As filed with the Securities and Exchange Commission on September 22, 2023

Securities Act File No. 333-

Investment Company Act File No. 811-06540

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

☐ Pre-Effective Amendment No. ___

☐ Post-Effective Amendment No. ___

(Check appropriate box or boxes)

BLACKROCK

MUNIYIELD QUALITY FUND III, INC.

(Exact Name of Registrant as Specified in Charter)

100 Bellevue Parkway

Wilmington, Delaware 19809

(Address of Principal Executive Offices: Number, Street, City, State, Zip Code)

(800) 882-0052

(Area Code and Telephone Number)

John M. Perlowski

President and Chief Executive Officer

BlackRock MuniYield Quality Fund III, Inc.

50 Hudson Yards

New

York, New York 10001

(Name and Address of Agent for Service)

With copies to:

|

|

|

| Margery K. Neale, Esq.

Elliot J. Gluck, Esq.

Willkie Farr & Gallagher LLP

787 Seventh Avenue New

York, New York 10019-6099 |

|

Janey Ahn, Esq.

BlackRock Advisors, LLC

50 Hudson Yards New York,

New York 10001 |

AS SOON AS PRACTICABLE AFTER THE EFFECTIVE DATE OF THIS REGISTRATION STATEMENT

(Approximate Date of Proposed Public Offering)

The Registrant hereby amends

this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in

accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

This Registration Statement is organized as follows:

| a. |

Letter to Common Shareholders of BlackRock Virginia Municipal Bond Trust (“BHV”), BlackRock

Investment Quality Municipal Trust, Inc. (“BKN”), BlackRock MuniYield Michigan Quality Fund, Inc. (“MIY”), BlackRock MuniYield Pennsylvania Quality Fund (“MPA”) and BlackRock MuniYield Quality Fund III, Inc.

(“MYI”) |

| b. |

Questions & Answers for Common Shareholders of BHV, BKN, MIY, MPA and MYI. |

| c. |

Notice of Joint Special Meeting of Shareholders of BHV, BKN, MIY, MPA and MYI. |

| d. |

Joint Proxy Statement/Prospectus regarding the proposed mergers of BHV, BKN, MIY and MPA into MYI.

|

| e. |

Statement of Additional Information regarding the proposed mergers of BHV, BKN, MIY and MPA into MYI.

|

| f. |

Part C: Other Information. |

BLACKROCK VIRGINIA MUNICIPAL BOND TRUST

BLACKROCK INVESTMENT QUALITY MUNICIPAL TRUST, INC.

BLACKROCK MUNIYIELD MICHIGAN QUALITY FUND, INC.

BLACKROCK MUNIYIELD PENNSYLVANIA QUALITY FUND

BLACKROCK MUNIYIELD QUALITY FUND III, INC.

100 Bellevue Parkway

Wilmington, Delaware 19809

(800) 882-0052

[●], 2023

Dear Common Shareholder:

You are cordially invited to attend a joint special shareholder meeting (the “Special Meeting”) of BlackRock Virginia Municipal Bond Trust

(“BHV”), BlackRock Investment Quality Municipal Trust, Inc. (“BKN”), BlackRock MuniYield Michigan Quality Fund, Inc. (“MIY”), BlackRock MuniYield Pennsylvania Quality Fund (“MPA”) and BlackRock MuniYield

Quality Fund III, Inc. (“MYI” or the “Acquiring Fund” and collectively with BHV, BKN, MIY and MPA, the “Funds,” and each, a “Fund”), to be held on [●], 2023 at [●] a.m. (Eastern time). The Special

Meeting will be held in a virtual meeting format only. Shareholders will not have to travel to attend the Special Meeting, but will be able to view the Special Meeting live, have a meaningful opportunity to participate, including the ability to ask

questions of management, and cast their votes by accessing a web link. Before the Special Meeting, I would like to provide you with additional background information and ask for your vote on important proposals affecting the Funds.

Common Shareholders of BHV: You and the preferred shareholders of BHV are being asked to vote as a single class on a proposal to approve an Agreement

and Plan of Merger between BHV and the Acquiring Fund (the “BHV Merger Agreement”) providing for the merger of BHV, a Delaware statutory trust and a closed-end management investment

company, with the Acquiring Fund, a Maryland corporation and a closed-end management investment company (the “BHV Merger”). The BHV Merger would be effected by merging BHV with and into a

wholly-owned subsidiary of the Acquiring Fund, which has been formed for the sole purpose of consummating the BHV Merger and will transfer its assets and liabilities to the Acquiring Fund and dissolve as soon as practicable following the completion

of the BHV Merger. The Acquiring Fund has a similar investment objective and similar investment strategies, policies and restrictions as BHV, although there are some differences. Preferred shareholders of BHV are also being asked to vote as a

separate class on a proposal to approve the BHV Merger Agreement and the BHV Merger.

Common Shareholders of BKN: You and the preferred

shareholders of BKN are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Merger between BKN and the Acquiring Fund (the “BKN Merger Agreement”) providing for the merger of BKN, a Maryland corporation

and a closed-end management investment company, with the Acquiring Fund, a Maryland corporation and a closed-end management investment company (the

“BKN Merger”). The BKN Merger would be effected by merging BKN with and into a wholly-owned subsidiary of the Acquiring Fund, which has been formed for the sole purpose of consummating the BKN Merger and will transfer its assets and

liabilities to the Acquiring Fund and dissolve as soon as practicable following the completion of the BKN Merger. The Acquiring Fund has a similar investment objective and similar investment strategies, policies and restrictions as BKN, although

there are some differences. Preferred shareholders of BKN are also being asked to vote as a separate class on a proposal to approve the BKN Merger Agreement and the BKN Merger.

Common Shareholders of MIY: You and the preferred shareholders of MIY are being asked to vote as a single class on a proposal to approve an Agreement

and Plan of Merger between MIY and the Acquiring Fund (the “MIY Merger Agreement”) providing for the merger of MIY, a Maryland corporation and a closed-end management investment company,

with the Acquiring Fund, a Maryland corporation and a closed-end management investment company (the “MIY Merger”). The MIY Merger would be effected by merging MIY with and into a wholly-owned

subsidiary of the Acquiring Fund, which has been formed for the sole purpose of consummating the MIY Merger and will transfer its assets and liabilities to the Acquiring Fund and dissolve as soon as practicable following the completion of the MIY

Merger. The Acquiring Fund has a similar investment objective and similar investment strategies, policies and

restrictions as MIY, although there are some differences. Preferred shareholders of MIY are also being asked to vote as a separate class on a proposal to approve the MIY Merger Agreement and the

MIY Merger.

