UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM

20-F

☐

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the fiscal year ended June 30, 2024

OR

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date

of event requiring this shell company report for the transition period from ____________ to ____________

Commission

file number: 001-42277

GLOBAL

ENGINE GROUP HOLDING LIMITED

(Exact

Name of Registrant as Specified in its Charter)

N/A

(Translation

of Registrant’s Name into English)

British

Virgin Islands

(Jurisdiction

of Incorporation or Organization)

Room

C, 19/F, World Tech Centre,

95

How Ming Street, Kwun Tong, Kowloon, Hong Kong

(Address

of principal executive offices)

Mr.

Andrew, LEE Yat Lung

Tel:

+852 3955 2300

Email:

andrew.lee@globalengine.com.hk

Room C, 19/F, World Tech Centre,

95

How Ming Street, Kwun Tong, Kowloon, Hong Kong

(Name,

Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities

registered or to be registered pursuant to Section 12(b) of the Act:

Title

of Each Class | | Trading Symbol(s) | | Name of Each Exchange on Which Registered |

Ordinary Shares $0.0000625 par value per share | | GLE | | The NASDAQ Stock Market LLC |

Securities

registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities

for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate

the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered

by the annual report:

As of June 30, 2024, the issuer had 16,000,000

Ordinary Shares outstanding.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

If

this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section

13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate

by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth

company. See definition of “large accelerated filer,” accelerated filer,” and “emerging growth company”

in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Emerging growth company | ☒ |

If

an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant

to Section 13(a) of the Exchange Act. ☐

| † |

The term

“new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board

to its Accounting Standards Codification after April 5, 2012. |

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b) by the registered

public accounting firm that prepared or issued its audit report. Yes ☐ No ☒

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate

by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ | | International

Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | | Other ☐ |

| * |

If “Other”

has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected

to follow. Item 17 ☐ Item 18 ☐ |

If

this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange

Act). Yes ☐ No ☒

(APPLICABLE

ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate

by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities

Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☐

TABLE

OF CONTENTS

INTRODUCTION

Unless

otherwise indicated, numerical figures included in this Annual Report on Form 20-F (the “Annual Report”) have been subject

to rounding adjustments. Accordingly, numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures

that precede them.

For

the sake of clarity, this Annual Report follows the Hong Kong naming convention of last name followed by first name, regardless of whether

an individual’s name is Chinese or English. This Annual Report includes statistical and other industry and market data that we

obtained from industry publications and research, surveys and studies conducted by third parties. Industry publications and third-party

research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although

they do not guarantee the accuracy or completeness of such information. While we believe these industry publications and third-party

research, surveys and studies are reliable, you are cautioned not to give undue weight to this information.

| |

● |

“BVI” are to

the “British Virgin Islands”; |

| |

● |

“BVI Act” are

to the BVI Business Companies Act (Law Revision 2020) (as amended); |

| |

|

|

| |

● |

“BVI Sub” are

to Global Engine Holdings Limited, a BVI company; |

| |

● |

“China” or

the “PRC” are to the People’s Republic of China, including the special administrative regions of Hong Kong and

Macau for the purposes of Annual Report only;; |

| |

● |

the “Company”

or “GE Group” are to Global Engine Group Holding Limited, a BVI company; |

| |

● |

“mainland China”

are to the mainland of the People’s Republic of China; |

| |

● |

“GEL” are to

Global Engine Limited, a Hong Kong company; |

| |

● |

“Hong Kong”

are to the Hong Kong Special Administrative Region of the People’s Republic of China for the purposes of this Annual Report

only; |

| |

|

|

| |

● |

“ICT” are to

information communication technologies; |

| |

● |

“HKD” or “HK

Dollar” are to the legal currency of Hong Kong; |

| |

● |

“$,”

“dollars,” “US$” or “U.S. dollars” are to the legal currency of the United States; |

| |

|

|

| |

● |

“shares”

or “Ordinary Shares” are to the ordinary shares of Global Engine Group Holding Limited, par value $0.0000625 per share; |

| |

|

|

| |

● |

“U.S.

GAAP” are to generally accepted accounting principles in the United States; and |

| |

|

|

| |

● |

“we”,

or “us” in this Annual Report are to Global Engine Group Holding Limited, a BVI company and its subsidiaries, unless

the context otherwise indicates. |

This Annual Report contains translations of

certain foreign currency amounts into U.S. dollars for the convenience of the reader. Translations of amounts in the consolidated

balance sheet, consolidated statements of income, consolidated statements of cash flows and the section titled

“Compensation - Compensation of Executive Officers” from HKD into US$ as of and for the year ended June 30, 2024

are solely for the convenience of the reader and were calculated at the rate of US$1.00=HKD 7.8083 representing the exchange rate

set forth in the H.10 statistical release of the Federal Reserve Board on June 28, 2024. This Annual Report contains translations of

certain foreign currency amounts into U.S. dollars for the convenience of the reader. No representation is made that the HKD amounts

could have been, or could be, converted, realized or settled into US$ at such rate, or at any other rate. We do not have any

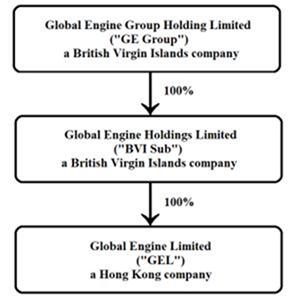

material operations of our own and we are a holding company with operations conducted in Hong Kong through our Hong Kong subsidiary

GEL, using Hong Kong dollars, the currency of Hong Kong. Global Engine Group Holding Limited’s reporting currency is Hong Kong

dollars.

FORWARD-LOOKING

INFORMATION

This

Annual Report contains forward-looking statements. These statements are made under the “safe harbor” provisions of Section

21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements can be identified by terminology such as “will,”

“expects,” “anticipates,” “future,” “intends,” “plans,” “believes,”

“estimates,” “may,” “intend,” “it is possible,” “subject to” and similar

statements. Among other things, the sections titled “Item 3. Key Information—D. Risk Factors,” “Item 4. Information

on the Company,” and “Item 5. Operating and Financial Review and Prospects” in this Annual Report, as well as our strategic

and operational plans, contain forward-looking statements. Statements that are not historical facts, including statements about our beliefs

and expectations, are forward-looking statements and are subject to change, and such change may be material and may have a material and

adverse effect on our financial condition and results of operations for one or more prior periods. Forward-looking statements involve

inherent risks and uncertainties. A number of important factors could cause actual results to differ materially from those contained,

either expressly or impliedly, in any of the forward-looking statements in this Annual Report. All information provided in this Annual

Report and in the exhibits is as of the date of this Annual Report, and we do not undertake any obligation to update any such information,

except as required under applicable law.

Part

I

Item

1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not

Applicable.

Item

2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not

Applicable.

