false

FY

0001928581

P5Y

0001928581

2023-07-01

2024-06-30

0001928581

dei:BusinessContactMember

2023-07-01

2024-06-30

0001928581

2024-06-30

0001928581

2023-06-30

0001928581

us-gaap:RelatedPartyMember

2024-06-30

0001928581

us-gaap:RelatedPartyMember

2023-06-30

0001928581

2022-07-01

2023-06-30

0001928581

FTEL:MerchandiseRevenueMember

2023-07-01

2024-06-30

0001928581

FTEL:MerchandiseRevenueMember

2022-07-01

2023-06-30

0001928581

FTEL:SalesOfConsumableProductsMember

2023-07-01

2024-06-30

0001928581

FTEL:SalesOfConsumableProductsMember

2022-07-01

2023-06-30

0001928581

FTEL:RevenueFromLicensingCustomersMember

2023-07-01

2024-06-30

0001928581

FTEL:RevenueFromLicensingCustomersMember

2022-07-01

2023-06-30

0001928581

us-gaap:CommonStockMember

2022-06-30

0001928581

FTEL:SubscriptionReceivableMember

2022-06-30

0001928581

us-gaap:AdditionalPaidInCapitalMember

2022-06-30

0001928581

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-06-30

0001928581

us-gaap:RetainedEarningsMember

2022-06-30

0001928581

2022-06-30

0001928581

us-gaap:CommonStockMember

2023-06-30

0001928581

FTEL:SubscriptionReceivableMember

2023-06-30

0001928581

us-gaap:AdditionalPaidInCapitalMember

2023-06-30

0001928581

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-06-30

0001928581

us-gaap:RetainedEarningsMember

2023-06-30

0001928581

us-gaap:CommonStockMember

2022-07-01

2023-06-30

0001928581

FTEL:SubscriptionReceivableMember

2022-07-01

2023-06-30

0001928581

us-gaap:AdditionalPaidInCapitalMember

2022-07-01

2023-06-30

0001928581

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-07-01

2023-06-30

0001928581

us-gaap:RetainedEarningsMember

2022-07-01

2023-06-30

0001928581

us-gaap:CommonStockMember

2023-07-01

2024-06-30

0001928581

FTEL:SubscriptionReceivableMember

2023-07-01

2024-06-30

0001928581

us-gaap:AdditionalPaidInCapitalMember

2023-07-01

2024-06-30

0001928581

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-07-01

2024-06-30

0001928581

us-gaap:RetainedEarningsMember

2023-07-01

2024-06-30

0001928581

us-gaap:CommonStockMember

2024-06-30

0001928581

FTEL:SubscriptionReceivableMember

2024-06-30

0001928581

us-gaap:AdditionalPaidInCapitalMember

2024-06-30

0001928581

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-06-30

0001928581

us-gaap:RetainedEarningsMember

2024-06-30

0001928581

FTEL:FitellCorporationMember

2023-07-01

2024-06-30

0001928581

FTEL:FitellCorporationMember

2022-07-01

2023-06-30

0001928581

FTEL:KMASCapitalAndInvestmentPtyLtdMember

2023-07-01

2024-06-30

0001928581

FTEL:KMASCapitalAndInvestmentPtyLtdMember

2024-06-30

0001928581

FTEL:KMASCapitalAndInvestmentPtyLtdMember

2023-06-30

0001928581

FTEL:GDWellnessPtyLtdMember

2023-07-01

2024-06-30

0001928581

FTEL:GDWellnessPtyLtdMember

2024-06-30

0001928581

FTEL:GDWellnessPtyLtdMember

2023-06-30

0001928581

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

FTEL:OneVendorsMember

2023-07-01

2024-06-30

0001928581

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

FTEL:TwoVendorsMember

2023-07-01

2024-06-30

0001928581

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

FTEL:OneVendorsMember

2022-07-01

2023-06-30

0001928581

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

FTEL:TwoVendorsMember

2022-07-01

2023-06-30

0001928581

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

FTEL:ThreeVendorsMember

2022-07-01

2023-06-30

0001928581

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

FTEL:ThreeVendorsMember

2023-07-01

2024-06-30

0001928581

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

FTEL:FourVendorsMember

2022-07-01

2023-06-30

0001928581

FTEL:WarrantOneMember

2024-06-30

0001928581

FTEL:WarrantTwoMember

2024-06-30

0001928581

FTEL:WarrantOneMember

2023-07-01

2024-06-30

0001928581

FTEL:WarrantTwoMember

2023-07-01

2024-06-30

0001928581

us-gaap:EquitySecuritiesMember

2024-06-30

0001928581

us-gaap:EquitySecuritiesMember

2023-06-30

0001928581

us-gaap:EquitySecuritiesMember

us-gaap:FairValueInputsLevel1Member

us-gaap:FairValueMeasurementsRecurringMember

2024-06-30

0001928581

us-gaap:EquitySecuritiesMember

us-gaap:FairValueInputsLevel2Member

us-gaap:FairValueMeasurementsRecurringMember

2024-06-30

0001928581

us-gaap:EquitySecuritiesMember

us-gaap:FairValueInputsLevel3Member

us-gaap:FairValueMeasurementsRecurringMember

2024-06-30

0001928581

us-gaap:EquitySecuritiesMember

us-gaap:FairValueMeasurementsRecurringMember

2024-06-30

0001928581

us-gaap:FairValueInputsLevel1Member

us-gaap:FairValueMeasurementsRecurringMember

2024-06-30

0001928581

us-gaap:FairValueInputsLevel2Member

us-gaap:FairValueMeasurementsRecurringMember

2024-06-30

0001928581

us-gaap:FairValueInputsLevel3Member

us-gaap:FairValueMeasurementsRecurringMember

2024-06-30

0001928581

us-gaap:FairValueMeasurementsRecurringMember

2024-06-30

0001928581

us-gaap:EquitySecuritiesMember

us-gaap:FairValueInputsLevel1Member

us-gaap:FairValueMeasurementsRecurringMember

2023-06-30

0001928581

us-gaap:EquitySecuritiesMember

us-gaap:FairValueInputsLevel2Member

us-gaap:FairValueMeasurementsRecurringMember

2023-06-30

0001928581

us-gaap:EquitySecuritiesMember

us-gaap:FairValueInputsLevel3Member

us-gaap:FairValueMeasurementsRecurringMember

2023-06-30

0001928581

us-gaap:EquitySecuritiesMember

us-gaap:FairValueMeasurementsRecurringMember

2023-06-30

0001928581

us-gaap:FairValueInputsLevel1Member

us-gaap:FairValueMeasurementsRecurringMember

2023-06-30

0001928581

us-gaap:FairValueInputsLevel2Member

us-gaap:FairValueMeasurementsRecurringMember

2023-06-30

0001928581

us-gaap:FairValueInputsLevel3Member

us-gaap:FairValueMeasurementsRecurringMember

2023-06-30

0001928581

us-gaap:FairValueMeasurementsRecurringMember

2023-06-30

0001928581

FTEL:ConvertibleNotesMember

2024-01-15

0001928581

FTEL:ConvertibleNotesMember

2024-01-15

2024-01-15

0001928581

2024-01-15

0001928581

FTEL:WarrantTwoMember

FTEL:ConvertibleNotesMember

2024-01-15

0001928581

FTEL:ConvertibleNotesMember

2023-07-01

2024-06-30

0001928581

FTEL:ConvertibleNotesMember

2024-06-30

0001928581

us-gaap:WarrantMember

2024-06-30

0001928581

us-gaap:WarrantMember

2023-07-01

2024-06-30

0001928581

us-gaap:WarrantMember

2023-06-30

0001928581

us-gaap:WarrantMember

2023-07-01

2024-06-30

0001928581

us-gaap:WarrantMember

2024-06-30

0001928581

2023-08-02

0001928581

2023-08-02

2023-08-02

0001928581