Common Shareholders of MPA: You and the preferred shareholders of MPA are being asked to vote as a single class on a proposal to

approve an Agreement and Plan of Merger between MPA and the Acquiring Fund (the “MPA Merger Agreement” and collectively with the BHV Merger Agreement, the BKN Merger Agreement and the MIY Merger Agreement, the “Merger

Agreements”) providing for the merger of MPA, a Massachusetts business trust and a closed-end management investment company, with the Acquiring Fund, a Maryland corporation and a closed-end management investment company (the “MPA Merger” and collectively with the BHV Merger, BKN Merger, MIY Merger, the “Mergers”). The MPA Merger would be effected by merging MPA with

and into a wholly-owned subsidiary of the Acquiring Fund, which has been formed for the sole purpose of consummating the MPA Merger and will transfer its assets and liabilities to the Acquiring Fund and dissolve as soon as practicable following the

completion of the MPA Merger. The Acquiring Fund has a similar investment objective and similar investment strategies, policies and restrictions as MPA, although there are some differences. Preferred shareholders of MPA are also being asked to vote

as a separate class on a proposal to approve the MPA Merger Agreement and the MPA Merger.

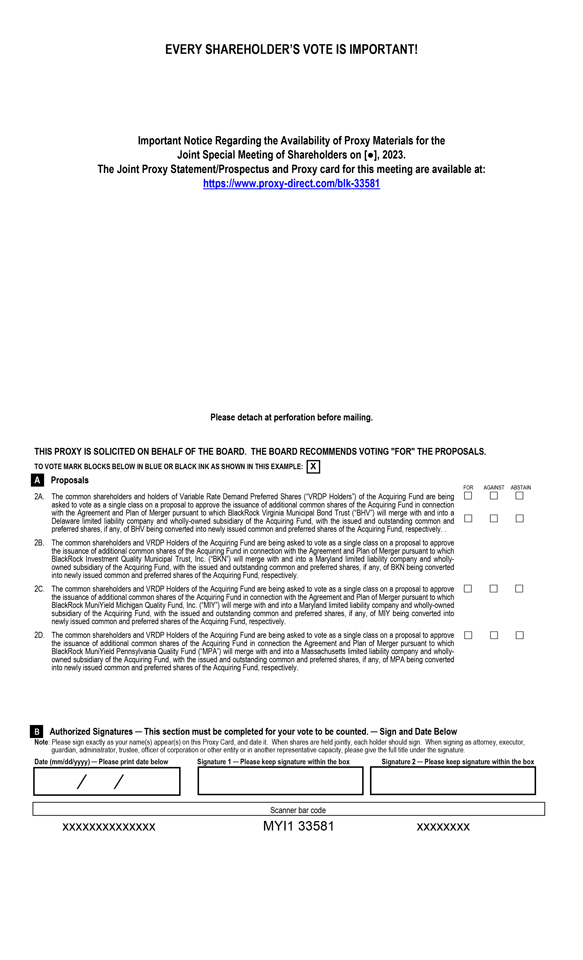

Common Shareholders of the Acquiring Fund: You and the

preferred shareholders of the Acquiring Fund are being asked to vote as a single class on a proposal to approve the issuance of additional common shares of the Acquiring Fund in connection with the BHV Merger, the BKN Merger, the MIY Merger and the

MPA Merger (each, a “Merger”). Preferred shareholders of the Acquiring Fund are also being asked to vote as a separate class on a proposal to approve each Merger Agreement and the respective Merger.

The enclosed Joint Proxy Statement/Prospectus is only being delivered to the Funds’ common shareholders. The preferred shareholders of each Fund are also

being asked to attend the Special Meeting and to vote as a separate class with respect to the proposals described above. Each Fund is delivering to its preferred shareholders a separate proxy statement with respect to the proposals described above.

The Board of Directors or Board of Trustees, as applicable, of each Fund believes that the proposal that the common shareholders of its Fund are being

asked to vote upon is in the best interests of its respective Fund and its shareholders and unanimously recommends that you vote “FOR” such proposal.

Your vote is important. Attendance at the Special Meeting will be limited to each Fund’s shareholders as of [●], 2023, the record date for

the Special Meeting.

If your shares in a Fund are registered in your name, you may attend and participate in the Special Meeting at

https://meetnow.global/M4VASFL by entering the control number found in the shaded box on your proxy card on the date and time of the Special Meeting. You may vote during the Special Meeting by following the instructions that will be available

on the Special Meeting website during the Special Meeting.

If you are a beneficial shareholder of a Fund (that is if you hold your shares of a Fund

through a bank, broker, financial intermediary or other nominee) and want to attend the Special Meeting you must register in advance of the Special Meeting. To register, you must submit proof of your proxy power (legal proxy), which you can obtain

from your financial intermediary or other nominee, reflecting your Fund holdings along with your name and email address to Georgeson LLC, each Fund’s tabulator. You may email an image of your legal proxy to

shareholdermeetings@computershare.com. Requests for registration must be received no later than 5:00 p.m. (Eastern time) three business days prior to the Special Meeting date. You will receive a confirmation email from Georgeson LLC of your

registration and a control number and security code that will allow you to vote at the Special Meeting.

Even if you plan to attend the Special Meeting,

please promptly follow the enclosed instructions to submit voting instructions by telephone or via the Internet. Alternatively, you may submit voting instructions by signing and dating each proxy card or voting instruction form you receive, and if

received by mail, returning it in the accompanying postage-paid return envelope.

We encourage you to carefully review the enclosed materials, which explain the proposals in more detail. As a

shareholder, your vote is important, and we hope that you will respond today to ensure that your shares will be represented at the meeting. You may vote using one of the methods below by following the instructions on your proxy card or voting

instruction form(s):

| |

• |

|

By signing, dating and returning the enclosed proxy card or voting instruction form(s) in the postage-paid

envelope; or |

| |

• |

|

By participating at the Special Meeting as described above. |

If you do not vote using one of the methods described above, you may be called by Georgeson LLC, the Funds’ proxy solicitor, to vote your shares.

If you have any questions about the proposals to be voted on or the virtual Special Meeting, please call Georgeson LLC, the firm assisting us in the

solicitation of proxies, toll free at (866) 413-5899.

