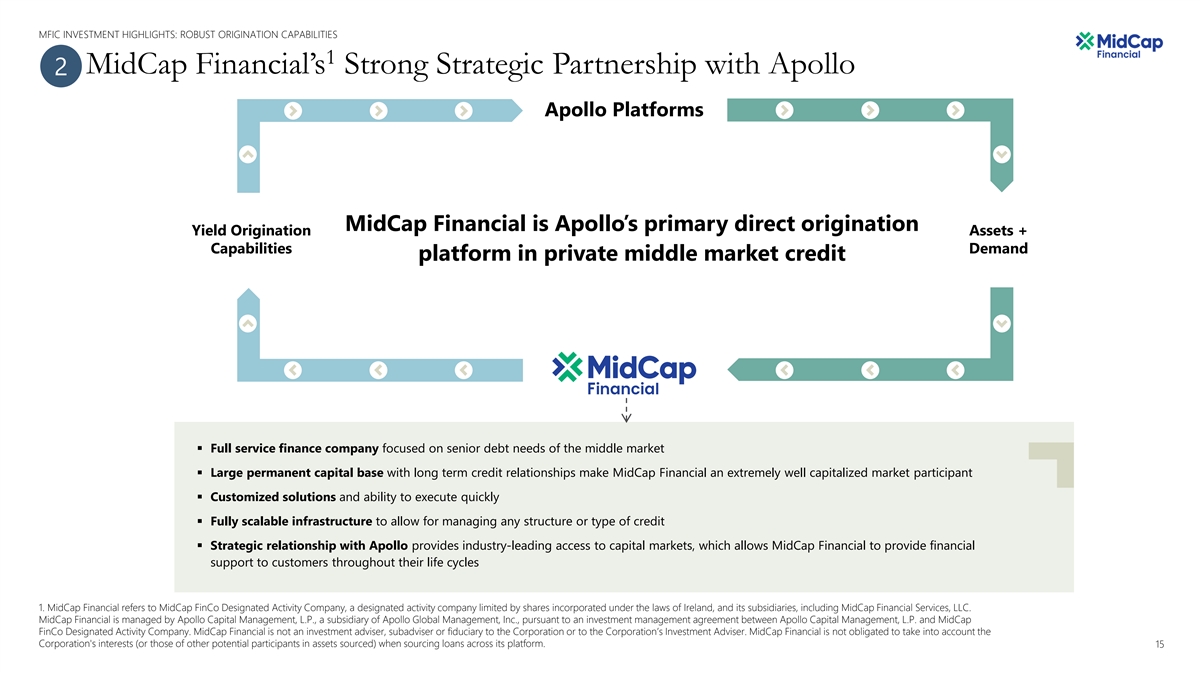

MFIC INVESTMENT HIGHLIGHTS: ROBUST ORIGINATION CAPABILITIES 1 MidCap

Financial’s Strong Strategic Partnership with Apollo 2 Apollo Platforms MidCap Financial is Apollo’s primary direct origination Yield Origination Assets + Capabilities Demand platform in private middle market credit § Full service

finance company focused on senior debt needs of the middle market § Large permanent capital base with long term credit relationships make MidCap Financial an extremely well capitalized market participant § Customized solutions and ability

to execute quickly § Fully scalable infrastructure to allow for managing any structure or type of credit § Strategic relationship with Apollo provides industry-leading access to capital markets, which allows MidCap Financial to provide

financial support to customers throughout their life cycles 1. MidCap Financial refers to MidCap FinCo Designated Activity Company, a designated activity company limited by shares incorporated under the laws of Ireland, and its subsidiaries,

including MidCap Financial Services, LLC. MidCap Financial is managed by Apollo Capital Management, L.P., a subsidiary of Apollo Global Management, Inc., pursuant to an investment management agreement between Apollo Capital Management, L.P. and

MidCap FinCo Designated Activity Company. MidCap Financial is not an investment adviser, subadviser or fiduciary to the Corporation or to the Corporation’s Investment Adviser. MidCap Financial is not obligated to take into account the

Corporation's interests (or those of other potential participants in assets sourced) when sourcing loans across its platform. 15

MFIC INVESTMENT HIGHLIGHTS: ROBUST ORIGINATION CAPABILITIES 1 MidCap

Financial Offers a Broad Suite of Products, Providing Solutions to 2 Nearly All Financing Needs of Middle Market Clients Business Segments Leveraged Asset Based Real Estate Lender Life Sciences and Franchise Lending Lending Lending Finance

Technology Lending Lending Product Capabilities Senior First Senior Senior Cash Senior Asset Franchise Mortgage Venture Based Debt Flow Debt Debt Debt Debt Middle Market 1. MidCap Financial refers to MidCap FinCo Designated Activity Company, a

designated activity company limited by shares incorporated under the laws of Ireland, and its subsidiaries, including MidCap Financial Services, LLC. MidCap Financial is managed by Apollo Capital Management, L.P., a subsidiary of Apollo Global

Management, Inc., pursuant to an investment management agreement between Apollo Capital Management, L.P. and MidCap FinCo Designated Activity Company. MidCap Financial is not an investment adviser, subadviser or fiduciary to the Corporation or to

the Corporation’s Investment Adviser. MidCap Financial is not obligated to take into account the Corporation's interests (or those of other potential participants in assets sourced) when sourcing loans across its platform. 16

MFIC INVESTMENT HIGHLIGHTS: ROBUST ORIGINATION CAPABILITIES 1 MidCap

Financial Proven Leadership in Industry 2 2 Middle Market Lending League Table Rank Lender # Deals 1 Antares Capital 183 MIDCAP FINANCIAL 159 2 3 TPG Twin Brook 138 Churchill 124 4 Ares Capital Corp 107 5 6 Crescent Capital 89 Apogem Capital (fka

Madison Capital) 70 7 8 Monroe Capital 66 Morgan Stanley Private Credit 66 8 Barings 65 9 10 Deerpath Capital 58 1. MidCap Financial refers to MidCap FinCo Designated Activity Company, a designated activity company limited by shares incorporated

under the laws of Ireland, and its subsidiaries, including MidCap Financial Services, LLC. MidCap Financial is managed by Apollo Capital Management, L.P., a subsidiary of Apollo Global Management, Inc., pursuant to an investment management agreement

between Apollo Capital Management, L.P. and MidCap FinCo Designated Activity Company. MidCap Financial is not an investment adviser, subadviser or fiduciary to the Corporation or to the Corporation’s Investment Adviser. MidCap Financial is not

obligated to take into account the Corporation's interests (or those of other potential participants in assets sourced) when sourcing loans across its platform. 2. Source: KBRA DLD’s rankings for full year 2023. Reflects lenders serving as

lead/co-lead. 17

MFIC INVESTMENT HIGHLIGHTS: PRUDENT PORTFOLIO CONSTRUCTION Investment

Strategy 3 Focused on First Lien Loans to Middle Market Companies Focused on true first lien assets, top of the capital structure, with flexibility to invest across the capital structure 1 Assets Primarily Sourced by MidCap Financial’s

Portfolio and Investments Primarily focused on senior secured middle market loans sourced by Midcap Financial, a leading middle market lender with a broad product suite and significant expertise in niche asset classes Ability to co-invest with

MidCap Financial and the broader Apollo platform enhances ability MFIC positioned 2 to be a pure play to win deals on the basis of size and certainty of execution senior secured middle market Prudent Portfolio Construction BDC Prudent portfolio

construction including granular position sizes and emphasis on diversification - by sponsor, industry, and end market 1. MidCap Financial refers to MidCap FinCo Designated Activity Company, a designated activity company limited by shares

incorporated under the laws of Ireland, and its subsidiaries, including MidCap Financial Services, LLC. MidCap Financial is managed by Apollo Capital Management, L.P., a subsidiary of Apollo Global Management, Inc., pursuant to an investment

management agreement between Apollo Capital Management, L.P. and MidCap FinCo Designated Activity Company. MidCap Financial is not an investment adviser, subadviser or fiduciary to the Corporation or to the Corporation’s Investment Adviser.