Item

3. KEY INFORMATION

A.

[Reserved]

B.

Capitalization and Indebtedness

Not

applicable.

C.

Reasons for the Offer and Use of Proceeds

Not

applicable.

D.

Risk Factors

SUMMARY

OF RISK FACTORS

Investment

in our securities involves a high degree of risk. You should carefully consider the risks described below together with all of the other

information included in this Annual Report before making an investment decision. The risks and uncertainties described below represent

our known material risks to our business. If any of the following risks actually occurs, our business, financial condition or results

of operations could suffer. In that case, you may lose all or part of your investment.

Risks

Related to Our Business. See “Item 3. Key Information — Risk Factors — Risks Related to Our Business”

starting on page 6 of this Annual Report.

Risks

and uncertainties related to our business and industry include, but are not limited to, the following:

| |

● |

Changes

in capital markets, merger and acquisition activity, legal or regulatory requirements, general economic conditions and monetary or

geopolitical disruptions, as well as other factors beyond our control, could reduce demand for our practice offerings or services,

in which case our revenues and profitability could decline. |

| |

● |

Our

revenues, operating income and cash flows are likely to fluctuate. |

| |

● |

We

have a substantial customer concentration, with a limited number of customers accounting for a substantial portion of our revenues.

|

| |

|

|

| |

● |

We

are exposed to the credit risks of our customers. |

| |

● |

We

rely on a limited number of vendors. A loss of any of these vendors could significantly negatively affect our business. |

| |

● |

Inadequate

or inaccurate external and internal information, including budget and planning data, could lead to inaccurate financial forecasts

and inappropriate financial decisions. |

| |

|

|

| |

● |

We

may fail to innovate or create new solutions which align with changing market and customer demand. |

| |

● |

We

may not manage our growth effectively, and our profitability may suffer. |

| |

|

|

| |

● |

Our

limited operating history may not provide an adequate basis to judge our future prospects and results of operations. |

| |

|

|

| |

● |

A

failure in our information technology, or IT, systems could cause interruptions in our services, undermine the responsiveness of

our services, disrupt our business, damage our reputation and cause losses. |

| |

|

|

| |

● |

We

may not be able to protect our intellectual property rights. |

| |

● |

We

may be subject to intellectual property infringement claims, which may be expensive to defend and may disrupt our business and operations. |

| |

|

|

| |

● |

Our

principal shareholders have substantial influence over our company and their interests may not be aligned with the interests of our

other shareholders. |

| |

● |

If we

become directly subject to the recent scrutiny, criticism and negative publicity involving U.S.-listed Chinese companies, we may

have to expend significant resources to investigate and resolve the matter which could harm our business operations, stock price

and reputation and could result in a loss of your investment in our ordinary shares, especially if such matter cannot be addressed

and resolved favorably. |

| |

● |

If we

fail to compete effectively, we may miss new business opportunities or lose existing customers, and our revenues and profitability

may decline. |

Risks

Related to Our People. See “Item 3. Key Information — Risk Factors — Risks Related to Our People”

starting on page 20 of this Annual Report.

We

are also subject to risks and uncertainties related to our people, including, but not limited to, the following:

| |

● |

Our

failure to recruit and retain qualified professionals could negatively affect our financial results and our ability to staff client

engagements, maintain relationships with clients and drive future growth. |

| |

|

|

| |

● |

Headcount

reductions to manage costs during periods of reduced demand for our services could have negative impacts on our business over the

longer term. |

| |

|

|

| |

● |

Employees

may leave our Company to form or join competitors, and we may not have, or may choose not to pursue, legal recourse against such

professionals. |

Risks

Related to Acquisitions. See “Item 3. Key Information — Risk Factors — Risks Related to Acquisitions”

starting on page 21 of this Annual Report.

We

are also subject to risks and uncertainties related to our potential acquisitions, including, but not limited to, the following:

| |

● |

We

may have difficulty integrating acquisitions or convincing clients to allow assignment of their engagements to us, which can reduce

the benefits we receive from acquisitions. |

| |

|

|

| |

● |

An

acquisition may not be accretive in the near term or at all. |

| |

|

|

| |

● |

We

may have a different system of governance and management from a company we acquire or its parent, which could cause professionals

who join us from an acquired company to leave us. |

| |

|

|

| |

● |

Due

to fluctuations in our stock price, acquisition candidates may be reluctant to accept our ordinary shares as purchase price consideration,

use of our shares as purchase price consideration may be dilutive or the owners of certain companies we seek to acquire may insist

on stock price guarantees. |

Risks

Related to Our Corporate Structure. See “Item 3. Key Information — Risk Factors — Risks Related to Our

Corporate Structure” starting on page 22 of this Annual Report.

We

are also subject to risks and uncertainties related to our corporate structure, including, but not limited to, the following:

| |

● |

We

may rely on dividends and other distributions on equity paid by our subsidiaries to fund any cash and financing requirements we may

have, and any limitation on the ability of our subsidiaries to make payments to us could have a material adverse effect on our ability

to conduct our business. |

| |

|

|

| |

● |

Although

we currently have no operations in mainland China and we believe that we are not subject to the Chinese government’s direct

influence or discretion over the manner in which we conduct our business activities outside of mainland China, there is no guarantee

that the PRC government will not seek to intervene or influence GEL’s operations at any time. If GEL were to become subject

to such oversight, discretion or control, including over overseas offerings of securities and/or foreign investments, it may result

in a material adverse change in GEL’s operations, significantly limit or completely hinder GE Group’s ability to offer

or continue to offer securities to investors and cause the value of GE Group’s securities to significantly decline or be worthless,

which would materially affect the interests of the investors. There also can be no assurance that the PRC government will not intervene

or impose restrictions on GE Group’s ability to transfer or distribute cash within its organization, which could result in

an inability or prohibition on making transfers or distributions to entities outside of Hong Kong and adversely affect its business. |

| |

|

|

| |

● |

There

remain some uncertainties as to whether we will be required to obtain approvals from Chinese authorities to offer securities in the

future, and if required, we cannot assure you that we will be able to obtain such approval. |

| |

● |

Our

lack of effective internal controls over financial reporting may affect our ability to accurately report our financial results or

prevent fraud which may affect the market for and price of our Ordinary Shares. |

| |

● |

If

we cease to qualify as a foreign private issuer, we would be required to comply fully with the reporting requirements of the Exchange

Act applicable to U.S. domestic issuers, and we would incur significant additional legal, accounting and other expenses that we would

not incur as a foreign private issuer. |

| |

● |

We

are an “emerging growth company” within the meaning of the Securities Act, and if we take advantage of certain exemptions

from disclosure requirements available to emerging growth companies, this could make it more difficult to compare our performance

with other public companies. |

| |

|

|

| |

● |

As

an “emerging growth company” under applicable law, we will be subject to lessened disclosure requirements. Such reduced

disclosure may make our Ordinary Shares less attractive to investors. |

| |

● |

We

will incur increased costs as a result of being a public company, particularly after we cease to qualify as an “emerging growth

company.” |

| |

● |

Our

board of directors may decline to register transfers of Ordinary Shares in certain circumstances. |

Risks

Related to Doing Business in Hong Kong. See “Item 3. Key Information — Risk Factors — Risks Related to Doing

Business in Hong Kong” starting on page 25 of this Annual Report.