As always, we appreciate your support.

Sincerely,

JOHN M. PERLOWSKI

President and Chief Executive Officer of the Funds

Please vote now. Your vote is important.

To avoid the wasteful and unnecessary expense of further solicitation(s), we urge you to indicate your

voting instructions on the enclosed proxy card, date and sign it and return it promptly in the postage-paid envelope provided, or record your voting instructions by telephone or via the internet, no matter how large or small your holdings may be. If

you submit a properly executed proxy but do not indicate how you wish your common shares to be voted, your common shares will be voted “FOR” the proposal. If your common shares are held through a broker, you must provide voting

instructions to your broker about how to vote your common shares in order for your broker to vote your common shares as you instruct at the Special Meeting.

[●], 2023

IMPORTANT NOTICE

TO

COMMON SHAREHOLDERS OF

BLACKROCK VIRGINIA MUNICIPAL BOND TRUST

BLACKROCK INVESTMENT QUALITY MUNICIPAL TRUST, INC.

BLACKROCK MUNIYIELD MICHIGAN QUALITY FUND, INC.

BLACKROCK MUNIYIELD PENNSYLVANIA QUALITY FUND

BLACKROCK MUNIYIELD QUALITY FUND III, INC.

QUESTIONS & ANSWERS

Although we urge you to read the entire Joint Proxy Statement/Prospectus, we have provided for your convenience a brief overview of some of

the important questions concerning the joint special shareholder meeting (the “Special Meeting”) of BlackRock Virginia Municipal Bond Trust (“BHV”), BlackRock Investment Quality Municipal Trust, Inc. (“BKN”), BlackRock

MuniYield Michigan Quality Fund, Inc. (“MIY”), BlackRock MuniYield Pennsylvania Quality Fund (“MPA”) (collectively, the “Target Funds”) and BlackRock MuniYield Quality Fund III, Inc. (“MYI” or the

“Acquiring Fund” and collectively with the Target Funds, the “Funds,” and each, a “Fund”) and the proposals to be voted on. It is expected that the effective dates (collectively, the “Closing Date”) of the

Mergers will be sometime during the first half of 2024, but they may be at a different time as described in the Joint Proxy Statement/Prospectus.

The enclosed Joint Proxy Statement/Prospectus is being sent only to the common shareholders of the Funds. Each of BHV, MIY, MPA and the

Acquiring Fund is separately soliciting the votes of its holders of Variable Rate Demand Preferred Shares (“VRDP Shares” and the holders thereof, “VRDP Holders”) and BKN is separately soliciting the votes of its holders of

Variable Rate Muni Term Preferred Shares (“VMTP Shares” and the holders thereof, “VMTP Holders,” and such VMTP Shares together with VRDP Shares and the common shares of each Fund, the “Shares”), as applicable, through a

separate proxy statement.

| Q: |

Why is a shareholder meeting being held? |

| A: |

Common Shareholders of BlackRock Virginia Municipal Bond Trust (NYSE Ticker: BHV): You and the VRDP

Holders of BHV are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Merger (the “BHV Merger Agreement”) among BHV, the Acquiring Fund and a wholly-owned subsidiary of the Acquiring Fund (the “BHV

Merger Sub”) providing for the merger of BHV with and into the BHV Merger Sub (the “BHV Merger”). The BHV Merger Sub has been formed for the sole purpose of consummating the BHV Merger and will transfer its assets and liabilities to

the Acquiring Fund and dissolve as soon as practicable following the completion of the BHV Merger. |

BHV VRDP Holders are

also being asked to vote as a separate class on a proposal to approve the BHV Merger Agreement and the BHV Merger through a separate proxy statement.

Common Shareholders of BlackRock Investment Quality Municipal Trust, Inc. (NYSE Ticker: BKN): You and the VMTP Holders of BKN are

being asked to vote as a single class on a proposal to approve an Agreement and Plan of Merger (the “BKN Merger Agreement”) among BKN, the Acquiring Fund and a wholly-owned subsidiary of the Acquiring Fund (the “BKN Merger Sub”)

providing for the merger of BKN with and into the BKN Merger Sub (the “BKN Merger”). The BKN Merger Sub has been formed for the sole purpose of consummating the BKN Merger and will transfer its assets and liabilities to the Acquiring Fund

and dissolve as soon as practicable following the completion of the BKN Merger. If the BKN Merger Agreement is approved by the requisite shareholders, BKN will redeem all of its outstanding VMTP Shares prior to the Closing Date of the BKN Merger.

BKN may issue, prior to the Closing Date of the BKN Merger, VRDP Shares with terms substantially identical to the terms of the Acquiring Fund VRDP Shares and use the proceeds from such issuance for the redemption of all of the outstanding VMTP

Shares of BKN (the “VMTP Refinancing”). If BKN has any VMTP Shares outstanding as of, and the VMTP Refinancing is not completed prior to, the Closing Date of the BKN Merger, then the BKN Merger will not be consummated.

BKN VMTP Holders are also being asked to vote as a separate class on a proposal to approve the

BKN Merger Agreement and the BKN Merger through a separate proxy statement.

Common Shareholders of BlackRock MuniYield Michigan Quality

Fund, Inc. (NYSE Ticker: MIY): You and the VRDP Holders of BHV are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Merger (the “MIY Merger Agreement”) among MIY, the Acquiring Fund and a

wholly-owned subsidiary of the Acquiring Fund (the “MIY Merger Sub”) providing for the merger of MIY with and into the MIY Merger Sub (the “MIY Merger”). The MIY Merger Sub has been formed for the sole purpose of consummating the

MIY Merger and will transfer its assets and liabilities to the Acquiring Fund and dissolve as soon as practicable following the completion of the MIY Merger.

MIY VRDP Holders are also being asked to vote as a separate class on a proposal to approve the MIY Merger Agreement and the MIY Merger through

a separate proxy statement.