us-gaap:VehiclesMember

2024-06-30

0001928581

us-gaap:VehiclesMember

2023-06-30

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

iso4217:AUD

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

(Mark

One)

FORM

20-F

| ☐ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OFTHE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ |

ANNUALREPORT

PURSUANT TO SECTION 13 OR 15(d) OFTHE SECURITIES EXCHANGE ACT OF 1934

For

the fiscal year ended June 30, 2024

|

OR

| ☐ |

TRANSITION REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☐ |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date

of event requiring this shell company report

For

the transition period from __________________ to ____________________

Commission

file number: 001-41774

FITELL

CORPORATION

(Exact

name of Registrant as specified in its charter)

Cayman

Islands

(Jurisdiction

of incorporation or organization)

23-25

Mangrove Lane

Taren

Point, NSW 2229

Australia

+612

95245266

(Address

of principal executive offices)

Cogency

Global Inc.

122

East 42nd Street, 18th Floor

New

York, NY 10168

(800)

221-0102

(Name,

Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to

Section 12(b) of the Act.

| Title

of each class |

|

Trading

Symbol(s) |

|

Name

of each exchange on which registered |

| Ordinary

Shares, par value $0.0001 per share |

|

FTEL |

|

The

Nasdaq Stock Market LLC |

Securities

registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title

of Class)

Securities

for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title

of Class)

Indicate

the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered

by the annual report.

20,123,386

Ordinary Shares were outstanding as of June 30, 2024.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒ No

If

this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section

13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒ No

Note

– Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities

Exchange Act of 1934 from their obligations under those Sections.

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

☒ Yes ☐ No

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth

company. See definition of “large accelerated filer, “accelerated filer,” and “emerging growth company”

in Rule 12b-2 of the Exchange Act.

| Large

accelerated filer ☐ |

Accelerated

filer ☐ |

Non-accelerated

filer ☐ |

| |

|

Emerging

growth company ☒ |

If

an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided

pursuant to Section 13(a) of the Exchange Act.

†

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards

Board to its Accounting Standards Codification after April 5, 2012.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the

effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.

7262(b) by the registered public accounting firm that prepared or issued its audit report. ☐

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether

any of those error corrections are restatements that required a recovery analysis of incentive- based compensation received by any of

the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-Indicate by check mark which

basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ |

International

Financial Reporting Standards as issued Other by the International Accounting Standards Board ☐ |

Other ☐ |

If

“Other” has been checked in response to the previous question, indicate by check mark which financial statement item the

registrant has elected to follow.

☐ Item

17 ☐ Item 18

If

this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange

Act).

☐ Yes ☒ No

(APPLICABLE

ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate

by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities

Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

Table

of Contents

Use

of Certain Defined Terms

Unless

otherwise indicated or the context requires otherwise, references in this annual report to:

●

“AUD” are to Australian Dollars, the legal currency of Australia;

●

“Companies Act” are to the Companies Act (Revised), as consolidated and revised, of the Cayman Islands;

●

“Exchange Act” are to the Securities Exchange Act of 1934, as amended;

●

“FINRA” are to the Financial Industry Regulatory Authority;

●

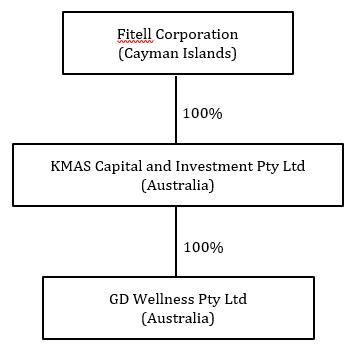

“Fitell,” “the Company,” “we,” “us,” or “our”

refer to Fitell Corporation, a Cayman Islands exempted company

incorporated

under the laws of Cayman Islands on April 11, 2022, and its consolidated subsidiaries, through

which it conducts its business;

●

“FY2022” are to the financial year ended June 30, 2022;

●

“FY2023” are to the financial year ended June 30, 2023;

●

“FY2024” are to the financial year ended June 30, 2024;

●

“GD” are to GD Wellness Ptd Ltd, a wholly-owned operating subsidiary of KMAS, incorporated under the laws of Australia on

July 22, 2005;

●

“IPO” are to the Company’s initial public offering which was consummated on August 10, 2023;

●

“KMAS” are to KMAS Capital and Investment Pty Ltd, a company incorporated under the laws of Australia on July 26, 2016, a

wholly-owned subsidiary of Fitell which holds all of the issued and outstanding shares of our operating subsidiary GD;

●

“$,” “U.S. dollars,” or “dollars” are to the legal currency of the United States;

●

“SEC” are to the Securities and Exchange Commission;

●

“Securities Act” are to the Securities Act of 1933, as amended;

●

“Shares”, “shares,” or “Ordinary Shares” are to the Ordinary Shares of Fitell Corporation, par value

$0.0001 per share; and

●

“SKMA”, are to a company owned by Ms. Jieting Zhao, incorporated under the laws of the British Virgin Islands.

Our

business is and has been conducted in Australia through our Australian subsidiary GD Wellness Pty Ltd since our inception, using Australian

dollars, the currency of Australia. Our financial statements are presented in United States dollars. In this annual report, we refer

to assets, obligations, commitments and liabilities in our financial statements in United States dollars. These dollar references are

based on the exchange rate of Australian dollars to United States dollars, determined as of a specific date or for a specific period.

Changes in the exchange rate will affect the amount of our obligations and the value of our assets in terms of United States dollars

which may result in an increase or decrease in the amount of our obligations (expressed in dollars) and the value of our assets.