Substantially

all of our operations are in Hong Kong, so we face risks and uncertainties related to doing business in Hong Kong in general, including,

but not limited to, the following:

| |

● |

Although we and our subsidiaries

are not based in mainland China and we have no operations in mainland China, in light of the PRC government’s recent expansion

of authority in Hong Kong, we may be subject to uncertainty about any future actions of the PRC government or authorities in Hong

Kong, and it is possible that all the legal and operational risks associated with being based in and having operations in the PRC

may also apply to operations in Hong Kong in the future. There is no assurance that there will not be any changes in the economic,

political and legal environment in Hong Kong. The PRC government may intervene or influence our current and future operations in

Hong Kong at any time, or may exert more control over offerings conducted overseas and/or foreign investment in issuers like ourselves.

Such governmental actions, if and when they occur: (i) could significantly limit or completely hinder our ability to continue our

operations; (ii) could significantly limit or hinder our ability to offer or continue to offer our Ordinary Shares to investors;

and (iii) may cause the value of our Ordinary Shares to significantly decline or become worthless. |

| |

|

|

| |

● |

There remain some uncertainties

as to whether we will be required to obtain approvals from Chinese authorities to offer securities in the future, and if required,

we cannot assure you that we will be able to obtain such approval. |

| |

|

|

| |

● |

It may be difficult for

overseas shareholders and/or regulators to conduct investigation or collect evidence within China. |

| |

|

|

| |

● |

A substantial part of GEL’s

operations are in Hong Kong. However, due to the long arm provisions under the current PRC laws and regulations, the Chinese government

may exercise significant oversight and discretion over the conduct of our business and may intervene in or influence our operations

at any time, which could result in a material change in our operations and/or the value of our Ordinary Shares. The PRC government

may also intervene or impose restrictions on our ability to move money out of Hong Kong to distribute earnings and pay dividends

or to reinvest in our business outside of Hong Kong. Changes in the policies, regulations, rules, and the enforcement of laws of

the Chinese government may also be quick with little advance notice and our assertions and beliefs of the risk imposed by the PRC

legal and regulatory system cannot be certain. |

| |

|

|

| |

● |

You may incur additional

costs and procedural obstacles in effecting service of legal process, enforcing foreign judgments or bringing actions in Hong Kong

against us or our management named in this Annual Report based on Hong Kong laws. |

| |

● |

The enactment of Law of

the PRC on Safeguarding National Security in the Hong Kong Special Administrative Region (the “Hong Kong National Security

Law”) could impact our Hong Kong holding subsidiary. |

| |

● |

There are political risks

associated with conducting business in Hong Kong. |

| |

● |

We may be affected by the

currency peg system in Hong Kong. |

Risks

Related to Our Ordinary Shares. See “Item 3. Key Information — Risk Factors — Risks Related to Our Ordinary

Shares” starting on page 33 of this Annual Report.

In

addition to the risks described above, we are subject to general risks and uncertainties related to our Ordinary Shares, including, but

not limited to, the following:

| |

● |

Although the audit report

included in this Annual Report is prepared by U.S. auditors who are subject to PCAOB inspections on a regular basis, there is no

guarantee that future audit reports will be prepared by auditors inspected by the PCAOB and, as such, in the future investors may

be deprived of the benefits of such inspection. Furthermore, trading in our securities may be prohibited under the HFCA Act if the

SEC subsequently determines our audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely,

and as a result, U.S. national securities exchanges, such as the Nasdaq, may determine to delist our securities. Furthermore, on

June 22, 2021, the U.S. Senate passed the AHFCAA, which, if enacted, would amend the HFCA Act and require the SEC to prohibit an

issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive

years instead of three, thus reducing the time period for triggering the prohibition on trading. |

| |

● |

The recent

joint statement by the SEC, proposed rule changes submitted by Nasdaq, and an act passed by the U.S. Senate and the U.S. House of

Representatives, all call for additional and more stringent criteria to be applied to emerging market companies. These developments

could add uncertainties to our business operations, share price and reputation. |

| |

● |

Our Ordinary

Shares may be thinly traded and you may be unable to sell at or near ask prices or at all if you need to sell your Ordinary Shares

to raise money or otherwise desire to liquidate your shares. |

| |

● |

The market price for our

shares may be volatile. |

| |

|

|

| |

● |

Volatility in the price

of our Ordinary Shares may subject us to securities litigation. |

| |

● |

Substantial future sales

of our Ordinary Shares or the anticipation of future sales of our Ordinary Shares in the public market could cause the price of our

Ordinary Shares to decline. |

| |

● |

We do

not intend to pay dividends for the foreseeable future. |

| |

|

|

| |

● |

The market

price for our Ordinary Shares may be volatile. |

| |

● |

As a foreign private issuer,

we are permitted to, and we will, rely on exemptions from certain Nasdaq Stock Exchange corporate governance standards applicable

to domestic U.S. issuers. This may afford less protection to holders of our shares. |

| |

|

|

| |

● |

If we cease to qualify

as a foreign private issuer, we would be required to comply fully with the reporting requirements of the Exchange Act applicable

to U.S. domestic issuers, and we would incur significant additional legal, accounting and other expenses that we would not incur

as a foreign private issuer. |

| |

|

|

| |

● |

We may experience extreme

stock price volatility unrelated to our actual or expected operating performance, financial condition or prospects, making it difficult

for investors to assess the rapidly changing value of our Ordinary Shares. |

RISK

FACTORS

Risks

Related to Our Business

Changes

in capital markets, merger and acquisition activity, legal or regulatory requirements, general economic conditions and monetary or geopolitical

disruptions, as well as other factors beyond our control, could reduce demand for our practice offerings or services, in which case our

revenues and profitability could decline.