Common Shareholders of BlackRock MuniYield Pennsylvania Quality Fund (NYSE Ticker: MPA): You and the

VRDP Holders of MPA are being asked to vote as a single class on a proposal to approve an Agreement and Plan of Merger (the “MPA Merger Agreement” and collectively with the BHV Merger Agreement, BKN Merger Agreement and MIY Merger

Agreement, the “Merger Agreements”) among MPA, the Acquiring Fund and a wholly-owned subsidiary of the Acquiring Fund (the “MPA Merger Sub” and collectively with the BHV Merger Sub, the BKN Merger Sub and the MIY Merger Sub, the

“Merger Subs”) providing for the merger of MPA with and into the MPA Merger Sub (the “MPA Merger” and collectively with the BHV Merger, the BKN Merger and the MIY Merger, the “Mergers”). The MPA Merger Sub has been

formed for the sole purpose of consummating the MPA Merger and will transfer its assets and liabilities to the Acquiring Fund and dissolve as soon as practicable following the completion of the MPA Merger.

MPA VRDP Holders are also being asked to vote as a separate class on a proposal to approve the MPA Merger Agreement and the MPA Merger through

a separate proxy statement.

Common Shareholders of BlackRock MuniYield Quality Fund III, Inc. (NYSE Ticker: MYI): You and the

Acquiring Fund VRDP Holders are being asked to vote as a single class on a proposal to approve the issuance of additional common shares of the Acquiring Fund in connection with each Merger Agreement (each, an “Issuance” and collectively,

the “Issuances”).

Acquiring Fund VRDP Holders are also being asked to vote as a separate class on a proposal to approve each

Merger Agreement, including the issuance of additional Acquiring Fund VRDP Shares, through a separate proxy statement.

The term

“Combined Fund” refers to the Acquiring Fund as the surviving Fund after the consummation of each of the Mergers.

The BKN Merger

is contingent upon the completion of the VMTP Refinancing if BKN does not redeem all of its VMTP Shares following shareholder approval of the BKN Merger. If BKN has any VMTP Shares outstanding as of, and the VMTP Refinancing is not completed prior

to, the Closing Date of the BKN Merger, then the BKN Merger will not be consummated.

No Merger is contingent upon the approval of any

other Merger. If a Merger is not consummated, the Fund(s) for which such Merger(s) was not consummated would continue to exist and operate on a standalone basis.

| Q: |

Why has each Fund’s Board recommended these proposals? |

| A: |

The Board of Directors or Board of Trustees, as applicable (each, a “Board” and each member thereof,

a “Board Member”), of each Fund has determined that its Merger(s) is in the best interests of its Fund and that the interests of existing common shareholders and preferred shareholders of its Fund will not be diluted with respect to net

asset value (“NAV”) and liquidation preference, respectively, as a result of the Merger. The Mergers seek to achieve certain economies of scale and other operational efficiencies by combining five funds that have similar investment

objectives and similar investment strategies, policies and restrictions and are managed by the same investment adviser, BlackRock Advisors, LLC (the “Investment Advisor”). |

ii

In light of these similarities, the Mergers are intended to reduce fund redundancies and create a

single, larger fund that may benefit from anticipated operating efficiencies and economies of scale. The Mergers are intended to result in the following potential benefits to common shareholders:

| |

(i) |

lower net total expenses (after fees waived and excluding interest expense) per Common Share for common

shareholders of each Fund (as common shareholders of the Combined Fund following the Mergers) due to economies of scale resulting from the larger size of the Combined Fund; |

| |

(ii) |

improved net earnings yield on NAV and tax-equivalent yield on NAV for

common shareholders of each Fund other than the Acquiring Fund; |

| |

(iii) |

higher distribution rate for common shareholders of each Fund; |

| |

(iv) |

improved secondary market trading of the common shares of the Combined Fund; and |

| |

(v) |

operating and administrative efficiencies for the Combined Fund, including the potential for the following:

|

| |

(a) |

greater investment flexibility and investment options; |

| |

(b) |

greater diversification of portfolio investments; |

| |

(c) |

the ability to trade portfolio securities in larger positions and more favorable transaction terms;

|

| |

(d) |

additional sources of leverage or more competitive leverage terms and more favorable transaction terms;

|

| |

(e) |

benefits from having fewer closed-end funds offering similar products

in the market, including an increased focus by investors on the remaining funds in the market (including the Combined Fund) and additional research coverage; and |

| |

(f) |

benefits from having fewer similar funds in the same fund complex, including a simplified operational model and

a reduction in risk of operational, legal and financial errors. |

The Board of each Fund, including Board Members thereof

who are not “interested persons” (as defined in the Investment Company Act of 1940, as amended (the “1940 Act”), approved its Merger Agreement(s) and the Issuances, as applicable, concluding that the Merger(s) is in the best

interests of its Fund and that the interests of existing common shareholders and preferred shareholders of its Fund will not be diluted with respect to NAV and liquidation preference, respectively, as a result of the Merger(s). As a result of the

Mergers, however, common and preferred shareholders of each Fund may hold a reduced percentage of ownership in the larger Combined Fund than they did in any of the individual Funds before the Mergers. Each Board’s conclusion was based on each

Board Member’s business judgment after consideration of all relevant factors taken as a whole with respect to its Fund and the Fund’s common and preferred shareholders, although individual Board Members may have placed different weight on

various factors and assigned different degrees of materiality to various factors.

Because the shareholders of each Fund will vote

separately on the Fund’s respective Merger(s) or Issuances, as applicable, and the BKN Merger is contingent upon the completion of the VMTP Refinancing if BKN does not redeem all of its VMTP Shares following shareholder approval of the BKN

Merger, there are multiple potential combinations of Mergers. To the extent either Merger is not completed, any expected expense savings by the Combined Fund, or other potential benefits resulting from the Mergers, may be reduced.

If a Merger is not consummated, then the Investment Advisor may, in connection with ongoing management of the Fund for which such Merger(s) was

not consummated and its product line, recommend alternative proposals to the Board of that Fund.

| Q: |

How will the Mergers affect the fees and expenses of the Funds? |

| A: |

For the 12-month period ended July 31, 2023, the Total Expense

Ratios of BHV, BKN, MIY, MPA and MYI were 4.46%, 3.40%, 3.27%, 3.03% and 3.15%, respectively. “Total Expenses” means a Fund’s total annual operating expenses (including interest expense and acquired fund fees and expenses).