MidCap Financial is not obligated to take into account the Corporation's interests (or those of other potential participants in assets sourced) when sourcing loans across its platform. 2. On December 29, 2021, the Corporation received an exemptive

order from the SEC, which was amended on January 10, 2023 (the “Order”), permitting greater flexibility to participate in co-investment transactions with certain of its affiliates where terms other than price and quantity are negotiated,

subject to the conditions included therein. The Order superseded a prior exemptive order received from the SEC on March 29, 2016. 18 18

MFIC INVESTMENT HIGHLIGHTS: PRUDENT PORTFOLIO CONSTRUCTION MFIC Compares

Favorably to BDC Averages on Select Key Metrics 3 We believe MFIC’s revenue We believe MFIC’s portfolio is We believe MFIC’s relatively quality is higher compared to more senior when compared to high exposure to floating rate peers

with far less contribution BDC peers which should loans helps lower mitigate some of the credit risks from non-cash sources of interest rate risk in a more challenging operating income environment 1 2 1, 3 First Lien Exposure PIK Income % Total

Income Floating Rate Exposure 7% 87% 86% 83% 75% 1% MFIC BDC Average MFIC BDC Average MFIC BDC Average Note: Past performance is not indicative nor a guarantee of future results. 1. Source: Raymond James Business Development Company Weekly, January

22, 2024. 2. Source: Calculated based on data from Wells Fargo 1Q24 BDC Scorecard, January 29, 2024. Based on TTM data as of September 30, 2023. 3. MFIC’s corporate lending portfolio is 100% floating rate. Corporate lending includes leveraged

lending, life sciences, franchise finance, asset based and lender finance. Excludes Merx Aviation and other select investments. 19

MFIC INVESTMENT HIGHLIGHTS: SHAREHOLDER FRIENDLY FEE STRUCTURE MFIC Has

the Lowest Fee Structure, Among Listed BDCs 4 MFIC charges a management fee of 1.75% on net assets (i.e., equity) (equates to ~0.75% on gross assets) while all comparable listed BDCs charge on gross assets at a higher comparable rate. 2.0% 1.90%

1.75% 32.0% 1.70% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.50% 1.4% 27.0% 1.25% 1.30% 1.10% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 22.0% 0.90% 0.75% 20% 20.0% 20% 20% 20% 20% 20% 20% 0.70% 17.0% 17.5% 17.5% 17.5% 17.5% 17.5% 17.5% 17.5% 17.5%

17.5% 17.5% 17.5% 17.5% 0.50% 15.0% 15.0% 12.0% 0.30% MFIC BXSL GBDC GSBD MSDL NCDL PFLT BBDC NMFC ARCC BCSF TCPC CGBD CION FSK OCSL OBDC OBDE PNNT TSLX SLRC PSEC Total Return Yes Yes Yes Yes Yes Yes No Yes No No Yes Yes No No No No No No No No No

No Hurdle Management Fee on Assets Incentive Fee Rate Source: Company filings. All BDC data shown as of December 31, 2023. Peer set is defined as largest externally managed, diversified BDCs and excludes one BDC which does not have a comparable

investment strategy. There can be no assurance that the BDCs presented will continue to have the BDC fee structures presented. Fee structure comparison includes managements fees and incentive in income and capital gains. Certain BDCs may not charge

management fees on cash and / or have tiered fee structures. MFIC’s new fee structure became effective on January 1, 2023. Prior to this reduction, MFIC’s base management fee was 1.5% on gross assets financed using leverage up to 1.0x

debt-to-equity and 1.0% on gross assets financed using leverage over 1.0x debt-to equity. 20

MFIC 2023 Accomplishments and Portfolio Review 21

MFIC 2023 ACCOMPLISHMENTS AND PORTFOLIO REVIEW 2023 Key Accomplishments

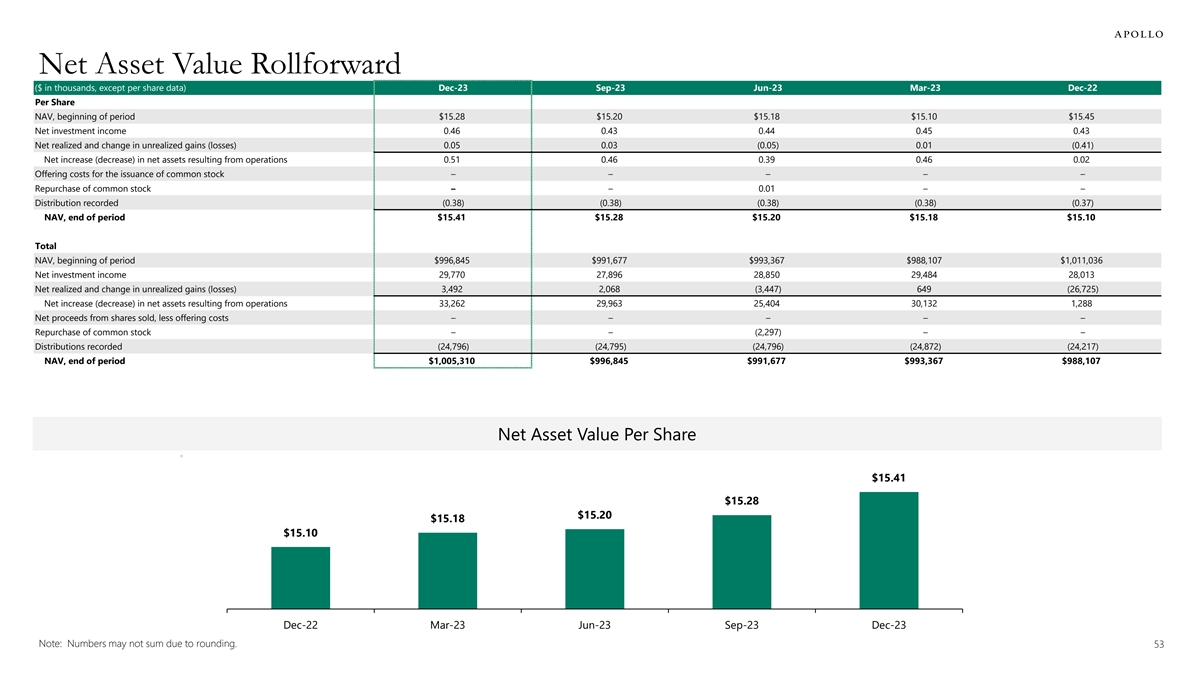

• Net Investment Income ROE of 11.7% benefitted from elevated base rates, solid fee and prepayment income, and MFIC’s industry leading fee structure Generated ü 1 Solid ROE’s • Net Income ROE of 11.9% aided by modest

portfolio appreciation given stable performance of our borrowers Demonstrated • NAV per share rose $0.31 (from $15.10 as of 12/31/22 to $15.41 as of 12/31/23) or 2.1% as net investment income outpaced distributions by 17% NAV Stability and