CAUTIONARY

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This

annual report on Form 20-F contains forward-looking statements that involve risks and uncertainties, including statements relating to

our future financial performance and results, financial condition, business strategy, plans, goals and objectives, including certain

projections, milestones, targets, business trends, and other statements that are not historical facts. These forward-looking statements

are made under the “safe harbor” provision under Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange

Act, and as defined in the Private Securities Litigation Reform Act of 1995. These forward-looking statements generally are identified

by the words “budget,” “target,” “aim,” “strategy,” “guidance,” “outlook,”

“anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,”

“expect,” “believe,” “intend,” “may,” “should,” “will,” “could”

and similar expressions denoting uncertainty or an action that may, will or is expected to occur in the future; although, not all forward-looking

statements contain these identifying words. These statements involve estimates, assumptions, known and unknown risks, uncertainties and

other factors that could cause actual results to differ materially from any future results, performances or achievements expressed or

implied by the forward-looking statements.

Forward-looking

statements include, but are not limited to, statements concerning:

| |

● |

the

timing of the development of future services; |

| |

|

|

| |

● |

projections

of revenue, earnings, capital structure and other financial items; |

| |

|

|

| |

● |

statements

regarding the capabilities of our business operations; |

| |

|

|

| |

● |

statements

of expected future economic performance; |

| |

|

|

| |

● |

statements

regarding competition in our market; and |

| |

|

|

| |

● |

assumptions

underlying statements regarding us or our business. |

These

forward-looking statements are subject to a number of risks and uncertainties, including:

| |

● |

our

dependence on macroeconomic conditions and consumer discretionary spending; |

| |

|

|

| |

● |

the

intense competition in the gym and fitness equipment industry; |

| |

|

|

| |

● |

the

impacts of the COVID-19 pandemic on our business and results of operations; |

| |

|

|

| |

● |

fluctuations

in product costs and availability; |

| |

|

|

| |

● |

international

risks and costs associated with our supply chain; |

| |

|

|

| |

● |

changes

in consumer demand; |

| |

|

|

| |

● |

risks

associated with operating our own online platform, including confidential consumer data; |

| |

|

|

| |

● |

reputational

harms which could adversely impact our ability to attract and retain customers; |

| |

|

|

| |

● |

the

potentially negative impact of our strategic plans and initiatives on our financial results; |

| |

|

|

| |

● |

unauthorized

disclosure of sensitive or confidential customer, vendor, or our information; |

| |

|

|

| |

● |

the

inability to attract, train, engage, and retain key personnel; |

| |

|

|

| |

● |

the

loss of one or more of our key executives; |

| |

|

|

| |

● |

the

effect of design and manufacturing defects on our products and services; |

| |

|

|

| |

● |

the

adverse effects from accidents, safety incidents, or workforce disruptions; |

| |

|

|

| |

● |

the

inability to sustain pricing levels for our products and services; |

| |

|

|

| |

● |

the

risk of warranty claims and product returns; |

| |

|

|

| |

● |

changes

in marketing of our products and services which could affect our marketing expenses and subscription levels; |

| |

|

|

| |

● |

the

need for additional capital to support business growth and objectives; |

| |

|

|

| |

● |

payment

processing risk; |

| |

● |

foreign

currency exchange rate fluctuations; |

| |

|

|

| |

● |

our

dependence on suppliers and manufactures to provide us with sufficient quantities of quality products in a timely fashion; |

| |

|

|

| |

● |

our

limited control over our suppliers, manufacturers, and logistics partners; |

| |

|

|

| |

● |

the

costs and risks associated with our complex regulatory, compliance, and legal environment; |

| |

|

|

| |

● |

our

inability or failure to protect our intellectual property rights; |

| |

|

|

| |

● |

changes

in tax laws and regulations; |

| |

|

|

| |

● |

failure

to comply with the U.S. Foreign Corrupt Practices Act of 1977 (the “FCPA”); |

| |

|

|

| |

● |

our

status as a “foreign private issuer” under U.S. securities laws and the disclosure obligations which are applicable to

us on the Nasdaq Capital Market; |

| |

|

|

| |

● |

our

use of home country corporate governance practices instead of otherwise applicable Nasdaq corporate governance requirements; |

| |

|

|

| |

● |

the

accuracy of our market growth forecasts; |

| |

|

|

| |

● |

our

management team’s limited experience managing a public company; |

| |

|

|

| |

● |

the

risk of earthquakes, fire, power outages, floods, public health crises, including the COVID-19 pandemic, and other catastrophic

events, and to interruption by man-made problems such as terrorism; |

| |

|

|

| |

● |

our

status as an “emerging growth company” and our election to comply with the reduced disclosure requirements as a public

company that may make our Ordinary Shares less attractive to investors; |

| |

|

|

| |

● |

the

risk that Ms. Jieting Zhao may have different interests than that of other shareholders; |

| |

|

|

| |

● |

the risk that Flying Height Consulting Services Limited may have different

interests than that of other shareholders; |

| |

|

|

| |

● |

the risk that if we fail to establish and maintain an effective system

of internal control over financial reporting, our ability to accurately and timely report our financial results or prevent fraud may be

adversely affected, and investor confidence and the market price of our Ordinary Shares may be adversely impacted; |

| |

|

|

| |

● |

our

intention to not pay dividends for the foreseeable future; |

| |

|

|

| |

● |

the

risk that an active, liquid trading market may not develop or be sustained for our Ordinary Shares; |

| |

|

|

| |

● |

the

risk that the laws of the Cayman Islands may not provide our shareholders with benefits comparable to those provided to shareholders

of corporations incorporated in the United States; and |

| |

|

|

| |

● |

the

risk that, because we are a Cayman Islands company and all of our business is conducted in Australia, you may be unable to bring

an action against us or our officers and directors or to enforce any judgment you may obtain, and the U.S. regulatory bodies may

be limited in their ability to conduct investigations or inspections of our operations in Australia; and |

While

we believe these expectations, and the estimates and projections on which they are based, are reasonable and were made in good faith,

the ultimate correctness of these forward-looking statements depends upon a number of known and unknown risks, uncertainties, events,

and other important factors, which include, but are not limited to, the risks disclosed in “Item 3. Key Information—3D. Risk

Factors” of this annual report. Any of these risk factors could cause our actual results, performance or achievements, or industry

results to differ materially from those expressed or implied in our forward-looking statements. Consequently, you should not rely on

any of these forward-looking statements.

The

forward-looking statements speak only as of the date on which they are made, and, except as required by law, we undertake no obligation

to correct, update, or revise any forward-looking statement to reflect new information, future events or circumstances, or otherwise,

except to the extent required under federal securities laws, after the date on which the statement is made or to reflect the occurrence

of unanticipated events. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or

combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. You are

advised to consult any additional disclosures we make in our other SEC filings. All subsequent written and oral forward-looking statements

attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained in

this annual report.

PART

I

Item 1. Identity of Directors, Senior Management and Advisers

Not

applicable.

Item 2. Offer Statistics and Expected Timetable

Not

applicable.

Item 3. Key Information

| B. |

Capitalization and indebtedness. |

Not

applicable.

| C. |

Reasons for the offer and use of proceeds. |

Not

applicable.