“Total Expense Ratio” means a Fund’s Total Expenses expressed as a percentage of its average net assets attributable to its common shares. |

iii

Each Fund and the Investment Advisor have entered into a fee waiver agreement (the “Fee

Waiver Agreement”), pursuant to which the Investment Advisor has contractually agreed to waive the management fee with respect to any portion of each Fund’s assets attributable to investments in any equity and fixed-income mutual funds and

exchange-traded funds (“ETFs”) managed by the Investment Advisor or its affiliates that have a contractual fee, through June 30, 2025 (the “Affiliated Mutual Fund and ETF Waiver”). In addition, pursuant to the Fee Waiver

Agreement, the Investment Advisor has contractually agreed to waive its management fees by the amount of investment advisory fees each Fund pays to the Investment Advisor indirectly through its investment in money market funds advised by the

Investment Advisor or its affiliates, through June 30, 2025 (the “Affiliated Money Market Fund Waiver” and together with the Affiliated Mutual Fund and ETF Waiver, the “Affiliated Fund Waiver”). The Fee Waiver Agreement may

be continued from year to year thereafter, provided that such continuance is specifically approved by the Investment Advisor and each Fund (including by a majority of each Fund’s Independent Board Members). Neither the Investment Advisor nor

the Funds are obligated to extend the Fee Waiver Agreement. The Fee Waiver Agreement may be terminated at any time, without the payment of any penalty, only by each Fund (upon the vote of a majority of the Independent Board Members or a majority of

the outstanding voting securities of each Fund), upon 90 days’ written notice by each Fund to the Investment Advisor.

With respect to

BHV, the Investment Advisor has voluntarily agreed to waive a portion of its investment management fee equal to an annual rate of 0.13% of the average weekly managed assets (as defined below) (the “BHV Voluntary Waiver”). The BHV Voluntary

Waiver may be reduced or discontinued at any time.

If any of the Mergers are consummated, the Investment Advisor has contractually agreed

to waive a portion of its investment management fee equal to an annual rate of 0.01% of the average daily net assets (as defined below) of the Combined Fund through June 30, 2025 (the “Combined Fund Contractual Waiver”). The Combined

Fund Contractual Waiver may be terminated prior to June 30, 2025 only by action of a majority of the Board Members who are not “interested persons” of the Combined Fund (as defined in the 1940 Act) or by a vote of the Combined

Fund’s outstanding voting securities.

In the Investment Advisor’s view, the most likely combination is the Mergers of all of the

Funds, which is also expected to result in the lowest Total Expense Ratio (after fees waived and excluding interest expense) for the Combined Fund. If the only Merger discussed in the Joint Proxy Statement/Prospectus that is completed is the Merger

of BHV into the Acquiring Fund, the Combined Fund would be expected to have a higher Total Expense Ratio than if any other combination of Mergers were completed. As of July 31, 2023, any combination of Mergers is expected to result in a Total

Expense Ratio (after fees waived and excluding interest expense) for the Combined Fund that is lower than the Total Expense Ratio of each Target Fund.

For the 12-month period ended July 31, 2023, for BHV, BKN, MIY and MPA, the Acquiring Fund and the

Combined Fund, the historical and pro forma Total Expense Ratios (after giving effect to the Affiliated Fund Waiver with respect to BHV and MPA, the BHV Voluntary Waiver and the Combined Fund Contractual Waiver) applicable to the

Mergers are as follows:

Total Expense Ratios Including Interest Expense

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| BHV |

|

BKN |

|

|

MIY |

|

|

MPA |

|

|

Acquiring Fund

(MYI) |

|

|

Pro forma

Combined

Fund

(BHV into

MYI) |

|

|

Pro forma

Combined Fund

(BHV, BKN,

MIY and MPA

into MYI) |

|

| 4.23%1 |

|

|

3.40 |

% |

|

|

3.27 |

% |

|

|

3.02 |

%2 |

|

|

3.15 |

% |

|

|

3.13 |

% |

|

|

3.11 |

% |

iv

| 1 |

Without giving effect to the Affiliated Fund Waiver or the BHV Voluntary Waiver, BHV’s Total Expense Ratio

(including interest expense) is 4.46%. |

| 2 |

Without giving effect to the Affiliated Fund Waiver, MPA’s Total Expense Ratio (including interest

expense) is 3.03%. |

Total Expense Ratios Excluding Interest Expense

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| BHV |

|

BKN |

|

|

MIY |

|

|

MPA |

|

|

Acquiring Fund

(MYI) |

|

|

Pro forma

Combined

Fund

(BHV into

MYI) |

|

|

Pro forma

Combined Fund

(BHV, BKN,

MIY and MPA

into MYI) |

|

| 1.77%1 |

|

|

0.93 |

% |

|

|

0.91 |

% |

|

|

0.96 |

%2 |

|

|

0.89 |

% |

|

|

0.87 |

% |

|

|

0.85 |

% |

| 1 |

Without giving effect to the Affiliated Fund Waiver or the BHV Voluntary Waiver, BHV’s Total Expense Ratio

(excluding interest expense) is 2.00%. |

| 2 |

Without giving effect to the Affiliated Fund Waiver, MPA’s Total Expense Ratio (excluding interest

expense) is 0.97%. |

The Funds estimate that the completion of all of the Mergers would result in a Total Expense

Ratio (including interest expense and after giving effect to the Combined Fund Contractual Waiver) for the Combined Fund of 3.11% on a historical and pro forma basis for the 12-month period ended

July 31, 2023, representing a reduction in the Total Expense Ratio (including interest expense and after giving effect to the Affiliated Fund Waiver with respect to BHV and the BHV Voluntary Waiver) for the common shareholders of BHV,

BKN, MIY and the Acquiring Fund by 1.12%, 0.29%, 0.16% and 0.04%, respectively, and an increase in the Total Expense Ratio (including interest expense and after giving effect to the Affiliated Fund Waiver with respect to MPA) for the common

shareholders of MPA by 0.09%. Without giving effect to the Affiliated Fund Waiver with respect to BHV and MPA, the BHV Voluntary Waiver (which may be reduced or discontinued at any time without notice) or the Combined Fund Contractual Waiver, the

Total Expense Ratio (including interest expense) for the common shareholders of BHV, BKN, MIY and the Acquiring Fund is expected to decrease by 1.33%, 0.27%, 0.14% and 0.02%, respectively, and the Total Expense Ratio (including interest

expense) for the common shareholders of MPA is expected to increase by 0.10%.