ü • Approach to dividends seeks to provide shareholders with an attractive current yield, while also retaining some earnings for NAV stability and growth Growth • Amended Senior Secured Revolving Credit Facility including extending

final maturity by over 2 years and achieving a slight reduction in pricing Enhanced • Closed inaugural CLO (MFIC Bethesda CLO 1 LLC), a $402 million CLO secured by middle market loans, with the issuance of $230 million of AAA notes with a

ü Liability Structure spread of 240 bps over SOFR • Issued $80 million of 8.0% unsecured notes due 2028 in December 2023 2 • Reaping the rewards of our multi-year focus on investing in true first lien middle market loans sourced by

MidCap Financial Corporate Lending 3 • Investments on non-accrual status remain very low- $5.7 million or 0.2% of the total portfolio Portfolio Demonstrated ü Resilience Despite • Portfolio company weighted average net leverage

improved to 5.27x as of 12/31/23, compared to 5.49x as of 12/31/22 Headwinds • Portfolio company weighted average attachment point improved to 0.1x as of 12/31/23, compared to 0.2x as of 12/31/22 Significant Progress • Sold 26 aircraft

reducing owned fleet from 57 to 31 Reducing Exposure to ü • Reduced MFIC’s investment in Merx by 27% which reflects a $76 million return of capital Merx Note: Information on this slide is for the calendar year ended December 31,

2023. Past performance is not indicative nor a guarantee of future results. 1. NII ROE defined as net investment income dividend by average net assets. Net Income ROE defined as net increase (decrease) in net assets resulting form operations divided

by average net assets. 2. MidCap Financial refers to MidCap FinCo Designated Activity Company, a designated activity company limited by shares incorporated under the laws of Ireland, and its subsidiaries, including MidCap Financial Services, LLC.

MidCap Financial is managed by Apollo Capital Management, L.P., a subsidiary of Apollo Global Management, Inc., pursuant to an investment management agreement between Apollo Capital Management, L.P. and MidCap FinCo Designated Activity Company.

MidCap Financial is not an investment adviser, subadviser or fiduciary to the Corporation or to the Corporation's Investment Adviser. MidCap Financial is not obligated to take into account the Corporation’s interests (or those of other

potential participants in assets sourced) when sourcing loans across its platform. 3. As of December 31, 2023. At fair value. 22

MFIC Senior Secured Diversified Investment Portfolio Portfolio Snapshot

Portfolio by Strategy Portfolio by Industry Portfolio $2.33 bn # of Portfolio Companies 152 # of Industries 23 8% 17.8% 19.3% 1 Corporate Lending and Other % Total Portfolio 92% 9% Non-Accrual % Total Portfolio 0.2% 2.6% 7% 2.9% Corporate Lending

Portfolio Statistics 3.1% 2 Weighted Average Yield 12.2% 17.5% 3.6% Weighted Average Spread over SOFR 623 bps 4.8% First Lien 96% 77% Floating Rate 100% 8.1% 11.9% Sponsored 88% 8.4% 3 Pursuant to co-investment order 86% High Tech Industries Average

exposure $14.7 mn Healthcare & Pharmaceuticals 4 Leveraged Lending Business Services % with financial covenants 98% 11 Aviation and Consumer Transport 5 Corporate Lending Median EBITDA $47 mn Life Sciences Consumer Services and Other 5, 6, 7, 8

Weighted Avg Net Leverage 5.27 x Beverage, Food & Tobacco Lender Finance, Asset Based, Consumer Goods – Non-durable 5, 6, 7, 8 Franchise Finance and Other Weighted Avg Attachment Point 0.1 x 11 Transportation – Cargo, Distribution

Aviation 5, 6, 8, 9 Weighted Avg Interest Coverage 1.9 x Manufacturing, Capital Equipment Automotive 10 Other Note: As of December 31, 2023. At fair value, unless otherwise noted. Subject to change at any time. without notice. Past performance is

not indicative nor a guarantee of future results. There is no guarantee that similar allocations or investments will be available in the future. Diversification does not ensure profit or protect against loss. 1. Corporate lending includes leveraged

lending, life sciences, franchise finance, asset based and lender finance. Excludes Merx Aviation and other select investments. 2. Weighted average yield on debt investments. On a cost basis. Exclusive of investment on non-accrual status. Based on

average of beginning of period and end of period portfolio yield. 3. On December 29, 2021, the Corporation received an exemptive order from the SEC, which was amended on January 10, 2023 (the “Order”), permitting greater flexibility to

participate in co-investment transactions with certain of its affiliates where terms other than price and quantity are negotiated, subject to the conditions included therein. The Order superseded a prior exemptive order received from the SEC on

March 29, 2016. 4. On a cost basis. 5. Source: Company data. 6. Through MFIC position based on corporate lending portfolio. 7. Excludes select investments where metric is not relevant or appropriate or data is not available. 8. Weighted average by

cost. Current metric. 9. The weighted average interest coverage ratio of the corporate lending portfolio was 1.8x based on TTM EBITDA through September 2023 and estimated annualized interest expense assuming December 31, 2023 base rates. 10. Other

includes: Diversified Investment Vehicles, Banking, Finance, Real Estate; Insurance; Chemicals, Plastics & Rubber; Wholesale; Advertising, 23 Printing& Publishing; Construction & Building; Retail; Hotel, Gaming, Leisure, Restaurants;

Consumer Goods –Durable; Utilities –Electric; Telecommunications; Energy –Electricity and Energy –Oil & Gas. 11. As of December 31, 2023, Merx owned 31 aircraft with weighted average age ~13.2 years and weighted average

lease maturity of ~3.5 years.

MFIC 2023 ACCOMPLISHMENTS AND PORTFOLIO REVIEW MFIC Credit Quality Remains

Resilient 1 2 Median LTM EBITDA Net Leverage and Attachment Point Net Leverage Attachment Point $55 $54 5.49 x 5.45 x 5.45 x 5.44 x 5.27 x $50 $48 $47 0.2 x 0.1 x 0.1 x 0.1 x 0.1 x Dec-22 Mar-23 Jun-23 Sep-23 Dec-23 Dec-22 Mar-23 Jun-23 Sep-23

Dec-23 3 4 Cash Interest Coverage Investments on Non-Accrual Status $50.0 0.8% $45.0 0.7% $40.0 2.5 x 0.6% 0.5% 2.3 x $35.0 2.1 x 1.9 x 1.9 x 0.5% $30.0 0.4% 0.4% $25.0 0.4% 0.3% $20.0 0.3% 0.2% $12 $15.0 $10 $9 0.2% $7 $10.0 $6 0.1% $5.0 $0.0 0.0%