Different

factors outside of our control could affect demand for a segment’s practices and our services. These include:

| |

● |

fluctuations in U.S. and/or global economies, including economic downturns or recessions and the strength and rate of any general economic recoveries; |

|

● |

level of leverage incurred by countries or businesses; |

|

● |

merger and acquisition activity; |

|

● |

frequency and complexity of significant commercial litigation; |

|

● |

over

expansion by businesses causing financial difficulties; |

|

● |

business and management crises, including the occurrence of alleged fraudulent or illegal activities and practices; |

|

● |

new and complex laws and regulations, repeals of existing laws and regulations or changes of enforcement of laws, rules and regulations, including antitrust/competition reviews of proposed merger and acquisition transactions; |

|

● |

other economic, geographic or political factors; and |

|

● |

general business conditions. |

We

are not able to predict the positive or negative effects that future events or changes to the U.S. or global economies will have on our

business or the business of any particular segment. Fluctuations, changes and disruptions in financial, credit, merger and acquisition

and other markets, political instability and general business factors could impact various segments’ operations and could affect

such operations differently. Changes to factors described above, as well as other events, including by way of example, contractions of

regional economies, or the economy of a particular country, trade restrictions, monetary systems, banking, real estate and retail or

other industries; debt or credit difficulties or defaults by businesses or countries; new, repeals of or changes to laws and regulations,

including changes to the bankruptcy and competition laws of the U.S. or other countries; tort reform; banking reform; a decline in the

implementation or adoption of new laws or regulation, or in government enforcement, litigation or monetary damages or remedies that are

sought; or political instability may have adverse effects on one or more of our segments or service, practice or industry offerings.

Our

revenues, operating income and cash flows are likely to fluctuate.

We

experience fluctuations in our revenues and cost structure and the resulting operating income and cash flows and expect that this

will continue to occur in the future. We may experience fluctuations in our annual and quarterly financial results, including

revenues, operating income and earnings per share, for reasons that may include: (i) the types and complexity, number, size, timing

and duration of client engagements; (ii) the timing of revenue recognition under U.S. GAAP; (iii) the utilization of

revenue-generating professionals, including the ability to adjust staffing levels up or down to accommodate the business and

prospects of the applicable segment and practice; (iv) the geographic locations of our clients or the locations where services are

rendered; (v) billing rates and fee arrangements, including the opportunity and ability to successfully reach milestones and

complete, and collect success fees and other outcome-contingent or performance-based fees; (vi) the length of billing and collection

cycles and changes in amounts that may become uncollectible; (vii) changes in the frequency and complexity of government regulatory

and enforcement activities; (viii) business and asset acquisitions; (ix) fluctuations in the exchange rates of various currencies

against the U.S. dollar; (x) fee adjustments upon the renewal of expired service contracts or acceptance of new clients due to the

adjusted scope per our refined business strategy; and (xi) economic factors beyond our control.

The

results of different segments and practices may be affected differently by the above factors. The positive effects of certain events

or factors on certain segments and practices may not be sufficient to overcome the negative effects of those same events or factors on

other parts of our business. In addition, our mix of practice offerings adds complexity to the task of predicting revenues and results

of operations and managing our staffing levels and expenditures across changing business cycles and economic environments.

Our

results are subject to seasonal and other similar factors. While we assess our annual guidance at the end of each quarter and update

such guidance when we think it is appropriate, unanticipated future volatility can cause actual results to vary significantly from our

guidance, even where that guidance reflects a range of possible results and has been updated to take account of partial-year results.

We

have a substantial customer concentration, with a limited number of customers accounting for a substantial portion of our revenues.

We derive a significant

portion of our revenues from a few major customers. For the year ended June 30, 2024, three major third-party customers, (i)

Intellino Tech Sdn Bhd; (ii) VNET Group, Inc.; and (iii) Aisly Global Inc., accounted for 63.3%, 15.8% and 15.7%, respectively, of

the Company’s total revenues. For the year ended June 30, 2023, three major third-party customers, (i) VNET Group, Inc.; (ii)

Teligent International Limited; and (iii) Aisly Global Inc., accounted for 33.9%, 15.5% and 13.2%, respectively, of the

Company’s total revenues, and one related-party customer, China Information Technology Development Limited (the Company has

entered into separate agreements with each of Macro Systems Limited and DataCube Research Centre Limited and the revenues derived

from these two entities have been consolidated and reported under their parent company China Information Technology Development

Limited), accounted for 19.0% of the Company’s total revenues. For the year ended June 30, 2022, two major third-party

customers, (i) VNET Group, Inc.; and (ii) Aisly Global Inc., accounted for 33.1% and 23.8%, respectively, of the Company’s

total revenues, and one related-party customer, China Information Technology Development Limited, accounted for 21.9% of the

Company’s total revenues. The contract with Intellino Tech Sdn Bhd, dated June 1, 2023, as amended, has a term of twelve

months and expired on May 31, 2024 and the second contract, dated August 9, 2024 has a term of 3 months and will expire on November

14, 2024. The contract with 21Vianet Group Limited, dated October 4, 2019, has a term of approximately seven years and six months

and will expire on March 31, 2027. The contract with Diyixian.com Limited, dated January 1, 2020, has a term of one year and

expired on December 31, 2020, after which we continue to provide services to the customer without a written agreement on a periodic

basis. The contract with Teligent International Limited, dated June 1, 2023, has a term of one month and expired on June 30,

2023. We have entered into two (2) contacts with Aisly Global Inc. The first contract, originally dated January 1, 2021, as amended,

has a term of 23 months and expired on November 30, 2022 and the second contract, dated August 30, 2023, has a term of 8 months and

expired on April 30, 2024. We had four (4) contracts with Macro Systems Limited including one contract dated September 1, 2020

(expired June 30, 2021), one contract dated March 19, 2021 (expired on December 31, 2021), one contract dated March 19, 2021

(expired on June 30, 2022) and one contract dated March 1, 2021 (expired on December 31, 2022). The contract with DataCube Research Center Limited, originally dated August 27, 2021, as amended, had a

term of 24 months, was originally set to expire on March 31, 2024, but said contract was terminated on September 30, 2023.

Inherent

risks exist whenever a large percentage of total revenues are concentrated with a limited number of customers. It is not possible for

us to predict the future level of demand for our products and services that will be generated by these customers or the future demand

for our products by these customers in the marketplace. If any of these customers experience declining or delayed sales due to market,

economic or competitive conditions, we could be pressured to reduce our prices or they could decrease the purchase quantity of our products

and services, which could have an adverse effect on our margins and financial position, and could negatively affect our revenues and

results of operations. If any of our largest customers terminates the purchase of our products and services, such termination would materially

negatively affect our revenues, results of operations and financial condition.

Many

of our customers have entered into short-term contracts, with terms of one year or less, which do not provide for automatic renewal and

require the customer to opt-in to extend the term. Our customers have no obligation to renew, upgrade, or expand their agreements

with us after the terms of their existing agreements have expired. If one or more of our customers terminate their contracts with us,

whether for convenience, for default in the event of a breach by us, or for other reasons specified in our contracts, as applicable;

if our customers elect not to renew their contracts with us; or if our customers renew their contractual arrangements with us for shorter

contract lengths or for a reduced scope; our business and results of operations could be adversely affected. This adverse impact would

be even more pronounced for customers that represent a material portion of our revenue or business operations.