You

should carefully consider each of the following risks and all the other information contained in this annual report and in our other

filings with the SEC in evaluating us and our common stock. Although the risks are organized by headings, and each risk is discussed

separately, many are interrelated. Our business, financial condition, results of operations and cash flows could be materially and adversely

affected by these risks, and, as a result, the trading price of our common stock could decline. We have in the past been adversely affected

by certain of, and may in the future be affected by, these risks. You should not interpret the disclosure of any risk factor to imply

that the risk has not already materialized.

Risks

Related to Our Industry and Macroeconomic Conditions

Our

business is dependent on macroeconomic conditions and consumer discretionary spending, and reductions in such spending might adversely

affect the Company’s business, operations, liquidity, and financial results.

We

are an online retailer of gym and fitness equipment both under our proprietary brands and other brand names. Fitell’s mission is

to build an ecosystem with a whole fitness and wellness experience powered by technology to our customers. Our business depends on consumer

discretionary spending, and our results are highly dependent on Australian and Asian consumer confidence and the health of the Australian

and Asian economies. Consumer spending may be affected by many factors outside of the Company’s control, including general economic

conditions; consumer disposable income; consumer confidence and perception of economic conditions; the threat or outbreak of war, terrorism

or public unrest (including, without limitation, the conflict in Ukraine) which may cause supply chain disruptions, increased fuel costs

and the cost of materials, and create general economic instability; wage and unemployment levels; consumer debt and inflationary pressures;

the costs of basic necessities and other goods; effects of weather and natural disasters caused by climate change or otherwise; and epidemics,

contagious disease outbreaks, and other public health concerns including the ongoing COVID-19 pandemic. Decreases in consumer discretionary

spending may result in a decrease in comparable sales, and average value per transaction, which might cause us to increase promotional

activities, which will have a negative impact on our gross margins, all of which could negatively affect the Company’s business,

operations, liquidity, and financial results, particularly if consumer spending levels are depressed for a prolonged period of time.

Uncertain

global economic conditions could have a material adverse effect on our business, financial condition, results of operations or prospects.

Our

financial results are tied to global economic conditions and their impact on levels of consumer confidence and consumer spending. Global

consumer markets can be impacted by significant U.S. and international economic downturns, such as the current levels of inflation and

the global credit crunch experienced in 2008. Continued high levels of inflation or a return to a recession or a weak recovery, due to

factors that include, but are not limited to, disruptions in financial markets in the United States, or elsewhere, federal budget, tax

or trade policy issues in the United States, political upheavals, war or unrest economic sanctions against trading nations, and demonetization,

could cause us to experience revenue declines due to deteriorated consumer confidence and spending, and a decrease in the availability

of credit or on commercially acceptable terms, which could have a material adverse effect on our business prospects or financial condition.

Our

business is also dependent upon certain industries, such as the gym, fitness, and fitness equipment industries, and these are also cyclical

in nature. Therefore, these industries may experience their own significant fluctuations in demand for our products based on such things

as economic conditions and consumer demand. Many of these factors are beyond our control. As a result of the volatility in the industries

we plan to serve, we may ultimately have difficulty increasing or maintaining our level of sales or profitability. If the industries

we serve were to suffer a downturn, then our business may be further adversely affected.

Intense

competition in the gym and fitness equipment industry and in retail could limit our growth and reduce our profitability.

The

market for gym and fitness equipment retailers is highly fragmented, intensely competitive, and continually evolving. We compete with

retailers from multiple categories and in multiple channels, including large formats; traditional and specialty formats; mass merchants;

department stores; internet-based and direct-sell retailers; and increasingly from vendors that sell directly to customers. Our competitors

include companies that may have greater market presence (both brick and mortar and online), name recognition and financial, marketing

and other resources than we do. Further, the ability of consumers to compare prices in real-time puts additional pressure on us to maintain

competitive pricing. If we are unsuccessful in marketing and advertising strategies, especially for online and social media platforms,

or less successful than our competitors, we could lose customers and sales could decline, which could have an adverse impact on our revenues,

business, and results of operations. Furthermore, we cannot be sure that we will be able to continue to effectively compete in our markets

due to the disruptions caused by the COVID-19 pandemic or that any of our competitors are not in a better position to either respond

to the disruptions caused by the COVID-19 pandemic or capitalize on potential displaced market share, including vendors with whom we

compete accelerating their existing efforts to sell directly to consumers. An inability to successfully respond to competitive pressures

could have a material adverse effect on our results of operations or reputation. Our responses to competitive pressures could also have

a material effect on our results or reputation, including as it relates to pricing, quality, assortment, advertising, service, locations,

and online shopping experiences.

Industry

consolidation may result in increased competition, which could have a material adverse effect on our business.

Some

of our competitors have made, or may make acquisitions or enter into partnerships or other strategic relationships to achieve competitive

advantages. In addition, new entrants not currently considered competitors may enter our market through acquisitions, partnerships or

strategic relationships. We expect industry consolidation to continue and/or increase. Industry consolidation may result in competitors

with more compelling product offerings or greater pricing flexibility than we may have, or business practices that make it more difficult

for us to compete effectively, including on the basis of price, sales, technology or supply. These competitive pressures could have a

material adverse effect on our business.

Fluctuations

in product costs and availability due to inflationary pressures, fuel price uncertainty, supply chain constraints, increases in commodity

prices, labor shortages and other factors could negatively impact our business and results of operations.

Our

product costs are affected, in part, by the costs of component materials. A substantial increase in the prices of raw materials or decrease

in the availability of raw materials could dramatically increase the costs associated with manufacturing the equipment that we purchase

from our vendors, which could cause the price of our merchandise to increase and could have a negative impact on our sales and profitability.

In addition, increases in commodity prices could also adversely affect our results of operations. If we increase the price of our products

in order to maintain gross margins for our products, such increase may adversely affect demand for, and sales of, our products, which

could have a material adverse effect on our financial condition and results of operations.

We

rely upon various means of third-party transportation to deliver products from vendors and our manufacturing facilities to our customers.

Consequently, our results may be affected by those factors affecting transportation, including the price of fuel and the availability

of aircraft, ships, trucks, and drivers. The price of fuel and demand for transportation services has fluctuated significantly in recent

years, and has resulted in increased costs for us and our vendors. In addition, changes in regulations may result in higher fuel costs

through taxation, transportation restrictions or other means. Fluctuations in transportation costs and availability could adversely affect

our results of operations.

Labor

shortages in the transportation industry could negatively affect transportation costs and our ability to transport products to our customers

in a timely manner. Our results of operations may be adversely affected if we, or our vendors, are unable to secure adequate transportation

resources at competitive prices to fulfill our delivery schedules. Further, difficulties in moving products manufactured overseas and

through the ports of other jurisdictions, whether due to port congestion, government shutdowns, labor disputes, product regulations and/or

inspections or other factors, including natural disasters or health pandemics, could negatively affect our business.