2 Dec-22 Mar-23 Jun-23 Sep-23 Dec-23 Dec-22 Mar-23 Jun-23 Sep-23 Dec-23 Investments on non-accrual $ % total portfolio Note: Past performance is not indicative nor a guarantee of future results. Source: Company data. 1. Based on corporate lending

portfolio. Excludes select investments where metric is not relevant or appropriate or data is not available. 2. Weighed average by cost. Current metric. Through MFIC position. 3. The weighted average interest coverage ratio of the corporate lending

portfolio was 1.8x based on TTM EBITDA through September 2023 and estimated annualized interest expense assuming December 31, 2023 base rates. 4. At fair value. 24

Proposed Mergers of MFIC, AFT, and AIF 25

PROPOSED MERGERS OF MFIC, AFT, AND AIF We Believe the Proposed Mergers of

AFT and AIF with MFIC 1 are in the Best Interests of All Shareholders & MFIC AFT & AIF 2 2 P Expected to be accretive to return on equity and net investment income per share ü Expected to be accretive to return on equity and net

investment income per share P Special cash dividendü Special cash payment and additional special cash dividend ü Increased scaleü Increased scale ü Expected to result in greater stock liquidityü Expected to result in

greater stock liquidity ü Potentially expands MFIC’s research analyst coverageü Gains benefit of research analyst coverage ü Expected to improve access to capitalü Expected to improve access to capital ü Potential

operational synergiesü Potential operational synergies ü Expected to improve portfolio metrics Proposed Mergers Create a Larger, More Scaled BDC Focused on Middle Market Direct Lending 1. In connection with the consideration of the

transactions, the boards of directors of MFIC, AFT, and AIF each established a special committee, consisting only of certain independent directors (the “MFIC Special Committee” and the “CEF Special Committees”). The boards of

directors of MFIC, AFT and AIF unanimously approved their respective mergers in consideration of the unanimous recommendations of the MFIC Special Committee and respective CEF Special Committees. 2. ROE denotes return on equity and NII denotes net

investment income. 26

PROPOSED MERGERS OF MFIC, AFT, AND AIF Significant Shareholder Financial

Benefits Related to the Transactions Special Cash Payment to • An affiliate of Apollo will make a special cash payment of $0.25 per share to each AFT or AIF shareholder of record as of the closing 1 AFT and AIF Shareholders date of the

applicable transaction, following the closing of the applicable merger. • Following the closing of the Merger(s), as applicable, MFIC will pay a cash dividend of $0.20 per share. The exact record date for the Special Cash Dividend $0.20 per

share special dividend will be determined by the MFIC Board of Directors based upon the timing of the closings of the to Shareholders 2 Merger(s). • All merger-related expenses will be reimbursed by an affiliate of Apollo for each successful

transaction. • A portion of the merger-related expenses of AFT or AIF, as applicable, will be reimbursed by an affiliate of Apollo, if the respective Transaction Expense transaction is not successful; the remainder will be borne by AFT or AIF,

as applicable. Reimbursement • In addition, a portion of the merger-related expenses of MFIC will be reimbursed by an affiliate of Apollo if neither transaction is successful; the remainder will be borne by MFIC. 1. The exact record date will

be the closing date of the applicable transaction. The specific tax characteristics of the $0.25 per share special cash payment have not yet been determined. Apollo and its affiliates make no assurances regarding the tax treatment to stockholders of

the receipt of this special cash payment. 2. The specific tax characteristics of the $0.20 per share special dividend have not yet been determined and will be reported to stockholders on Form 1099 after the end of the calendar year in which it is

paid. Apollo and its affiliates make no assurances regarding the tax treatment to stockholders of the receipt of this special dividend. 27

PROPOSED MERGERS OF MFIC, AFT, AND AIF Overview of MFIC, AFT, and AIF

MidCap Financial Apollo Senior Apollo Tactical Investment Corporation Floating Rate Fund Inc. Income Fund Inc. NASDAQ: MFIC NYSE: AFT NYSE: AIF Listed Business Development Company (“BDC”) Listed Closed End Fund (“CEF”) Listed

Closed End Fund (“CEF”) Structure Regulated under the 1940 Act Registered under the 1940 Act Registered under the 1940 Act Seek current income and preservation of capital Primary objective is to seek current income with by investing

primarily in senior, secured loans a secondary objective of preservation of capital Investment Generate current income and, to a lesser extent made to companies whose debt is rated below by investing in a portfolio of senior loans, Objective

long-term capital appreciation investment grade and investments with similar corporate bonds and other credit instruments of economic characteristics. varying maturities Inception Date April 8, 2004 February 23, 2011 February 25, 2013 Tax Structure

Regulated investment company (“RIC”) Regulated investment company (“RIC”) Regulated investment company (“RIC”) 1, 2 Portfolio Size / Direct Origination % $2.37 billion / 92% $346 million / 23% $311 million / 33% 2

Net Asset Value $997 million $234 million $212 million 2 Net Asset Value Per Share $15.28 $15.05 $14.63 2 Shares Outstanding 65,253,275 15,573,575 14,464,026 Regulatory Minimum 3 3 150% 300% 300% Asset Coverage Ratio Apollo Investment Management,

L.P., Apollo Credit Management, LLC. Apollo Credit Management, LLC. Investment Adviser an affiliate of Apollo Global Management, Inc. an affiliate of Apollo Global Management, Inc. an affiliate of Apollo Global Management, Inc. 1. At fair value. 2.

As of September 30, 2023. 3. On debt. 28

PROPOSED MERGERS OF MFIC, AFT, AND AIF 1 Summary of Key Terms of the

Transactions 2 • MFIC to acquire 100% of AFT and AIF in two parallel stock-for-stock transactions, with shares to be exchanged on a NAV-for-NAV basis • The Mergers will result in an ownership split of the combined company proportional to

each of MFIC’s, AFT’s, and AIF’s respective net asset values Structure of the Mergers • MFIC will be the surviving entity in both mergers and will continue to operate as a BDC and trade under the ticker symbol

“MFIC” on the NASDAQ Global Select Exchange • The Transactions are intended to be treated as tax-free reorganizations • Cash payment of $0.25 per share from an affiliate of Apollo Global Management, Inc.