We

are exposed to the credit risks of our customers.

Our

financial position and profitability are dependent on our customers’ creditworthiness. Thus, we are exposed to our customers’

credit risks. There is no assurance that we will not encounter doubtful or bad debts in the future. Due to economic conditions in Hong

Kong, in particular the risk of monetary and fiscal policies to address inflation, businesses in Hong Kong are generally conserving cash

or under increased financial and credit stress. As a result, we could experience slower payments from our customers and borrowers, an

increase in accounts receivable aging and/or an increase in bad debts. If we were to experience any unexpected delay or difficulty in

collections from our customers or borrowers, our cash flows and financial results would be adversely affected.

We

rely on a limited number of vendors. A loss of any of these vendors could significantly negatively affect our business.

We rely on a limited number

of vendors. For the year ended June 30, 2024, two vendors, (i) Nexsen Limited; and (ii) MDT Innovations (Labuan) Ltd. accounted

for 77.7% and 17.4%, respectively, of the Company’s total purchases. For the year ended June 30, 2023, two vendors, (i) Nexsen Limited;

and (ii) MDT Innovations (Labuan) Ltd. accounted for 73.0% and 17.2%, respectively, of the Company’s total purchases. For the year

ended June 30, 2022, three vendors, (i) MDT Innovations Sdn Bdh and MDT Innovations (Labuan) Ltd.; (ii) Nexsen Limited; and (iii) FlexStream

Asia Limited, accounted for 40.2%, 34.9% and 12.5%, respectively, of the Company’s total purchases. The contracts with Logic Network

Limited for different services, dated November 1, 2019, May 1, 2020 and November 15, 2021 will expire or expired on March 31, 2027 (for

a term of seven years and four months), December 31, 2020 (for a term of eight months) and November 14, 2022 (for a term of one year),

respectively. We had four contracts with Nexsen Limited including one dated January 2, 2020 (expired on December 31, 2020); one dated

July 2, 2021 (expired on June 30, 2022); one dated April 1, 2022 (expired on March 31, 2024) and one dated September 25, 2023 (expired

on March 31, 2024).. The contract with Flexstream Asia Limited, dated June 1, 2021, had a term of 13 months and expired on June 30, 2022,

after which Flexstream Asia Limited continues to provide services to us on a monthly basis. We had entered into five contracts with MDT

Innovations Sdn Bdh for different services: one dated September 1, 2020 for ten months (expired on June 30, 2021), one dated December

15, 2020 for six months (expired on June 30, 2021), one dated April 17, 2021 for eight and a half months (expired on December 31, 2021),

one on July 2, 2021 for twelve months (expired on June 30, 2022), and one on September 29, 2021 (for a term from July 1, 2021 to December

31, 2021). We previously had a contract with Intelino Sdn Bhd, dated November 16, 2020, with a term of approximately seven and a half

months which expired on June 30, 2021. We entered into two (2) contracts with MDT Innovation (Labuan) Ltd: one contract dated August 30,

2023, which has a term of 8 months and will expire on April 30, 2024, and one contract dated January 2, 2022, which has a term of 12 months

and expired on December 31, 2022. This reliance on a limited number of vendors increases our risks, since we do not currently have

proven reliable alternatives or replacement vendors beyond these key vendors. If we experience a significant increase in demand of our

products, or if we need to replace an existing vendor, we may not be able to supplement service or replace them on acceptable terms, which

may undermine our ability to deliver products to customers in a timely manner. Identifying and approving suitable vendors could be an

extensive process that requires us to become satisfied with their quality control, technical capabilities, responsiveness and service,

financial stability, regulatory compliance, and labor and other ethical practices. Accordingly, a loss of any significant vendor would

have an adverse effect on our business, financial condition and results of operations. In addition, our vendors may face supply chain

risks and constraints of their own, which may impact the availability and pricing of our products as well as our gross margins.

Inadequate

or inaccurate external and internal information, including budget and planning data, could lead to inaccurate financial forecasts and

inappropriate financial decisions.

Our

financial forecasts are dependent on estimates and assumptions regarding budget and planning data, market growth, foreign exchange rates

and our ability to generate sufficient cash flow to reinvest in the business, fund internal growth, and meet our debt obligations. Our

financial projections are based on historical experience and on various other assumptions that our management believes to be reasonable

under the circumstances and at the time they are made. However, if our external and internal information is inadequate, our actual results

may differ materially from our forecasts and cause us to make inappropriate financial decisions. Any material variation between our financial

forecasts and our actual results may also adversely affect our future profitability, stock price and stockholder confidence.

We

may fail to innovate or create new solutions which align with changing market and customer demand.

As

a provider of integrated solutions, which involve the offering of products and services consisting of (i) providing comprehensive services

to telecom operators, (ii) offering business planning, development, technical and operations consulting programs to cloud and data center

providers, and (iii) offering system design, planning, development and operation services to technology companies, we expect to encounter

some of the challenges, risks, difficulties, and uncertainties frequently encountered by companies providing such products and services

in rapidly evolving markets. Some of these challenges include our ability to increase the total number of users of our services or adapt

to meet changes in our markets and competitive developments. Our personnel must continually stay current with vendor and marketplace

technology advancements, create solutions which may integrate evolving vendor products and services as well as services and solutions

we provide, to meet changing marketplace and customer demand. Our failure to innovate and provide value to our customers may erode our

competitive position and market share and may lead to a decrease in revenue and financial performance.

In

all of our markets, some of our competitors have greater financial, technical, marketing, and other resources than we do. In addition,

some of these competitors may be able to respond more quickly to new or changing opportunities, technologies, and customer requirements.

Many current and potential competitors engage in more extensive promotional marketing and advertising activities, offer more attractive

terms to customers, and adopt more aggressive pricing and credit policies than we do. We may not be successful in achieving revenue growth,

which may have a material adverse effect on our future operating results as a whole.

Our

business may face risks of clients’ default on payment.

Some

of our clients are businesses experiencing or being exposed to potential financial distress, facing complex challenges, being involved

in litigation or regulatory proceedings, or facing foreclosure of collateral or liquidation of assets. The aforementioned situations

may become increasingly prevalent among our existing and potential clients in light of the current uncertain micro-economic conditions

and/or potential economic slowdowns or recessions caused by COVID-19. Such clients may not have sufficient funds to continue operations

or to pay for our services. We do not always receive retainers before we begin performing services. In the cases where we have received

retainers, we cannot assure that the retainers will adequately cover our fees for the services we perform.

We

generally offer a fixed fee arrangement on our fees. Our failure to manage the engagements efficiently or collect the fees could expose

us to a greater risk of loss on such engagements. Providing services to clients that do not correlate to actual costs incurred may negatively

impact our profitability on such engagements and adversely affect the financial results of our business. We treat the outstanding fees

that we are unable to collect based on objective evidence as write-offs and will not adjust or accept renegotiation. Our fees set forth

in existing service contracts are not negotiable and may not be adjusted even if fee collection is not probable. Management periodically

monitors the outstanding fees, making an effort to timely collect outstanding fees and reviews the adequacy of write-offs to minimize

the impact of the potential payment defaults.