Approximately

85% of the products that the Company purchased in the fiscal year ended June 30, 2024, were manufactured abroad, which subjects us to

various international risks and costs, including foreign trade issues, currency exchange rate fluctuations, shipment delays and supply

chain disruption and political instability, which could cause our sales and profitability to suffer.

Approximately

85% of the products that the Company purchased in the fiscal year ended June 30, 2024, were manufactured abroad in China. Foreign imports

subject us to risk relating to changes in import duties quotas, the introduction of taxes on imported goods or the extension of income

taxes on our foreign suppliers’ sales of imported goods through the adoption of destination-based income tax jurisdiction, freight

cost increases and economic and political uncertainties. We may also experience shipment delays caused by shipping port constraints,

labor strikes, work stoppages, acts of war, including the current conflict in Ukraine, and terrorism, or other supply chain disruptions,

including those caused by extreme weather, natural disasters, and pandemics and other public health concerns.

If

any of these or other factors, including trade tensions between foreign nations, including China and Russia, were to cause a disruption

of trade from the countries in which our vendors’ supplies are located, our inventory levels may be reduced and/or the cost of

our products may increase. We may need to seek alternative suppliers or vendors, raise prices, or make changes to our operations, any

of which could have a material adverse effect on our sales and profitability, results of operations and financial condition. Additionally,

we could be impacted by negative publicity or, in some cases, face potential liability to the extent that any foreign manufacturers from

whom we directly or indirectly purchase products utilize labor, environmental, workplace safety and other practices that vary from those

commonly accepted in Australia. Also, the prices charged by foreign manufacturers may be affected by the fluctuation of their local currency

against the Australian dollar and the price of raw materials, which could cause the cost of our products to increase and negatively impact

our sales or profitability.

Failure

to manage inventory at optimal levels could adversely affect our business, financial condition and results of operations.

We

are required to manage a large volume of inventory effectively for our business. We depend on our forecasts for the anticipated demand

for our products to make procurement plans and manage our inventory. Our forecast for demands, however, may not accurately reflect the

actual market demands, which depends on a number of factors including, without limitation, launches of new products, changes in product

life cycles and pricing, product defects, changes in user spending patterns, supplier back orders and other supplier-related issues,

as well as the volatile economic environment in the markets where we sell our products. We cannot assure you that we will be able to

maintain proper inventory levels for our business at all times, and any such failure may have a material and adverse effect on our business,

financial condition and results of operations.

Inventory

levels in excess of demand may result in inventory write-downs or an increase in inventory holding costs and a potential negative effect

on our liquidity. As we plan to continue expanding our product offerings, we expect to include more products in our inventory, which

will make it more challenging for us to manage our inventory effectively and will put more pressure on our warehousing system. If we

fail to manage our inventory effectively, we may be subject to a heightened risk of inventory obsolescence, a decline in inventory values,

and significant inventory write-downs or write-offs. In addition, we may be required to lower sale prices in order to reduce inventory

level, which may lead to lower gross margins. High inventory levels may also require us to commit substantial capital resources, preventing

us from using that capital for other important purposes. Any of the above may materially and adversely affect our results of operations

and financial condition.

The

Company’s intangible assets consist of brand names and goodwill. At June 30, 2024 and 2023, the Company had brand names and goodwill

with costs of approximately $337,504 and $1,161,052, respectively, which all have indefinite lives. The Company evaluates intangible

assets with indefinite lives for impairment at least annually or when events or changes in circumstances indicate that an impairment

may exist. The Company determined that none of its intangible assets were impaired in the fiscal year ended June 30, 2024, and 2023.

Conversely,

if we underestimate customer demand, or if our suppliers fail to provide products to us in a timely manner, we may experience inventory

shortages, which may, in turn, require us to purchase our products at higher costs, leading to a negative impact on our financial condition

and our relationships with distributors. Under-stocking can lead to missed sales opportunities, while over-stocking could result in inventory

depreciation and decreased shelf space for stocks that are in higher demands. These results could adversely affect our business, financial

condition and results of operations.

Russia’s

invasion of Ukraine may present risks to our operations and investments.

Russia’s

recent military interventions in Ukraine have led to, and may lead to, additional sanctions being levied by the United States, European

Union and other countries against Russia. Russia’s military incursion and the resulting sanctions could adversely affect global

financial markets and thus could affect the value of our operations and investments, even though we do not have any direct exposure to

Russia or the adjoining geographic regions. Currently, we do not do any business with parties in Russia, Ukraine or Belarus, nor are

any of the products that we sell or the parts for such products manufactured in Russia, Ukraine or Belarus. In addition, Russia’s

invasion of Ukraine and the international sanctions against Russia that followed the invasion have not had a direct effect on our business.

The extent and duration of the military action, sanctions, and resulting market disruptions are impossible to predict, but could be substantial.

Any such disruptions caused by Russian military action or resulting sanctions may magnify the impact of other risks described in this

section. We cannot predict the progress or outcome of the situation in Ukraine, as the conflict and governmental reactions are rapidly

developing and beyond their control. Prolonged unrest, intensified military activities, or more extensive sanctions impacting the region

could have a material adverse effect on the global economy, and such effect could in turn have a material adverse effect on our operations,

results of operations, financial condition, liquidity and business outlook.

Risks

Related to Our Business

If

we are unable to predict or effectively react to changes in consumer demand, we may lose customers and our sales may decline.

Our

success depends in part on our ability to anticipate and respond in a timely manner to changing consumer demand, preferences, and shopping

patterns, which cannot be predicted with certainty and are subject to continual change and evolution. We strive to deliver a seamless

shopping experience to our customers through online shopping experiences. For example, we must meet athletes’ expectations with

respect to, among other things, creating appealing and consistent online experiences; delivering elevated customer service; and providing

fast and reliable delivery, and convenient return options. Our customers have expectations about how they shop through eCommerce or more

generally engage with businesses across different channels or media (through online and other digital or mobile channels or particular

forms of social media), which may vary across demographics and may evolve rapidly. If we are unable to provide an online retail experience

across all channels that aligns with our customers’ expectations and preferences, it could have an adverse impact on our revenues,

business and results of operations.

We

often make advance commitments to purchase products, which may make it more difficult for us to adapt to rapidly-evolving changes in

consumer preferences. Furthermore, supply chain challenges due to the COVID-19 pandemic and other factors have made it more difficult

to obtain certain in-demand products. Our sales could decline significantly if we misjudge the market for our new merchandise, which

may result in significant merchandise markdowns and lower margins, missed opportunities for other products, or inventory write-downs,

and could have a negative impact on our reputation, profitability and demand.

We

may be unable to attract and retain subscribers, which could have an adverse effect on our strategy to develop new interactive fitness

equipment and platforms/mobile application with subscription service.