(“Apollo”) to each AFT or AIF shareholder of record as of the closing of the applicable transaction, following the closing of the 3 Special Cash Payment applicable transaction • Following the closing of the Merger(s), as

applicable, MFIC will pay a cash dividend of $0.20 per share. The exact record date for the $0.20 per share special dividend will be determined by the MFIC Board of Directors 4 Special Cash Dividend based upon the timing of the closings of the

Merger(s) 5 • Combined company will have approximately $3.4 billion of investments and $1.4 billion of net assets 6 • No change to MFIC’s investment strategy which will remain focused on first lien floating rate loans to middle

market companies, primarily sourced by MidCap Financial 6 Pro Forma Balance Sheet • AFT’s and AIF’s liquid assets will be rotated in the ordinary course into first lien floating rate loans to middle market companies, primarily

sourced by MidCap Financial 7 • The mergers unlock approximately $330 million of incremental asset capacity due to MFIC’s lower minimum asset coverage • AFT’s and AIF’s existing indebtedness will be repaid by MFIC

contemporaneous to the closing of each transaction Merger Contingency • The mergers are not contingent on each other; i.e., MFIC can acquire one fund if shareholder approval is not obtained for both funds • All merger-related expenses

will be reimbursed by an affiliate of Apollo for each successful transaction Transaction Expenses • A portion of the merger-related expenses of AFT or AIF, as applicable, will be reimbursed by an affiliate of Apollo, if the respective

transaction is not successful; the remainder will be borne by AFT or AIF, as applicable • In addition, a portion of the merger-related expenses of MFIC will be reimbursed by an affiliate of Apollo if neither transaction is successful; the

remainder will be borne by MFIC • Apollo Investment Management, L.P., an affiliate of Apollo will continue to serve as the investment adviser of the combined company Post-Merger Governance • All current MFIC officers and directors will

remain in their current positions • MFIC Affirmative vote of a majority of votes cast • AFT Affirmative vote of majority of outstanding shares Closing Conditions • AIF Affirmative vote of majority of outstanding shares •

Other customary closing conditions • Filed a registration statement and preliminary joint proxy statement / prospectus Expected Timing • Anticipated closing in the first half of 2024, subject to shareholder approvals and other customary

closing conditions 1. The descriptions set forth above are a summary of certain terms and are not intended to be complete. Please refer to the Merger Agreements for complete descriptions of the key terms of each merger. 2. The NAV’s used in

determining the exchange ratios will include any distributions declared prior to each closing and will be determined within 48 hours prior to closing of the applicable merger. 3. The exact record date will be the closing date of the applicable

transaction. The specific tax characteristics of the $0.25 per share special cash payment have not yet been determined. Apollo and its affiliates make no assurances regarding the tax treatment to stockholders of the receipt of this special cash

payment 4. The specific tax characteristics of the $0.20 per share special dividend have not yet been determined and will be reported to stockholders on Form 1099 after the end of the calendar year in which it is paid. Apollo and its affiliates make

no assurances regarding the tax treatment to stockholders of the receipt of this special dividend. 5. Based on net assets as of September 30, 2023 for MFIC, AFT, and AIF. Includes the impact of the special cash dividend of $0.20 per share from the

combined company, payable after the closings to each MFIC share, including existing MFIC shares and the newly issued MFIC shares. Based on MFIC’s net leverage ratio of 1.40x. The net leverage ratio is defined as debt outstanding plus payable

for investments purchased, less receivable for investments sold, less cash and cash equivalents, less foreign currencies, divided by net assets. 6. MidCap Financial refers to MidCap FinCo Designated Activity Company, a designated activity company

limited by shares incorporated under the laws of Ireland, and its subsidiaries, including MidCap Financial Services, LLC. MidCap Financial is managed by Apollo Capital Management, L.P., a subsidiary of Apollo Global Management, Inc., pursuant to an

investment management agreement between Apollo Capital Management, L.P. and MidCap FinCo Designated Activity Company. MidCap Financial is not an investment adviser, subadviser or fiduciary to MFIC or MFIC’s Investment Adviser. MidCap Financial

is not obligated to take into account MFIC’s interests (or those of other potential participants in assets sourced) when sourcing loans across its platform. 7. MFIC is subject to a 150% minimum asset coverage requirement pursuant to Section

61(a)(2) of the 1940 Act, as amended by The Small Business Credit Availability Act (“SBCAA”). AFT and AIF are both subject to a 300% minimum asset coverage requirement on debt pursuant to Section 18 of the 1940 Act. 29

PROPOSED MERGERS OF MFIC, AFT, AND AIF Illustrative Exchange Ratios and

MFIC Pro Forma Ownership 1 Illustrative Exchange Ratios Pro Forma Ownership AFT AIF $15.05 $14.63 AFT NAV Per Share AIF NAV Per Share $15.28 $15.28 AIF MFIC NAV Per Share MFIC NAV Per Share 15% 0.9849 x 0.9577 x Exchange Ratio Exchange Ratio AFT Pro

Forma 16% 2 15.6 14.5 Net Assets AFT Shares Outstanding AIF Shares Outstanding $1,424 MFIC 15.3 13.9 69% MFIC Shares Issued MFIC Shares Issued to AFT Shareholders to AIF Shareholders 29.2 Total MFIC Shares Issued 1. Illustrative exchange ratios

based on NAV per share for MFIC, AFT, and AIF as of September 30, 2023. Under the terms of each merger agreement, AFT and AIF shareholders will receive an amount of new MFIC shares based upon the net asset values of each company at the time each

closing. The NAV’s used in determining the exchange ratios will include any distributions declared prior to each closing and will be determined within 48 hours prior to closing of the applicable merger. Changes in the NAV per share of MFIC,

AFT, and AIF before the consummation of the mergers may impact the exchange ratios. 2. Pro forma net assets includes the impact of the special cash dividend of $0.20 per share from the combined company, payable by MFIC after the closing of the

Merger(s). 30

PROPOSED MERGERS OF MFIC, AFT, AND AIF 1 Total Consideration to AFT and

AIF (Illustrative ) 2 MFIC to acquire 100% of AFT and AIF in two parallel stock-for-stock transactions, with shares to be exchanged on a NAV-for-NAV basis. In addition, an affiliate of Apollo will make a special cash payment of $0.25 per share to

each AFT or AIF shareholder of record as of the closing date 3 of the applicable transaction, following the closing of the applicable transaction. AFT AIF $15.30 $15.05 $0.25 $14.88 $14.63 $0.25 0.9849x share of 1 share of AFT 0.9577x share of MFIC

1 share of AIF NAV-for-NAV $15.05 MFIC $15.05 $14.63 NAV-for-NAV $14.63 Pre Merger Total Consideration Pre Merger Total Consideration Value Per Share Value Per Share NAV Cash payment from Apollo NAV Cash payment from Apollo 1. Illustrative exchange

ratio based on MFIC, AFT, and AIF NAV per share as of September 30, 2023. 2. Under the terms of each merger agreement, AFT and AIF shareholders will receive an amount of new MFIC shares based upon the net asset values of each company at the time of

each closing. The NAV’s used in determining the exchange ratios will include any distributions declared prior to each closing and will be determined within 48 hours prior to the closing of the applicable merger. Changes in the NAV per share of

MFIC, AFT, and AIF before the consummation of the mergers may impact the exchange ratios. 3. The exact record date will be the closing date of the applicable transaction. The specific tax characteristics of the $0.25 per share special cash payment

have not yet been determined. Apollo and its affiliates make no assurances regarding the tax treatment to stockholders of the receipt of this special cash payment. 31