Each Fund’s Total Expenses include interest expense

associated with such Fund’s VRDP Shares or VMTP Shares, as applicable. The Funds estimate that the completion of all of the Mergers would result in a Total Expense Ratio (excluding interest expense and after giving effect to the Combined

Fund Contractual Waiver) for the Combined Fund of 0.85% on a historical and pro forma basis for the 12-month period ended July 31, 2023, representing a reduction in the Total Expense Ratios

(excluding interest expense and after giving effect to the Affiliated Fund Waiver with respect to BHV and MPA and the BHV Voluntary Waiver) for the common shareholders of BHV, BKN, MIY and MPA and the Acquiring Fund by 0.92%, 0.08%, 0.06%,

0.11% and 0.04%, respectively. Without giving effect to the Affiliated Fund Waiver with respect to BHV and MPA, the BHV Voluntary Waiver (which may be reduced or discontinued at any time without notice) or the Combined Fund Contractual Waiver, the

Total Expense Ratio (excluding interest expense) for the common shareholders of BHV, BKN, MIY and MPA and the Acquiring Fund is expected to decrease by 1.13%, 0.06%, 0.04%, 0.10% and 0.02%, respectively.

BHV currently pays the Investment Advisor a monthly fee at an annual contractual investment management fee rate of 0.65% of its average weekly

managed assets. BKN currently pays the Investment Advisor a monthly fee at an annual combined contractual investment management and contractual administration fee rate of 0.50% of its average weekly managed assets (comprised of an annual contractual

investment management fee rate of 0.35% of its average weekly managed assets and an annual contractual administration fee rate of 0.15% average weekly managed assets). For BKN, the combined investment management and administration fee rate is being

used for comparison purposes because, unlike BKN, the contractual investment management fee rates for MPA, MIY, BHV and the Acquiring Fund include administrative services provided by the Investment Advisor to such Funds and such Funds do not pay

separate administration fees. Each of MPA and MIY currently pays the Investment Advisor a monthly fee at an annual contractual investment management fee rate of 0.49% of its average daily net assets. The Acquiring Fund currently pays the Investment

Advisor a monthly fee at an annual contractual investment management fee rate of 0.50% of its

v

average daily net assets. For purposes of calculating these fees, “net assets” mean the relevant Fund’s total assets minus the sum of its accrued liabilities (which does not

include liabilities represented by tender option bond trusts (“TOB Trusts”) and the liquidation preference of any outstanding preferred shares) and “managed assets” are determined as total assets of the Fund (including any assets

attributable to money borrowed for investment purposes) less the sum of its accrued liabilities (other than money borrowed for investment purposes). It is understood that the liquidation preference of any outstanding preferred shares (other than

accumulated dividends) and TOB Trusts is not considered a liability in determining the relevant Fund’s NAV.

If the Mergers are

consummated, the annual contractual investment management fee rate of the Acquiring Fund will be the annual contractual investment management fee rate of the Combined Fund, which will be 0.50% of the average daily net assets (as defined above) of

the Combined Fund. The Combined Fund will have a lower annual contractual investment management fee rate than BHV, the same combined annual contractual investment management and administration fee rate as BKN, a higher annual contractual investment

management fee rate than MIY and MPA, and the same annual contractual investment management fee rate as the Acquiring Fund. Additionally, if any of the Mergers are consummated, the Investment Advisor has agreed to the Combined Fund Contractual

Waiver through June 30, 2025, resulting in an actual investment management fee rate of 0.49% of the average daily net assets (as defined above) of the Combined Fund. Please see “Expense Table For Common Shareholders” in the Joint

Proxy Statement/Prospectus for additional information.

Based on a pro forma Broadridge peer expense universe for the Combined Fund,

the estimated total annual fund expense ratio (excluding investment-related expenses and taxes) is expected to be in the first quartile and contractual investment management fee rate and actual investment management fee rate over total assets are

each expected to be in the first quartile.

The level of expense savings (or increases) will vary depending on the combination of the Funds

in the Mergers, and furthermore, there can be no assurance that future expenses will not increase or that any expense savings for any Fund will be realized as a result of any Merger.

| Q: |

How will the Mergers affect the earnings, tax-equivalent yields, distributions and undistributed net income

of the Funds? |

| [A: |

The Combined Fund’s net earnings yield on NAV and tax-equivalent yield on NAV for common shareholders

following the Mergers are expected to be potentially higher than each Target Fund’s net earnings yield on NAV and tax-equivalent yield on NAV and potentially lower than the Acquiring Fund’s net earnings yield on NAV and tax-equivalent

yield on NAV, and the Combined Fund’s distribution rate on NAV for common shareholders following the Mergers is expected to be potentially higher than each Fund’s distribution rate on NAV for common shareholders. The table below sets out

the net earnings yield on NAV, tax-equivalent yield on NAV and distribution rate on NAV for common shareholders of each Fund and the pro forma Combined Fund as of July 31, 2023: |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Fund |

|

Net Earnings

Yield on NAV

(Annualized) |

|

|

Tax-Equivalent

Yield on

NAV

(Annualized)1 |

|

|

Distribution

Rate on NAV

(Annualized) |

|

| BHV |

|

|

1.54 |

% |

|

|

3.56 |

% |

|

|

2.56 |

% |

| BKN |

|

|

3.57 |

% |

|

|

5.95 |

% |

|

|

3.59 |

% |

| MIY |

|

|

3.18 |

% |

|

|

5.52 |

% |

|

|

3.20 |

% |

| MPA |

|

|

2.79 |

% |

|

|

5.12 |

% |

|

|

3.12 |

% |

| Acquiring Fund (MYI) |

|

|

3.73 |

% |

|

|

6.53 |

% |

|

|

3.88 |

% |

| Pro forma Combined Fund (BHV, BKN, MIY and MPA into MYI) |

|

|

3.63 |

% |

|

|

6.39 |

% |

|

|

3.89 |

% |

| |

1 |

Tax-exempt yield refers to the yield a taxable bond would have to earn in order to match, after taxes, the yield

available on a tax-exempt municipal bond. The highest federal individual income tax rate of 40.8% is assumed. The table above reflects each Fund’s tax-equivalent yield for the month ended July 31, 2023, annualized for a 12-month period.

|

The distribution level of any fund is subject to change based upon a number of factors, including the current and

projected level of the fund’s earnings, and may fluctuate over time; thus, subject to a number of other factors, including the fund’s distribution policy, a higher net earnings profile may potentially have a positive impact on such

fund’s distribution level over time. The Combined Fund’s earnings rate, tax-equivalent yield and distribution rate on NAV will change over time, and depending on market conditions, may be higher or lower than each Fund’s earnings and

distribution rate on NAV prior to the Mergers. A Fund’s earnings rate, tax-equivalent yield and net investment income are variables which depend on many factors, including its asset mix, portfolio turnover level, the amount of leverage utilized

by the Fund, the costs of such leverage, the performance of its investments, the movement of interest rates and general market conditions. In addition, the Combined Fund’s future earnings will vary depending upon the combination of completed

Mergers. There can be no assurance that the future earnings of a Fund, including the Combined Fund after the Mergers, will remain constant.