We

may not manage our growth effectively, and our profitability may suffer.

We

experience fluctuations in growth of our different segments, practices or services, including periods of rapid or declining growth. Periods

of rapid expansion may strain our management team or human resources and information systems. To manage growth successfully, we may need

to add qualified managers and employees and periodically update our operating, financial and other systems, as well as our internal procedures

and controls. We also must effectively motivate, train and manage a larger professional staff. If we fail to add or retain qualified

managers, employees and contractors when needed, estimate costs, or manage our growth effectively, our business, financial results and

financial condition may suffer.

We

cannot assure that we can successfully manage growth and being profitable as we grow. In periods of declining growth, underutilized

employees and contractors may result in expenses and costs being a greater percentage of revenues. In such situations, we will have to

weigh the benefits of decreasing our workforce or limiting our service offerings and saving costs against the detriment that we could

experience from losing valued professionals and their industry expertise and clients.

Our

reputation and brand recognition is crucial to our business. Any harm to our reputation or failure to enhance our brand recognition may

materially and adversely affect our business, financial condition and results of operations.

Our

reputation and brand recognition, which depends on earning and maintaining the trust and confidence of our current or potential clients,

is critical to our business. Our reputation and brand is vulnerable to many threats that can be difficult or impossible to control, and

costly or impossible to remediate. Regulatory inquiries or investigations, lawsuits initiated by clients or other third parties, employee

misconduct, perceptions of conflicts of interest and rumors, among other things, could substantially damage our reputation, even if they

are baseless or satisfactorily addressed. Moreover, any negative media publicity about our industry in general or product or service

quality problems of other firms in the industry, including our competitors, may also negatively impact our reputation and brand. If we

are unable to maintain a good reputation or further enhance our brand recognition, our ability to attract and retain clients and key

employees could be harmed and, as a result, our business and revenues would be materially and adversely affected.

We

may not be able to grow at the historical rate of growth, and if we fail to manage our growth effectively, our business may be materially

and adversely affected.

We

anticipate significant continuing growth in the foreseeable future. However, we cannot assure you that we will grow at the historical

rate of growth. Our rapid growth has placed, and will continue to place, a significant strain on our management, personnel, systems and

resources. To accommodate our growth, we will need to implement a variety of new and upgraded operational and systems procedures and

controls, including the improvement of our accounting and other internal management systems. We also will need to recruit, train, manage

and motivate employees and manage our relationships with an increasing number of clients. Moreover, as we introduce new services or enter

into new markets, we may face unfamiliar market and operational risks and challenges which we may fail to successfully address. We may

be unable to manage our growth effectively, which could have a material adverse effect on our business.

Our

limited operating history may not provide an adequate basis to judge our future prospects and results of operations.

Our

limited operating history makes the prediction of future results of operations difficult, and therefore, past results of operations achieved

by us should not be taken as indicative of the rate of growth, if any, that can be expected in the future. As a result, you should consider

our future prospects in light of the risks and uncertainties experienced by early stage companies in a rapidly evolving and increasingly

competitive market in Hong Kong.

We

may not be able to obtain or maintain all necessary licenses, permits and approvals and to make all necessary registrations and filings

for our activities in multiple jurisdictions and related to residents therein.

We

operate in an industry which is subject to regulation and may requires various licenses, permits and approvals in different jurisdictions

to conduct our businesses. Our customers include people who live in jurisdictions where we do not have licenses issued by the local regulatory

bodies. It is possible that authorities in those jurisdictions may take the position that we are required to obtain licenses or otherwise

comply with laws and regulations which we believe are not required or applicable to our business activities. If we fail to comply with

the regulatory requirements, we may encounter the risk of being disqualified for our existing businesses or being rejected for renewal

of our qualifications upon expiry by the regulatory authorities as well as other penalties, fines or sanctions. In addition, in respect

of any new business that we may contemplate, we may not be able to obtain the relevant approvals for developing such new business if

we fail to comply with the relevant regulations and regulatory requirements. As a result, we may fail to develop new business as planned,

or we may fall behind our competitors in such businesses.

A

failure in our information technology, or IT, systems could cause interruptions in our services, undermine the responsiveness of our

services, disrupt our business, damage our reputation and cause losses.

Our

IT systems support all phases of our operations, including marketing, customer development and the provision of customer support services,

and are an essential part of our technology infrastructure. If our systems fail to perform, we could experience disruptions in operations,

slower response time or decreased customer satisfaction. We must process, record and monitor a large number of transactions and our operations

are highly dependent on the integrity of our technology systems and our ability to make timely enhancements and additions to our systems.

System interruptions, errors or downtime can result from a variety of causes, including changes in customer usage patterns, technological

failures, changes to our systems, linkages with third-party systems and power failures. Our systems are vulnerable to disruptions from

human error, execution errors, errors in models such as those used for risk management and compliance, employee misconduct, unauthorized

trading, external fraud, computer viruses, distributed denial of service attacks, computer viruses or cyberattacks, terrorist attacks,

natural disaster, power outage, capacity constraints, software flaws, events impacting key business partners and vendors, and similar events.

It

could take an extended period of time to restore full functionality to our technology or other operating systems in the event of an unforeseen

occurrence, which could affect our ability to process and settle customer transactions. Moreover, instances of fraud or other misconduct

might also negatively impact our reputation and customer confidence in us, in addition to any direct losses that might result from such

instances. Despite our efforts to identify areas of risk, oversee operational areas involving risks, and implement policies and procedures

designed to manage these risks, there can be no assurance that we will not suffer unexpected losses, reputational damage or regulatory

actions due to technology or other operational failures or errors, including those of our vendors or other third parties.

If

we fail to prevent security breaches, improper access to or disclosure of our data or user data, or other hacking and attacks, we may

lose users, and our business, reputation, financial condition and results of operations may be materially and adversely affected.

Our

business involves the storage and transmission of proprietary information and sensitive or confidential data, including personal information

of its employees, customers and others. In addition, we operate data centers for its customers that host their technology infrastructure

and may store and transmit both business-critical data and confidential information. In connection with our services business, some of

our employees also have access to its customers’ confidential data and other information.

We

have privacy and data security policies in place that are designed to prevent security breaches and we have employed significant resources

to develop our security measures against breaches. However, as newer technologies evolve, and the portfolio of the service providers

with which the Company shares confidential information with grows, we could be exposed to increased risk of breaches in security and

other illegal or fraudulent acts, including cyberattacks. The evolving nature of such threats, in light of new and sophisticated methods

used by criminals and cyberterrorists, including computer viruses, malware, phishing, misrepresentation, social engineering and forgery,

is making it increasingly challenging to anticipate and adequately mitigate these risks.