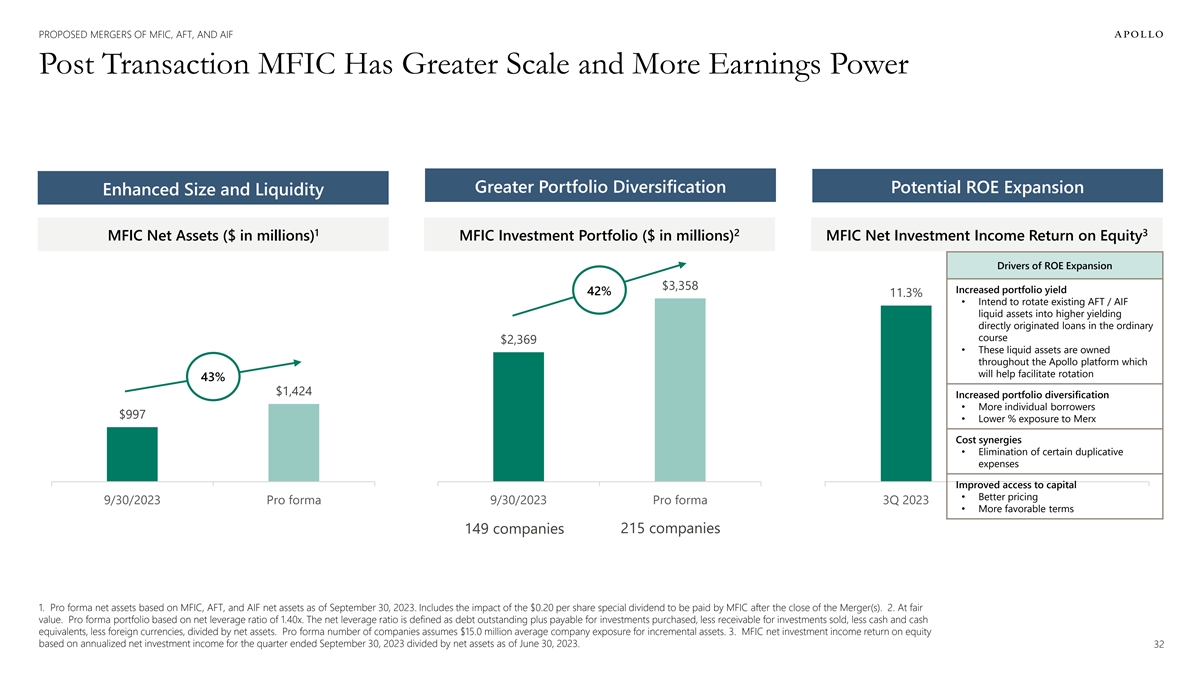

PROPOSED MERGERS OF MFIC, AFT, AND AIF Post Transaction MFIC Has Greater

Scale and More Earnings Power Greater Portfolio Diversification Potential ROE Expansion Enhanced Size and Liquidity 1 2 3 MFIC Net Assets ($ in millions) MFIC Investment Portfolio ($ in millions) MFIC Net Investment Income Return on Equity Drivers

of ROE Expansion $3,358 Increased portfolio yield 42% 11.3% • Intend to rotate existing AFT / AIF liquid assets into higher yielding directly originated loans in the ordinary course $2,369 • These liquid assets are owned throughout the

Apollo platform which will help facilitate rotation 43% $1,424 Increased portfolio diversification • More individual borrowers $997 • Lower % exposure to Merx Cost synergies • Elimination of certain duplicative expenses Improved

access to capital • Better pricing 9/30/2023 Pro forma 9/30/2023 Pro forma 3Q 2023 • More favorable terms 149 companies 215 companies 1. Pro forma net assets based on MFIC, AFT, and AIF net assets as of September 30, 2023. Includes the

impact of the $0.20 per share special dividend to be paid by MFIC after the close of the Merger(s). 2. At fair value. Pro forma portfolio based on net leverage ratio of 1.40x. The net leverage ratio is defined as debt outstanding plus payable for

investments purchased, less receivable for investments sold, less cash and cash equivalents, less foreign currencies, divided by net assets. Pro forma number of companies assumes $15.0 million average company exposure for incremental assets. 3. MFIC

net investment income return on equity based on annualized net investment income for the quarter ended September 30, 2023 divided by net assets as of June 30, 2023. 32

PROPOSED MERGERS OF MFIC, AFT, AND AIF Expense Synergies The proposed

mergers of AFT and AIF with MFIC are expected to be accretive to net investment income in part due to the opportunity for operating synergies by eliminating certain duplicative corporate expenses 1 Category Potential Savings Annual G&A Expenses

($ in millions) • Administrative fees ~$3.1 m potential $19.1 • Insurance Administrative savings $16.0 • Listing fees • Regulatory fees • Legal expenses • Audit fees Other • Board of Directors professional

services • Internal audit fees MFIC + AFT + AIF Pro forma (current expenses) expenses • Tax related expenses 3 • Printing and mailing expenses Pre-Merger Pro forma 2 Expense ratio 0.60% 0.47% 1. Current expenses reflect general and

administrative expenses for last twelve months as of September 30, 2023. 2. Expense ratio defined as general and administrative expense for last twelve months as of September 30, 2023 divided by average quarterly total assets from September 30, 2022

through September 30, 2023. 3. Pro forma expense ratio reflects potential general and administrative savings of $3.1 million and pro forma balance sheet of approximately $3.4 billion. 33

Average Daily Valued Traded 3 Month PROPOSED MERGERS OF MFIC, AFT, AND AIF

Increased Scale and Secondary Market Liquidity Potential for increased stock liquidity could lead to increased institutional ownership 2 1 Market Cap, Trading Volume & Research Coverage ($ in millions) Net Asset Value ($ in millions) $1,600

Market Capitalization Average Daily Value Traded 3 Months ($19) $212 $1,424 $1,600 $10.0 $1,400 $234 $9.0 $1,400 $1,200 $1,279 $997 $8.0 $1,000 $1,200 $7.0 $800 $1,000 $882 $6.0 $600 $800 $5.0 $4.0 $400 $600 $3.0 $200 $400 $2.0 $2.5 $206 $191 $0

$200 $1.0 MFIC AFT AIF Special $0.20 MFIC $1.3 $0.8 Per Share Pro forma $0 $- Dividend MFIC AFT AIF MFIC Pro forma Potentially 10 0 0 The combination of MFIC, AFT, and AIF would result in a Research expands MFIC’s analysts analysts analysts

larger, more scaled BDC Coverage analyst coverage 1. Net asset value for MFIC, AFT, and AIF as of September 30, 2023. MFIC pro forma net assets includes the impact of the $0.20 per share special dividend, payable by MFIC after the closing of the

Merger(s). 2. Market capitalization and average daily value traded 3 months as of November 3, 2023. Combined market capitalization does not include the impact of the $0.20 per share special dividend. 34 Market Capitalization

PROPOSED MERGERS OF MFIC, AFT, AND AIF Investment Portfolios Affiliates of

Apollo manage MFIC, AFT, and AIF, which mitigates the diligence concerns typically associated with mergers of unaffiliated entities. The CEFs’ portfolios primarily include liquid assets that are owned throughout the Apollo platform, which will

help facilitate a seamless rotation in the ordinary course into directly originated assets that align with MFIC’s investment strategy. MFIC AFT AIF 8% 5% 0% 8% Structured Credit and High Yield Other Merx Other 14% Bonds High Yield 40% 32%

Bonds Direct Direct Origination Origination $2.33 92% $317 $336 billion Direct million million Origination 62% 38% Broadly Broadly Syndicated Loans Syndicated Loans On a fair value basis. As of December 31, 2023. May not sum to 100% due to rounding.