If the Mergers are approved by shareholders, then the greater of (1) substantially all of the undistributed net investment income

(“UNII”), if any, or (2) the monthly distribution of each Fund is expected to be declared to such Fund’s common shareholders prior to the Closing Date (the “Pre-Merger Declared UNII

Distributions”). The declaration date, ex-dividend date (the “Ex-Dividend Date”) and record date of the Pre-Merger

Declared UNII Distributions will occur prior to the Closing Date. However, all or a significant portion of the Pre-Merger Declared UNII Distributions may be paid in one or more distributions to common

shareholders of the Funds entitled to such Pre-Merger Declared UNII Distributions after the Closing Date. Former BHV, BKN, MIY and MPA shareholders entitled to such

Pre-Merger Declared UNII Distributions paid after the Closing Date will receive such distributions in cash for a partial month post-Merger.

vi

Persons who purchase common shares of any of the Funds on or after the Ex-Dividend Date for the Pre-Merger Declared UNII Distributions should not expect to receive any distributions from any Fund until distributions, if any, are declared by the

Board of the Combined Fund and paid to shareholders entitled to any such distributions. No such distributions are expected to be paid by the Combined Fund until at least approximately one month following the Closing Date.

Additionally, the Acquiring Fund, in order to seek to provide its common shareholders with distribution rate stability, may include in its Pre-Merger Declared UNII Distribution amounts in excess of its undistributed net investment income and net investment income accrued through the Closing Date; any such excess amounts are not expected to constitute a

return of capital. This would result in the Acquiring Fund issuing incrementally more common shares in the Mergers since its NAV as of the valuation time for the Mergers would be lower relative to a scenario where such excess amounts were not

included in the Acquiring Fund’s Pre-Merger Declared UNII Distribution.

The Combined Fund

may retain a lower UNII balance after the Mergers than the Acquiring Fund prior to the Mergers. A lower UNII balance for the Combined Fund relative to the UNII balance of the Acquiring Fund poses risks for shareholders of the Combined Fund. UNII

balances, in part, support the level of a fund’s regular distributions and provide a cushion in the event a fund’s net earnings for a particular distribution period are insufficient to support the level of its regular distribution for that

period. If the Combined Fund’s net earnings are below the level of its current distribution rate, the Combined Fund’s UNII balance could be more likely to contribute to a determination to decrease the Combined Fund’s distribution

rate, or could make it more likely that the Combined Fund will make distributions consisting in part of a return of capital to maintain the level of its regular distributions. See “Dividends and Distributions.” Moreover, because a

fund’s UNII balance, in part, supports the level of a fund’s regular distributions, the UNII balance of the Combined Fund could impact the trading market for the Combined Fund’s common shares and the magnitude of the trading discount

to NAV of the Combined Fund’s common shares. However, the Combined Fund is anticipated to benefit from a lower expense ratio (compared to BHV, BKN, MIY, MPA and the Acquiring Fund), a potentially higher net earnings profile (compared to MPA,

BHV and MYI) and other anticipated benefits of economies of scale as discussed herein. Each Fund, including the Combined Fund, reserves the right to change its distribution policy with respect to common share distributions and the basis for

establishing the rate of its distributions for the common shares at any time and may do so without prior notice to common shareholders. The payment of any distributions by any Fund, including the Combined Fund, is subject to, and will only be made

when, as, and if, declared by the Board of such Fund. There is no assurance the Board of any Fund, including the Combined Fund, will declare any distributions for such Fund.

To the extent any Pre-Merger Declared UNII Distribution is not an “exempt interest dividend”

(as defined in the Internal Revenue Code of 1986, as amended (the “Code”)), the distribution may be taxable to shareholders for U.S. federal income tax purposes.]

| Q: |

Have common shares of each Fund historically traded at a premium or discount? |

| A: |

The common shares of each Fund have historically traded at both a premium and a discount. The table below sets

forth the market price, NAV, and the premium/discount to NAV of each Fund as of [●], 2023. |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Fund |

|

Market Price |

|

|

NAV |

|

|

Premium/(Discount) to NAV |

|

| BHV |

|

$ |

[●] |

|

|

$ |

[●] |

|

|

|

[●] |

% |

| BKN |

|

$ |

[●] |

|

|

$ |

[●] |

|

|

|

[●] |

% |

| MIY |

|

$ |

[●] |

|

|

$ |

[●] |

|

|

|

[●] |

% |

| MPA |

|

$ |

[●] |

|

|

$ |

[●] |

|

|

|

[●] |

% |

| Acquiring Fund (MYI) |

|

$ |

[●] |

|

|

$ |

[●] |

|

|

|

[●] |

% |

To the extent BHV’s, BKN’s, MIY’s and MPA’s common shares are trading at a wider discount

(or a narrower premium) than the Acquiring Fund at the time of its Merger, BHV, BKN, MIY and MPA’s common shareholders would have the potential for an economic benefit by the narrowing of the discount or widening of the premium. To the extent

BHV’s, BKN’s, MIY’s and MPA’s common shares are trading at a narrower discount (or wider premium) than the Acquiring Fund at the time of its Merger, BHV’s, BKN’s, MIY’s and MPA’s common shareholders may be

vii

negatively impacted if its Merger is consummated. Acquiring Fund common shareholders would only benefit from a premium/discount perspective to the extent the post-Merger discount (or premium) of

the Acquiring Fund common shares improves.