In

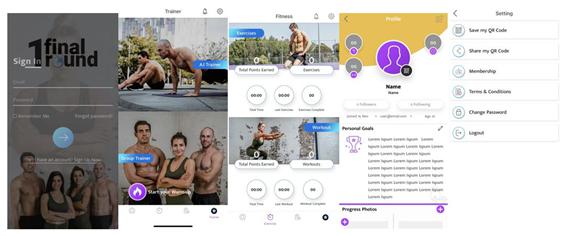

2021, we began development of new interactive fitness equipment and platforms/mobile application with subscription service, which include

smart cardio exercise equipment such as interactive exercise bikes, treadmills, and workout mirrors with built-in touchscreens and training

content platforms and 1FinalRound, our AI-powered interactive platform with our proprietary online training content and capability to

be interactive with personal trainers, follow members, and track workout progress.

The

success of these new products is dependent on our ability to attract and retain subscribers, and we cannot be sure that we will be successful

in these efforts, or that subscriber retention levels will not materially decline in the future. There are a number of factors that could

lead to a decline in subscriber levels or that could prevent us from increasing our subscriber levels, including:

| |

● |

our

failure to introduce new features, products, or services that our potential subscribers find engaging or our introduction of new

products or services, or changes to existing products and services that are not favorably received; |

| |

● |

harm

to our brand and reputation; |

| |

● |

pricing

and perceived value of our offerings; |

| |

● |

our

inability to deliver quality products, content, and services; |

| |

● |

unsatisfactory

experiences with the delivery, installation, or servicing of our products, including due to prolonged delivery timelines and limitations

on or the suspension of the in-home installation, return, and warranty servicing process; |

| |

● |

our

potential subscribers engaging with competitive products and services; |

| |

● |

technical

or other problems preventing subscribers from accessing our content and services in a rapid and reliable manner or otherwise affecting

the subscribers’ experience; |

| |

● |

a

decline in the public’s interest in interactive fitness equipment and platforms; |

| |

● |

deteriorating

general economic conditions or a change in consumer spending preferences or buying trends, whether as a result of the COVID-19 pandemic

or otherwise; and |

| |

● |

interruptions

in our ability to sell or deliver our products or to create content and services for our potential subscribers as a result of the

COVID-19 pandemic. |

Additionally,

further expansion into international markets such as Southeast Asia will create new challenges in attracting and retaining subscribers

that we may not successfully address. As a result of these factors, we cannot be sure that our potential subscriber levels will be adequate

to maintain or permit the expansion of our operations. A decline in future subscriber levels could have an adverse effect on our business,

financial condition, and/or operating results.

Online

growth in our business is complex and there are risks associated with operating our own online platform, including those relating to

confidential consumer data.

Maintaining

and continuing to improve our online retail platform involves substantial investment of capital and resources, integrating multiple information

and management systems, increasing supply chain and distribution capabilities, attracting, developing and retaining qualified personnel

with relevant subject matter expertise, and effectively managing and improving the customer experience. This involves substantial risk,

including risk of cost overruns, website downtime and other technology disruptions, supply and distribution delays, and other issues

that can affect the successful operation of our online platform. Technological disruptions can result from delays, or downtime caused

by high volumes of users or transactions, deficiencies in design or implementation, platform enhancements, power outages, computer and

telecommunications failures, computer viruses, worms, ransomware or other malicious computer programs, denial-of-service attacks, security

breaches through cyber-attacks from cyber-attackers or sophisticated organizations, catastrophic events such as fires, tornadoes, earthquakes

and hurricanes, and usage errors. If we are not able to successfully operate and continually improve our online platform to provide a

user-friendly, secure online experience offering merchandise and delivery options expected by our customers, we could be placed at a

competitive disadvantage and our reputation, operations, financial results, and future growth could be materially adversely affected.

Harm

to our reputation could adversely impact our ability to attract and retain customers.

Negative

publicity or perceptions involving us or our brands, products, vendors, or marketing and other partners, or failure to detect, prevent,

mitigate or address issues giving rise to reputational risk could adversely impact our reputation, business, results of operations, and

financial condition, and may adversely impact our ability to attract and retain customers. Issues that might pose a reputational risk

include: an inability to provide an online experience that meets the expectations of consumers; failure of our cyber-security measures

to protect against data breaches; product liability, product recalls, and product boycotts; our handling of issues relating to environmental,

social, and governance (“ESG”) matters, including inclusion and diversity; our response to the COVID-19 pandemic; our social

media activity; failure to comply with applicable laws and regulations; public stances on controversial social or political issues; product

sponsorship relationships, including those with celebrity spokespersons, influencers or group affiliations; and any of the other risks

enumerated in this section, “Item 3 – 3D. Risk Factors”. Furthermore, the prevalence of social media and a constant,

on-demand news cycle may accelerate and in the short-term increase the potential scope of any negative publicity we or others might receive

and could increase the negative impact of these issues on our reputation, business, results of operations, and financial condition.

Our

strategic plans and initiatives may initially result in a negative impact on our financial results and such plans and initiatives may

not achieve the desired results within the anticipated time frame or at all.

Our

ability to successfully implement and execute our strategic plans and initiatives depends on many factors, some of which are out of our

control. For example, a strategic determination to increase promotional activities in response to challenging conditions in the retail

market may not achieve the desired results and could negatively impact our gross profit margin. Our focus on long-term strategic investments,

including investments in our digital capabilities, our online platform, improvements to the consumer experience online, our supply chain,

the continued development of our smart cardio exercise equipment and 1FinalRound training platform and other specialty concepts may require

significant capital investment and management attention at the expense of other business initiatives and may take longer than anticipated

to achieve the desired return. Additionally, any new initiative is subject to certain risks, including consumer acceptance, competition,

product differentiation, and the ability to attract and retain qualified personnel to support the initiative.

We

could be subject to information technology system failures, network disruptions, and breaches in data security which could negatively

affect our business, financial position, results of operations and cash flows.

As

dependence on digital technologies is expanding, cyber incidents, including deliberate attacks or unintentional events have been increasing

worldwide. Computers and telecommunication systems are used to conduct our operations and have become an integral part of our business.

We use these systems to analyze and store financial and operating data, as well as to support our internal communications and interactions

with business partners. Cyber-attacks could compromise our computer and telecommunications systems and result in additional costs as

well as disruptions to our business operations or the loss of our data. A cyber-attack involving our information systems and related

infrastructure, or those of our business partners, could disrupt our business and negatively impact our operations in a variety of ways,

such as, among others:

| |

● |

an

attack on the computers which control our operations could cause a temporary interruption of our business; |

| |

● |

a

cyber-attack on our accounting or accounts payable systems could expose us to liability to employees and third parties if their sensitive

personal information is obtained; |

| |

● |

a

possible loss of material information, which in turn could delay our operations and selling efforts, causing economic losses; or |

| |

● |

a

cyber-attack on a service provider could result in supply chain disruptions, which could delay or halt our operations. |

| |

Unauthorized

disclosure of sensitive or confidential customer, vendor or Company information could result in substantial costs and reputational damage,

harm our business and standing with our athletes and could subject us to litigation and enforcement actions.