We

are likely in the future to be subject to these types of attacks. If we are unable to avert these attacks and security breaches, we could

be subject to significant legal and financial liabilities, our reputation would be harmed and we could sustain substantial revenue loss

from lost sales and customer dissatisfaction. We may not have the resources or technical sophistication to anticipate or prevent rapidly

evolving types of cyber-attacks. Cyber-attacks may target us, our suppliers, customers or other participants, or the internet infrastructure

on which we depend. Actual or anticipated attacks and risks may cause us to incur significantly higher costs, including costs to deploy

additional personnel and network protection technologies, train employees, and engage third-party experts and consultants. As we

do not carry cybersecurity insurance, we will not be able to mitigate such risks to any third party. Cybersecurity breaches would not

only harm our reputation and business, but also could materially decrease our revenue and net income.

We

may not be able to protect our intellectual property rights.

We

cannot make assurances that the steps we have taken to protect our intellectual property rights will be adequate to deter misappropriation

of proprietary information or that we will be able to detect unauthorized use and take appropriate steps to enforce our intellectual

property rights.

We

may be subject to intellectual property infringement claims, which may be expensive to defend and may disrupt our business and operations.

We

cannot be certain that our operations or any aspects of our business do not or will not infringe upon or otherwise violate trademarks,

copyrights, know-how or other intellectual property rights held by third parties. We may be from time to time in the future subject to

legal proceedings and claims relating to the intellectual property rights of others. In addition, there may be third-party trademarks,

copyrights, know-how or other intellectual property rights that are infringed by our products, services or other aspects of our business

without our awareness. Holders of such intellectual property rights may seek to enforce such rights against us in Hong Kong, the United

States or other jurisdictions. If any third-party infringement claims are brought against us, we may be forced to divert some resources

from our business and operations to defend against these claims, regardless of their merits.

Additionally,

the application and interpretation of Hong Kong’s intellectual property rights laws and the procedures and standards for granting

trademarks, copyrights, know-how or other intellectual property rights in Hong Kong are still evolving and are uncertain, and we cannot

ensure that Hong Kong courts or regulatory authorities would agree with our analysis. If we were found to be in violation of the intellectual

property rights of others, we may be subject to liability for our infringement activities or may be prohibited from using such intellectual

property, and we may incur licensing fees or be forced to develop alternatives of our own. As a result, our business and operating results

may be materially and adversely affected.

Compromise

of confidential or proprietary information could damage our reputation, harm our businesses and adversely impact our financial results.

Our

own confidential and proprietary information and that of our clients could be compromised, whether intentionally or unintentionally,

by our employees, consultants or vendors. A compromise of the security of our information technology systems leading to theft or misuse

of our own or our clients’ proprietary or confidential information, or the public disclosure or use of such information by others,

could result in losses, third-party claims against us and reputational harm, including the loss of clients. The theft or compromise of

our or our clients’ information could negatively impact our reputation, financial results and prospects. In addition, if our reputation

is damaged due to a data security breach, our ability to attract new engagements and clients may be impaired or we may be subjected to

damages or penalties, which could negatively impact our businesses, financial results or financial condition.

Increases

in labor costs in Hong Kong may adversely affect our business and results of operations.

The

economy in Hong Kong has experienced increases in inflation and labor costs in recent years. As a result, average wages in Hong Kong

are expected to continue to increase. In addition, we are required by Hong Kong laws and regulations to maintain various statutory employee

benefits, including mandatory provident fund scheme and work-related injury insurance, to provide statutorily required paid sick leave,

annual leave and maternity leave, and pay severance payments or long service payments. The relevant government agencies may examine whether

an employer has complied with such requirements, and those employers who fail to comply commit a criminal offence and may be subject

to fines and/or imprisonment. We expect that our labor costs, including wages and employee benefits, will continue to increase. Unless

we are able to control our labor costs or pass on these increased labor costs to our users by increasing the fees of our services, our

financial condition and operating results may be adversely affected.

We

do not have any business insurance coverage.

Currently,

we do not have any business liability or disruption insurance to cover our operations. We have determined that the costs of insuring

for these risks and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for

us to have such insurance. Any uninsured business disruptions may result in our incurring substantial costs and the diversion of resources,

which could have an adverse effect on our results of operations and financial condition.

Our

principal shareholders have substantial influence over our company and their interests may not be aligned with the interests of our other

shareholders

Andrew, LEE Yat Lung (“Mr.

Lee”) is currently the beneficial owner of 6,960,000 Ordinary Shares or 38.0% of our outstanding shares. Mr. Lee will be able to

exert significant voting influence over our business, including decisions regarding mergers, consolidations and the sale of all or substantially

all of our assets, election of directors and other significant corporate actions. These actions may be taken even if they are opposed

by our other shareholders, including our public shareholders. Moreover, this concentration of ownership may discourage, delay or prevent

a change in control of our company, which could deprive our shareholders of an opportunity to receive a premium for their shares as part

of a sale of our Company and might reduce the price of our Ordinary Shares.

We

face risks related to natural disasters, health epidemics and other outbreaks, which could significantly disrupt our operations.

We

are vulnerable to natural disasters and other calamities. Fire, floods, typhoons, earthquakes, power loss, telecommunications

failures, break-ins, war, riots, terrorist attacks or similar events may give rise to server interruptions, breakdowns, system

failures, technology platform failures or internet failures, which could cause the loss or corruption of data or malfunctions of

software or hardware as well as adversely affect our ability to provide products and services on our platform. In addition, our

results of operations could be adversely affected to the extent that any health epidemic harms the Hong Kong economy in general. A

prolonged outbreak of any illnesses or other adverse public health developments in Hong Kong or elsewhere in the world could have a

material adverse effect on our business operations. Such outbreaks could severely disrupt our operations and adversely affect our

business, financial condition and results of operations. Our headquarter is located in Hong Kong, where our management and employees

currently reside. Consequently, if any natural disasters, health epidemics or other public safety concerns were to affect Hong Kong

or cause travel restriction in or out of Hong Kong or its surrounding areas, our operation may experience material disruptions,

which may materially and adversely affect our business, financial condition and results of operations. On February 24, 2022, the

Russian Federation launched an invasion of Ukraine that has had an immediate impact on the global economy resulting in higher energy

prices and higher prices for certain raw materials and goods and services which in turn is contributing to higher inflation in the

United States and other countries across the globe with significant disruption to financial markets. We do not have any operation or

business in Russia or Ukraine, however, we may potentially be indirectly adversely impacted any significant disruption it has caused

and may continue to escalate. Any one or more of these events may impede our operation and delivery efforts and adversely affect our

sales results, or even for a prolonged period of time, which could materially and adversely affect our business, financial

condition, and results of operations.