Private and Confidential 35

PROPOSED MERGERS OF MFIC, AFT, AND AIF Pro Forma Portfolio Metrics Improve

Once Rotated and Deployed Portfolio Rotation, at Fair Value ($ in millions) 215 companies Deploy into direct origination Ø Portfolio increases by ~$1.0 billion $3,358 6%, $195 Ø Merx decreases to <6% $656 $332 149 companies 3 Rotate

into direct origination $474 $2,369 Retain $183 8%, $195 94% Ø Direct origination increases to 94% $3,162 92% $2,174 MFIC AFT + AIF Incremental Assets MFIC (9/30/23) (9/30/23) Pro Forma 1, 2 Direct Origination Merx Aviation, LLC Liquid Assets

(BSL, high yield bonds) Incremental Asset Capacity 1. Incremental asset capacity based on MFIC net leverage ratio of 1.40x. The net leverage ratio is defined as debt outstanding plus payable for investments purchased, less receivable for investments

sold, less cash and cash equivalents, less foreign currencies, divided by net assets. 2. MFIC is subject to a 150% minimum asset coverage requirement pursuant to Section 61(a)(2) of the 1940 Act, as amended by The Small Business Credit Availability

Act (“SBCAA”). AFT and AIF are both subject to a 300% minimum asset coverage requirement on debt pursuant to Section 18 of the 1940 Act. 3. Rotation will occur in the ordinary course. 36

PROPOSED MERGERS OF MFIC, AFT, AND AIF Existing Sources of Financing in

Place to Execute the Mergers MFIC Debt ($ in millions) $2,500 $2,500 $2,412 $2,412 $2,180 $374 $2,000 $2,000 Debt Outstanding $974 $2,038 $742 $600 $1,500 $1,500 Debt Outstanding Debt Outstanding $1,438 $1,438 $731 $731 $1,000 $1,000 $963 $232 $232

$500 $500 $125 $125 $125 $350 $350 $350 $- $- 9/30/2023 9/30/2023 Pro forma 1 Pro forma for CLO for Proposed Mergers 2 2025 Notes 2026 Notes MFIC Bethesda CLO 1 Revolver Outstanding Revolver Draw for the Proposed Mergers Undrawn Revolver Commitments

Note: The closed-end funds’ existing indebtedness will be repaid by MFIC contemporaneous to the closing of each transaction. 1. On November 2, 2023, MFIC completed a $402.36 million collateralized loan obligation (“CLO”)

transaction. Proceeds from the CLO transaction were used to repay borrowings under the Company’s multi-currency revolving credit facility (the “Revolver”). 2. Undrawn revolver commitments based on $1.705 billion of lender

commitments. Lender commitments under the Revolver will decrease to $1.550 billion on December 22, 2024. 37

PROPOSED MERGERS OF MFIC, AFT, AND AIF Combined Company Expected to

Generate Significant Value for All Shareholders Financially Attractive Transactions for All Shareholders Upfront cash payments and accretive to return on equity and net investment income per share Potential for Increased Shareholder Value Larger

company may enhance market visibility, increase stock liquidity, and increase shareholder value + Growth mindset Transactions Create a Larger BDC Focused on Middle Market Direct Lending 1 Leverages affiliation with MidCap Financial, a leading middle

market lender managed by Apollo 1. MidCap Financial refers to MidCap FinCo Designated Activity Company, a designated activity company limited by shares incorporated under the laws of Ireland, and its subsidiaries, including MidCap Financial

Services, LLC. MidCap Financial is managed by Apollo Capital Management, L.P., a subsidiary of Apollo Global Management, Inc., pursuant to an investment management agreement between Apollo Capital Management, L.P. and MidCap FinCo Designated

Activity Company. MidCap Financial is not an investment adviser, subadviser or fiduciary to MFIC or to MFIC’s Investment Adviser. MidCap Financial is not obligated to take into account the MFIC’s interests (or those of other potential

participants in assets sourced) when sourcing loans across its platform. 38

PROPOSED MERGERS OF MFIC, AFT, AND AIF Apollo Senior Floating Rate Fund

Inc. (NYSE: AFT) at a Glance Objective and Strategy 1 Portfolio Characteristics AFT is a diversified, closed-end management investment company. AFT’s investment objective Weighted Average Floating Rate Spread / % Floating Rate 4.96% / 92.3% is

to seek current income and preservation of capital by investing primarily in senior, secured loans made to companies whose debt is rated below investment grade and investments with Weighted Average Fixed Rate Coupon / % Fixed Rate 7.53% / 7.7%

similar economic characteristics. Weighted Average Maturity (in years) (floating assets) 4.24 Weighted Average Maturity (in years) (fixed assets) 5.07 Fund Facts and Data 2 Average Position Size by Issuer $3.8 million Symbol NYSE- AFT 2 Number of

Issuers 93 Inception Date 2/23/11 3 Weighted Average S&P Rating B Capital Structure 3 Weighted Average Rating Factor (Moody’s) 3,229 Shares Outstanding 15.6 million 4 Credit Quality Net Asset Value $234.1 million BB 4.4% Leverage $130.0

million B 54.8% Total Managed Assets $364.1 million CCC+ or Lower 9.6% Portfolio, at Fair Value $336.2 million Not Rated 31.2% Debt-to-Net Asset Value Ratio 0.56x 5 Top 5 Industries (% Market Value) Portfolio Composition (% Market Value) Services:

Business 18.3% Broadly Syndicated Loans 62.3% Healthcare & Pharmaceuticals 15.1% Direct Origination 32.0% High Tech Industries 15.0% High Yield Bonds 5.2% Banking, Finance, Insurance & Real Estate 9.2% Equity / Other 0.4% Telecommunications

6.0% Total 63.6% Information as of December 31, 2023. 1. Averages based on par value of investment securities, except for the % floating and fixed rate, which are based on market value. 2. Excludes equity investments. 3. Excludes securities with no

rating or non-performing defaulted securities as of December 31, 2023. Credit quality is calculated as a percentage of fair value of investment securities at December 31, 2023. The quality ratings reflected were issued by S&P Global Ratings

(“S&P”), an internationally recognized statistical rating organization. 4. Credit quality ratings reflect the rating agency’s opinion of the credit quality of the underlying positions in the Fund’s portfolio and not that

of the Fund itself. Credit quality ratings are subject to change. 5. The industry classifications reported are from widely recognized market indexes or rating group indexes, and/or as defined by Fund management, with the primary source being

Moody’s Investors Service (“Moody’s”), an internationally recognized statistical rating organization. 39

PROPOSED MERGERS OF MFIC, AFT, AND AIF Apollo Tactical Income Fund Inc.