The

protection of our data as well as customer data is critical. As with most online retailers, we collect, receive, store, manage, transmit

and delete confidential data, including payment card and personally identifiable information, in the normal course of customer transactions,

as well as other confidential and sensitive information, such as personal information about our customers and our vendors, and confidential

Company information. We also work with third-party vendors and service providers that provide technology, systems and services that we

use in connection with the collection, storage and transmission of this information. While we have taken significant steps to protect

confidential information, the intentional or negligent actions of third parties may undermine our existing security measures and allow

unauthorized parties to obtain access to our data systems and misappropriate confidential data. Our information systems, and those of

our third-party service providers, are vulnerable to an increasing threat of continually evolving data protection and cyber-security

risks. There can be no assurance that advances in computer capabilities, new discoveries in the field of cryptography or other developments

will prevent a future compromise of our customer transaction processing capabilities and other personal data. Because the techniques

used to obtain unauthorized access to, disable, degrade, or sabotage systems change frequently and often are not recognized until they

are launched against a target, we may be unable to anticipate these techniques or to implement adequate preventative measures.

While

we have no knowledge of any material data security breaches to date, any compromise of our data security could result in a violation

of applicable privacy and other laws or standards, significant legal and financial exposure beyond the scope or limits of our insurance

coverage, interruption of our operations, increased operating costs associated with remediation, equipment acquisitions or disposal,

added personnel, and a loss of confidence in our security measures, which could harm our business, reputation or investor confidence.

In

addition, data governance failures can adversely affect our reputation and business. Our business depends on our customers’ willingness

to entrust us with their personal information. Events that adversely affect that trust, including inadequate disclosure to our customers

of our uses of their information or any security breach involving the misappropriation, loss or other unauthorized disclosure of sensitive

or confidential information could attract a substantial amount of media attention, damage our reputation, expose us to risk of litigation

and material liability, disrupt our operations and harm our business. Further, the data privacy and cyber-security regulatory environment

is constantly changing, with new and increasingly rigorous and complex requirements. Maintaining our compliance with those requirements,

including recently enacted state consumer privacy laws, may require significant effort and cost, require changes to our business practices,

and limit our ability to obtain data used to provide a personalized customer experience. In addition, failure to comply with applicable

requirements could subject us to fines, sanctions, governmental investigations, lawsuits or reputational damage.

Problems

with the third-party e-commerce platform for online stores and retail point-of-sale system that we utilize and our information systems

could disrupt our operations and negatively impact our financial results and materially adversely affect our business operations.

We

utilize a third-party e-commerce platform for online stores and retail point-of-sale system for the needs of our business, including

as a provider for electronic payment processing. If any of these systems fail to function properly, it could disrupt our operations,

including our ability to track, record and analyze the merchandise that we sell, process shipments of goods, process financial information

or credit card or electronic payment transactions, deliver products or engage in similar normal business activities. If our independent

service provider becomes unwilling or unable to provide these services to us or if the cost of using our provider increases, our business

could be harmed.

Our

information systems, including our back-up systems, are subject to damage or interruption from power outages; computer and telecommunications

failures; computer viruses, worms, ransomware, and other malicious computer programs; denial-of-service attacks; security breaches (through

cyber-attacks from cyber-attackers or sophisticated organizations); catastrophic events such as fires, tornadoes, earthquakes and hurricanes;

and usage errors. If our information systems and our back-up systems are damaged, breached or cease to function properly, we may have

to make a significant investment to repair or replace them, and we may suffer loss of critical data and interruptions or delays in our

business operations. Any material disruption, malfunction or other similar problems in or with our core information systems could negatively

impact our financial results and materially adversely affect our business operations.

We

may be unable to attract, train, engage and retain key personnel.

Our

long-term success and ability to implement our strategic and business planning processes depends in large part on our ability to continue

to attract, retain, train and develop key personnel and qualified employees in all areas of the Company. Our ability to meet our labor

needs while controlling labor costs is subject to numerous external factors, including market pressures with respect to prevailing wage

rates, unemployment levels, and health and other insurance costs; the impact of legislation or regulations governing labor relations,

immigration, minimum wage, and healthcare benefits; changing demographics; and our reputation within the labor market. Should we fail

to increase our wages competitively in response to any increasing wage rates, the quality of our workforce could decline, causing our

customer service to suffer. Any increase in the cost of our labor could have an adverse effect on our operating costs, financial condition

and results of operations.

In

addition, in order to continue to build and enhance our online platforms, we must attract and retain a large number of skilled professionals,

including technology professionals to implement our ongoing technology and other strategic offerings. The market for these professionals

is increasingly competitive. An inability to provide wages and/or benefits that are competitive within the markets in which we operate

could adversely affect our ability to retain and attract these employees. Further, changes in market compensation rates may adversely

affect our labor costs.

The

loss of one or more of our key executives or the inability to successfully attract and retain executive officers or implement effective

succession planning strategies could have a material adverse effect on our business.

Our

long-term success and ability to implement our strategic and business planning processes depends in large part on our ability to continue

to attract and retain executive management. All employees, including members of our executive management and key personnel, are at-will

employees. The loss of any one or more of our executive management, including our chief executive officer and director, Yinying Lu, or

other key personnel could seriously harm our business. Additionally, effective succession planning for executive management and key personnel

is vital to our long-term continued success. Failure to ensure effective transfer of knowledge, setting of strategic direction, and smooth

transitions involving executive management and key personnel could hinder our long-term strategies and success.

We

are dependent upon key management employees and third parties.

The

responsibility of overseeing the day-to-day operations and the strategic management of our business depends substantially on our senior

officers and our key personnel. Loss of such personnel may have an adverse effect on our performance. The success of our operations will

depend upon numerous factors, many of which are beyond our control, including our ability to attract and retain additional key personnel

in sales, marketing, technical support and finance. We currently depend upon a relatively small number of key persons to seek out and

form strategic alliances and find and retain additional employees. Certain areas in which we operate are highly competitive regions and

competition for qualified personnel is intense. We may be unable to hire suitable personnel or there may be periods of time where a particular

position remains vacant while a suitable replacement is identified and appointed.

Our

inability to hire and maintain suitable personnel could have a material adverse effect on us and could prevent us from effectively pursuing

our business plan, including developing, growing, and operating our business profitably.

We

also depend upon third parties, including consultants, suppliers and others, for their expertise and expect to continue to do so for

the foreseeable future. Our ability to continue conducting our activities is in large part dependent upon the efforts of third parties.

We may need to engage additional third parties for new business operations. If such parties’ work is deficient or negligent or

is not completed in a timely manner, it could have a material adverse effect on the Company. As a result, our use of the services of

consultants could have a material adverse effect on us and could prevent us from effectively pursuing our business plan

Our

independent directors do not devote their full-time attention to the affairs of the Company and could allocate their time and attention

to other business ventures which may not benefit the Company.