Although our business operations so far

have not been materially and adversely affected by the outbreak of the coronavirus (COVID-19) due to our business nature, there can be

no assurance that our business operations will not be materially and adversely affected by the continuous effect of the COVID-19 pandemic

in the future.

An outbreak of respiratory

illness caused by the novel coronavirus, commonly referred as “COVID-19” emerged in late 2019 and has spread globally. COVID-19

is considered to be highly contagious and poses a serious public health threat. The World Health Organization labeled the COVID-19 outbreak

as a pandemic on March 11, 2020, given its threat beyond a public health emergency of international concern the organization had declared

on January 30, 2020.

In response to the COVID-19

outbreak, the governments of many countries, states, cities and other geographic regions have taken preventative or protective actions,

such as imposing restrictions on travel and business operations. Temporary closures of businesses have been ordered and numerous

other businesses have temporarily closed voluntarily. These actions may continue to expand in scope, type and impact. These measures,

while intended to protect human life, are expected to have significant adverse impacts on domestic and foreign economies of uncertain

severity and duration. It is likely that the current outbreak or continued spread of COVID-19 will cause an economic slowdown, which may

result in a global recession. The effectiveness of economic stabilization efforts being taken to mitigate the effects of the COVID-19

outbreak is currently uncertain.

A public health pandemic,

including COVID-19, potentially poses the risk that the Company or its affiliates, employees, suppliers, customers and others may be prevented

from conducting business activities for an indefinite period of time, including as a result of shutdowns, travel restrictions and other

actions that may be requested or mandated by governmental authorities. Such actions may prevent the Company from accessing the facilities

of its customers to deliver products and provide services. In addition, our customers may choose to delay or abandon projects on which

we provide products and/or services as a result of such actions.

Although the COVID-19 outbreak

so far has not materially disrupted our business operations due to the nature of our business being based on technical platform and resources

(unlike the manufacturing industry, for example), there can be no assurance that it will not materially and adversely affect us, our employees,

suppliers, or customers in the future. For example, if a significant number of our employees, or employees and third parties performing

key functions, including our CEO and members of our board of directors, become ill, our business may be further adversely impacted. In

addition, we have modified our business practices (including employee travel, employee work locations, and cancellation of physical participation

in meetings, events and conferences), and we may take further actions as may be required by government authorities or that we determine

are in the best interests of our employees, customers, partners, and suppliers. Such modified business practices (including the extension

of remote work arrangements) could pose challenges to our employees and our IT systems and increase operational risk, including cyber

security and IT systems management risks, and impair our ability to manage our business. An increase in operational challenges could have

a material and adverse effect on our business, financial conditions, and results of operations.

Our liquidity could be negatively

impacted if these conditions continue for a significant period of time and we may be required to pursue additional sources of financing

to obtain working capital, maintain appropriate inventory levels and meet our financial obligations. Our ability to obtain any required

financing is not guaranteed and largely dependent upon evolving market conditions and other factors. Depending on the continued impact

of the COVID-19 outbreak, further actions may be required to improve our cash position and capital structure. We cannot assure you that

we would be able to take any of these actions on terms that are favorable to us or at all, that these actions would be successful and

permit us to meet our scheduled debt service obligations or satisfy our capital requirements, or that these actions would be permitted

under the terms of our existing or future debt agreements.

We may also experience impacts

from market downturns and changes in demand for our products and services related to pandemic fears and impacts on our workforce as a

result of COVID-19. If the COVID-19 outbreak becomes more pronounced in our markets, or if another significant natural disaster or pandemic

were to occur in the future, our operations in areas impacted by such events could experience further adverse financial impacts due to

market changes and other resulting events and circumstances. The extent to which the COVID-19 outbreak impacts our results of operations,

financial condition and cash flows will depend on future developments that are highly uncertain and cannot be predicted, including new

information that may emerge concerning the severity of COVID-19, the longevity of COVID-19 and the actions to contain COVID-19 or treat

its impact, and how quickly and to what extent normal economic and operating conditions can resume. Although it is difficult to predict

the effect and ultimate impact of the COVID-19 outbreak on our business in the future, it is likely that the impact of COVID-19 may adversely

affect our results of operations, financial conditions and cash flows in the next fiscal year.

The effects of a subvariant

of the Omicron variant of COVID-19, which may spread faster than the original Omicron variant, as well as the effects of any new variants

and subvariants which may develop, including any actions taken by governments, may have the effect of slowing our sales in Hong Kong.

Furthermore, even after the

COVID-19 outbreak has subsided, we may experience impacts to our business as a result of the global economic impact of the COVID-19 outbreak,

including any economic downturn or recession or other long-term effects that have occurred or may occur to us, our customers and vendors

in the future.

Failure to comply

with laws and regulations applicable to our business could subject us to fines and penalties and could also cause us to lose customers

or otherwise harm our business.

Our

business is subject to regulation by various governmental agencies in Hong Kong, including agencies responsible for monitoring and enforcing

compliance with various legal obligations, such as privacy and data protection-related laws and regulations, intellectual property laws,

employment and labor laws, workplace safety, governmental trade laws, import and export controls, anti-corruption and anti-bribery laws,

and tax laws and regulations. In certain jurisdictions, these regulatory requirements may be more stringent than in Hong Kong. These laws

and regulations impose added costs on our business. Noncompliance with applicable regulations or requirements could subject us to:

| ● | investigations, enforcement

actions, and sanctions; |

| ● | mandatory changes to our network

and products; |

| |

● |

disgorgement of profits, fines, and damages; |

| |

|

|

| |

● |

civil and criminal penalties or injunctions; |

| ● | claims for damages by our customers

or channel partners; |

| ● | termination of contracts; |

| ● | failure to obtain, maintain

or renew certain licenses, approvals, permits, registrations or filings necessary to conduct our operations; and |

| ● | temporary or permanent debarment

from sales to public service organizations. |

If

any governmental sanctions are imposed, or if we do not prevail in any possible civil or criminal litigation, our business, results of

operations, and financial condition could be adversely affected. In addition, responding to any action will likely result in a significant

diversion of our management’s attention and resources and an increase in professional fees. Enforcement actions and sanctions could

materially harm our business, results of operations, and financial condition.

Any

reviews by regulatory agencies or legislatures may result in substantial regulatory fines, changes to our business practices, and other

penalties, which could negatively affect our business and results of operations. Changes in social, political, and regulatory conditions

or in laws and policies governing a wide range of topics may cause us to change our business practices. Further, our expansion into a

variety of new fields also could raise a number of new regulatory issues. These factors could negatively affect our business and results

of operations in material ways.

Moreover,

we are exposed to the risk of misconduct, errors and failure to functions by our management, employees and parties with whom we collaborate,