(NYSE: AIF) at a Glance 1 Portfolio Characteristics Objective and Strategy AIF is a diversified, closed-end management investment company. The Fund’s primary Weighted Average Floating Rate Spread / % Floating Rate 5.57% / 84.3% investment

objective is to seek current income with a secondary objective of preservation of Weighted Average Fixed Rate Coupon / % Fixed Rate 6.73% / 15.7% capital by investing in a portfolio of senior loans, corporate bonds and other credit Weighted Average

Maturity (in years) (floating assets) 4.78 instruments of varying maturities. The Fund seeks to generate current income and preservation of capital primarily by allocating assets among different types of credit Weighted Average Maturity (in years)

(fixed assets) 4.95 instruments based on absolute and relative value considerations. 2 Average Position Size by Issuer $3.4 million Fund Facts and Data 2 Number of Issuers 100 Symbol NYSE- AIF 3 Weighted Average S&P Rating B Inception Date

2/25/13 3 Weighted Average Rating Factor (Moody’s) 3,205 Capital Structure 4 Credit Quality Shares Outstanding 14.5 million BB 10.2% Net Asset Value $213.6 million B 37.7% Leverage $121.0 million CCC+ or Lower 11.0% Total Managed Assets $334.6

million Not Rated 41.1% Portfolio, at Fair Value $316.7 million 5 Top 5 Industries (% Market Value) Debt-to-Net Asset Value Ratio 0.57x Healthcare & Pharmaceuticals 16.6% Portfolio Composition (% Market Value) High Tech Industries 14.2% Broadly

Syndicated Loans 38.3% Services: Businesses 9.6% Direct Origination 40.5% Banking, Finance, Insurance & Real Estate 8.4% High Yield Bonds 13.5% Media: Advertising, Printing, & Publishing 7.3% Structured Products 7.4% Total 56.1% Equity /

Other 0.3% Information as of December 31, 2023. 1. Averages based on par value of investment securities, except for the % floating and fixed rate, which are based on market value. 2. Excludes equity investments. 3. Excludes securities with no rating

or non-performing defaulted securities as of December 31, 2023. Credit quality is calculated as a percentage of fair value of investment securities at December 31, 2023. The quality ratings reflected were issued by S&P Global Ratings

(“S&P”), an internationally recognized statistical rating organization. 4. Credit quality ratings reflect the rating agency’s opinion of the credit quality of the underlying positions in the Fund’s portfolio and not that

of the Fund itself. Credit quality ratings are subject to change. 5. The industry classifications reported are from widely recognized market indexes or rating group indexes, and/or as defined by Fund management, with the primary source being

Moody’s Investors Service (“Moody’s”), an internationally recognized statistical rating organization. Excludes Structured Products, which represent 7.4% of the fair value of the portfolio at December 31, 2023. 40

Conclusion 41

CONCLUSION Reasons to Own MFIC SECULAR TAILWINDS AND RECENT VOLATILITY

CREATE ATTRACTIVE ENVIRONMENT FOR PRIVATE CREDIT 1 1 ROBUST ORIGINATION CAPABILITIES OF MIDCAP FINANCIAL / APOLLO PROVIDE ATTRACTIVE AND SIGNIFICANT 2 DEAL FLOW PRUDENT PORTFOLIO CONSTRUCTION WITH FOCUS ON FIRST LIEN, CASH PAY, FLOATING RATE LOANS

TO MIDDLE 3 MARKET COMPANIES INDUSTRY-LEADING, SHAREHOLDER-FRIENDLY FEE STRUCTURE 4 1. MidCap Financial refers to MidCap FinCo Designated Activity Company, a designated activity company limited by shares incorporated under the laws of Ireland, and

its subsidiaries, including MidCap Financial Services, LLC. MidCap Financial is managed by Apollo Capital Management, L.P., a subsidiary of Apollo Global Management, Inc., pursuant to an investment management agreement between Apollo Capital

Management, L.P. and MidCap FinCo Designated Activity Company. MidCap Financial is not an investment adviser, subadviser or fiduciary to the Corporation or to the Corporation’s Investment Adviser. MidCap Financial is not obligated to take into

account the Corporation's interests (or those of other potential participants in assets sourced) when sourcing loans across its platform. 42

Appendix 43

MFIC Senior Leadership Team Howard T. Widra Executive Chairman Mr. Widra

has been with Apollo and/or its affiliates since 2013 and serves as Apollo’s Head of Direct Origination. He was appointed Executive Chairman in August 2022. He served as the Company’s Chief Executive Officer from May 2018 to August 2022

and as President from June 2016 to May 2018. He has also been a Director since May 2018. Mr. Widra was a co-founder of MidCap Financial, a middle-market specialty finance firm with $21.3 billion of annual originations1 and was formerly its Chief

Executive Officer. Prior to MidCap Financial, Mr. Widra was the founder and President of Merrill Lynch Capital Healthcare Finance. Prior to Merrill Lynch, Mr. Widra was President of GE Capital Healthcare Commercial Finance and held senior roles in

its predecessor entities including President of Heller Healthcare Finance, and COO of Healthcare Financial Partners. Mr. Widra holds a J.D., Cum Laude, from the Harvard Law School and a BA from the University of Michigan. Tanner Powell Chief

Executive Officer Mr. Powell joined Apollo in 2006. Mr. Powell was appointed Chief Executive Officer of the Company in August 2022. He served as President of the Company from May 2018 to August 2022 and served as Chief Investment Officer for the

Company’s investment adviser from June 2016 to August 2022. Mr. Powell is a Managing Director and Portfolio Manager in Apollo’s Direct Origination business. He holds leadership roles in Apollo’s Credit Business, including its

aircraft leasing and lending businesses. From 2004 to 2006, he served as an analyst in Goldman Sachs’ Principal Investment Area (PIA). From 2002 to 2004, Mr. Powell was an Analyst in the Industrials group at Deutsche Bank. He graduated from

Princeton University with a BA in political economy. Ted McNulty President and Chief Investment Officer, AIM Mr. McNulty joined Apollo in 2014. He is a is Managing Director in Apollo’s Credit business. He was appointed President of the Company

and Chief Investment Officer for the Company’s investment adviser in August 2022. Prior to joining Apollo, Mr. McNulty ran the mezzanine and later merchant banking business for a subsidiary of Mitsubishi UFJ, and was a director at Haland

before that. Previously, he held various roles at JPMorgan and its predecessor institutions, primarily in leveraged finance. Mr. McNulty received an MBA from the Kellogg School of Management and a BA in Government from Harvard University. Greg Hunt

Chief Financial Officer Mr. Hunt is a Managing Director of Finance at Apollo Global Management, Inc. He began his term as Chief Financial Officer and Treasurer of the Company in May 2012. Mr. Hunt also currently serves as Interim Chief Financial

Officer for Apollo Debt Solutions BDC. Previously, Mr. Hunt was Executive Vice President and Chief Financial Officer for Yankee Candle which he joined in April 2010. Prior to joining Yankee Candle, Mr. Hunt served as the Executive Vice President of

Strategic and Commercial Development for Norwegian Cruise Lines from 2007 to 2009. Prior to joining Norwegian Cruise Lines, Mr. Hunt served as Chief Financial Officer and Chief Restructuring Officer of Tweeter Home Entertainment Group, Inc. from

2006 to 2007 and Chief Financial Officer and Co-Chief Executive of Syratech Corporation from 2001 to 2006. Prior to Syratech, Mr. Hunt held several senior financial leadership positions including Chief Financial Officer of NRT Inc., Culligan Water

Technologies, Inc. and Samsonite `Corporation. Mr. Hunt has also served as a Director and Chairman of the Audit Committee of Kymera International, a global manufacturer and supplier of metal products, since January 2020; and as Director and Chairman

of the Audit Committee of Danimer Scientific (DNMR/NYSE), a leading developer and manufacturer of biodegradable plastic products, since June 2019. He is also the Co- Chair on the Board of Advisors for the University of Vermont School of Business.