Our

independent directors do not devote their time exclusively to the Company and engage in other business activities. Although there are

none known to us, the potential for conflicts of interest exists among us and affiliated persons for future business opportunities that

may not be presented to us. Our directors may have conflicts of interests in allocating time, services, and functions between the other

business ventures in which those persons may be or become involved.

Our

directors and officers may in the future be in a position of conflict of interest.

Some

of our directors and officers currently also serve as directors and officers of other companies involved in the fitness industry, and

any of our directors may in the future serve in such positions. As at the date of this annual report, none of our directors or officers

serves as an officer or director of a gym and fitness equipment company nor possesses a conflict of interests with our business. However,

there exists the possibility that they may in the future be in a position of conflict of interest.

We

may acquire additional businesses or assets, form joint ventures or make investments in other companies in the future that may be unsuccessful

and may harm our operating results and prospects.

As

part of our business strategy, we may pursue additional acquisitions of complementary businesses or assets. The type of financing for

any such acquisition will depend on circumstances existing at that time, including market conditions and our share price. If we are successful

at identifying and making such acquisitions, integration of any acquired businesses or assets nevertheless involves many challenges,

including a potential strain on our administrative and operational resources, unanticipated issues, expenses or liabilities, and difficulties

in the assimilation of different corporate cultures and business practices. We may also seek to enter into joint ventures, pursue strategic

alliances in an effort to leverage our existing operations and industry experience, increase our product offerings, expand our distribution

and make investments in other companies. We do not have specific timetables for these potential activities and we cannot guarantee that

we will be able to identify and complete suitable acquisitions or investments at reasonable prices, or that we will be successful in

realizing any anticipated benefits from any future acquisitions or investments.

The

success of any acquisitions, joint ventures, strategic alliances or investments will depend on our ability to identify, negotiate, complete

and, in the case of acquisitions, integrate those transactions and, if necessary, obtain satisfactory debt or equity financing to fund

those transactions. We may not realize the anticipated benefits of any acquisition, joint venture, strategic alliance or investment.

We may not be able to integrate acquisitions successfully into our existing business, maintain the key business relationships of businesses

we acquire, or retain key personnel of an acquired business, and we could assume unknown or contingent liabilities or incur unanticipated

expenses.

Integration

of acquired companies or businesses also may require management resources that otherwise would be available for ongoing development of

our existing business. Any acquisitions or investments made by us also could result in significant write-offs or the incurrence of debt

and contingent liabilities, any of which could harm our operating results. In addition, if we choose to issue equity as consideration

for any acquisition, our shareholders may experience dilution.

Our

products and services may be affected from time to time by design and manufacturing defects that could adversely affect our business

and result in harm to our reputation.

We

offer products and services that can be affected by design and manufacturing defects. Defects may also exist in components and products

that we source from third parties. Any such defects could make our products and services unsafe, create a risk of environmental or property

damage and personal injury, and subject us to the hazards and uncertainties of product liability claims and related litigation. There

can be no assurance that we will be able to detect and fix all issues and defects in the products and services we offer. Failure to do

so could result in widespread technical and performance issues affecting our products and services and could lead to claims against us.

We maintain general liability insurance; however, design and manufacturing defects, and claims related thereto, may subject us to judgments

or settlements that result in damages materially in excess of the limits of our insurance coverage. In addition, we may be exposed to

recalls, product replacements or modifications, write-offs of inventory, property and equipment, or intangible assets, and significant

warranty and other expenses such as litigation costs and regulatory fines. If we cannot successfully defend any large claim, maintain

our general liability insurance on acceptable terms, or maintain adequate coverage against potential claims, our financial results could

be adversely impacted. Further, quality problems could adversely affect the experience for users of our products and services, and result

in harm to our reputation, loss of competitive advantage, poor market acceptance, reduced demand for our products and services, delays

in new product and service introductions, and lost revenue.

Our

business could be adversely affected by an accident, safety incident, or workforce disruption.

Our

manufacturing processes and related activities, as well as our warehousing and logistics activities, could expose us to significant personal

injury claims that could subject us to substantial liability. While we maintain liability insurance in amounts and of the type generally

consistent with industry practice, the amount of such coverage may not be adequate to cover fully all claims, and we may be forced to

bear substantial losses from an accident or safety incident resulting from our manufacturing, warehousing, or delivery activities. Additionally,

if our employees decide to join or form a labor union, we may become party to a collective bargaining agreement, which could result in

higher employee costs and increased risk of work stoppages. It is also possible that a union seeking to organize one subset of our employee

population, such as the employees in our manufacturing facility, could also mount a corporate campaign, resulting in negative publicity

or other actions that require attention by our management team and our employees. Negative publicity, work stoppages, or strikes by unions

could have an adverse effect on our business, prospects, financial condition, and operating results.

Our

quarterly operating results and other operating metrics may fluctuate from quarter to quarter, which makes these metrics difficult to

predict.

Our

quarterly operating results and other operating metrics have fluctuated in the past and may continue to fluctuate from quarter to quarter

and make it difficult to forecast our future results. Consequently, you should not rely on our past quarterly operating results as indicators

of future performance. Our financial condition and operating results in any given quarter can be influenced by numerous factors, many

of which we are unable to predict or are outside of our control, including:

| |

● |

the

continued market acceptance of, and the growth of the fitness and wellness market; |

| |

● |

our

ability to maintain and attract new customers; |

| |

● |

the

timing and success of new product, service, feature, and content introductions by us or our competitors or any other change in the

competitive landscape of our market; |

| |

● |

pricing

pressure as a result of competition or otherwise; |

| |

● |

delays

or disruptions in our supply chain; |

| |

● |

errors

in our forecasting of the demand for our products and services, which could lead to lower revenue or increased costs, or both; |

| |

● |

increases

in marketing, sales, and other operating expenses that we may incur to grow and expand our operations and to remain competitive; |

| |

● |

the

ability to maintain our showroom; |

| |

● |

successful

expansion into international markets, including Asia; |

| |

● |

our

ability to maintain gross margins and operating margins; |

| |

● |

system

failures or breaches of security or privacy; |

| |

● |

adverse

litigation judgments, settlements, or other litigation-related costs, including content costs for past use; |

| |

● |

changes

in the legislative or regulatory environment, including with respect to privacy, consumer product safety, and advertising, or enforcement

by government regulators, including fines, orders, or consent decrees; |

| |

● |

fluctuations

in currency exchange rates and changes in the proportion of our revenue and expenses denominated in foreign currencies; |

| |

● |

changes

in our effective tax rate; |

| |

● |

changes

in accounting standards, policies, guidance, interpretations, or principles; and |

| |

● |

changes

in business or macroeconomic conditions, including the impact of the current COVID-19 outbreak, lower consumer confidence, recessionary