There can be no assurance that, after the Mergers, common shares of the Combined Fund will

trade at a narrower discount to NAV or wider premium to NAV than the common shares of any individual Fund prior to the Mergers. Upon consummation of the Mergers, the Combined Fund common shares may trade at a price that is less than the current

market price of Acquiring Fund common shares. In the Mergers, common shareholders of BHV, BKN, MIY and MPA will receive Acquiring Fund common shares based on the relative NAVs (not the market values) of the respective Fund’s common shares. The

market value of the common shares of the Combined Fund may be less than the market value of the common shares of each respective Fund prior to the Mergers.

| Q: |

How have the Funds historically performed compared to the Acquiring Fund? |

| A: |

The Acquiring Fund outperformed each Target Fund on a NAV basis for the one-, five- and ten-year periods ended December 31, 2022, with certain exceptions indicated in the table below. The performance table below illustrates the past performance of an investment in common shares of each Fund by

setting forth the average total returns based on NAV for the Funds for the periods indicated. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

Annualized Rates of Return |

|

| |

|

|

|

One Year ended

December 31, 2022

based on NAV |

|

|

Five Year ended

December 31, 2022

based on NAV |

|

|

Ten Year ended

December 31, 2022

based on NAV |

|

| BlackRock Virginia Municipal Bond Trust |

|

BHV |

|

|

(18.57 |

)% |

|

|

(0.93 |

)% |

|

|

1.29 |

% |

| BlackRock Investment Quality Municipal Trust, Inc. |

|

BKN |

|

|

(17.70 |

)% |

|

|

0.65 |

% |

|

|

3.41 |

% |

| BlackRock MuniYield Michigan Quality Fund, Inc. |

|

MIY |

|

|

(14.99 |

)% |

|

|

0.62 |

% |

|

|

2.92 |

% |

| BlackRock MuniYield Pennsylvania Quality Fund |

|

MPA |

|

|

(16.84 |

)% |

|

|

0.55 |

% |

|

|

2.65 |

% |

| BlackRock MuniYield Quality Fund III, Inc. (Acquiring Fund) |

|

MYI |

|

|

(16.26 |

)% |

|

|

1.14 |

% |

|

|

3.06 |

% |

A Fund’s past performance does not indicate or guarantee how its common shares will perform in the

future. Investment return and principal value of an investment will fluctuate so that the common shares, when sold, may be worth more or less than the original cost. Current performance may be lower or higher than the performance quoted, and numbers

may reflect small variances due to rounding. Standardized performance and performance data current to the most recent month end may be obtained by visiting the “Closed-End Funds” section of

www.blackrock.com. References to BlackRock’s website are intended to allow investors public access to information regarding the Funds and do not, and are not intended to, incorporate BlackRock’s website in the Joint Proxy

Statement/Prospectus.

| Q: |

How will holders of preferred shares be affected by the Mergers? |

| A: |

As of the date of the enclosed Joint Proxy Statement/Prospectus, each of BHV, MIY, MPA and the Acquiring Fund

has VRDP Shares outstanding and BKN has VMTP Shares outstanding. As of July 31, 2023, BHV had 116 Series W-7 VRDP Shares outstanding, MIY had 2,319 Series W-7 VRDP

Shares outstanding, MPA had 826 Series W-7 VRDP Shares outstanding, the Acquiring Fund had 3,564 Series W-7 VRDP Shares outstanding and BKN has 1,259 Series W-7 VMTP Shares outstanding. |

Pursuant to the VMTP Redemption, if the BKN Merger

Agreement is approved by the requisite shareholders, BKN will redeem all of its outstanding VMTP Shares prior to the Closing Date of the BKN Merger. Pursuant to the VMTP Refinancing, any outstanding VMTP Shares of BKN may be refinanced into BKN VRDP

Shares, with terms substantially identical to those of the Acquiring Fund’s VRDP Shares. The dividend rate of the BKN VRDP Shares to be issued in the BKN VMTP Refinancing will be based on the sum of the Securities Industry and Financial Markets

Association Municipal Swap Index and a percentage per annum based on the long-term ratings assigned to the VRDP Shares, whereas the current dividend rate of the currently outstanding BKN VMTP Shares is based on a variable rate set weekly at a fixed

rate spread to the Secured Overnight Financing Rate (SOFR). See “Information About the Preferred Shares of the Funds” in the Joint Proxy Statement/Prospectus for additional information about the preferred shares of each Fund.

The Board of each Fund has authorized the redemption of up to 100% of the Fund’s currently outstanding VRDP Shares or VMTP Shares, as

applicable, in connection with its respective Merger(s) prior to the Closing Date of such Merger(s). Any such redemption by a Target Fund would occur following shareholder approval of the Target Fund’s Merger, and any such redemption by the

Acquiring Fund would occur following shareholder approval of any one of the Mergers. In addition, the Board of each Fund has authorized the redemption of up to 67% of the Fund’s currently outstanding VRDP Shares or VMTP Shares, as applicable,

on one or more occasions between October 11, 2023 and April 1, 2024. Any such redemption is not related to a Fund’s Merger(s) or contingent on shareholder approval of a Fund’s Merger(s).

In connection with the Mergers, assuming that no BHV, MIY or MPA VRDP Shares are redeemed prior to the applicable Closing Date and BKN

refinances all of its currently outstanding VMTP Shares into VRDP Shares in the VMTP Refinancing prior to the Closing Date of the BKN Merger, the Acquiring Fund expects to issue 116 additional

viii

VRDP Shares to BHV VRDP Holders, 1,259 additional VRDP Shares to BKN VRDP Holders, 2,319 additional VRDP Shares to MIY VRDP Holders and 826 additional VRDP Shares to MPA VRDP Holders. Following

the completion of the Mergers, based on the Fund’s preferred shares currently outstanding, the Combined Fund is expected to have 8,084 VRDP Shares outstanding. If any Fund partially or fully redeems its preferred shares, the Combined Fund will

have fewer than 8,084 VRDP Shares outstanding, or possibly no VRDP Shares outstanding, following the completion of the Mergers.

Assuming

all of the Mergers are approved by shareholders, the Target Funds do not redeem all of their preferred shares prior to the Closing Date of the Mergers and the VMTP Refinancing, if any, is completed prior to the Closing Date of the BKN Merger, upon

the Closing Date of the Mergers, Target Fund VRDP Holders will receive on a one-for-one basis one newly issued Acquiring Fund VRDP Share, par value $0.10 per share and

with a liquidation preference of $100,000 per share (plus any accumulated and unpaid dividends that have accrued on the Target Fund VRDP Shares up to and including the day immediately preceding the Closing Date if such dividends have not been paid

prior to the Closing Date), in exchange for each Target Fund VRDP Share held by the Target Fund VRDP Holders immediately prior to the Closing Date. The newly issued Acquiring Fund VRDP Shares may be of the same series as the Acquiring Fund’s

outstanding VRDP Shares or a substantially identical series. No fractional Acquiring Fund VRDP Shares will be issued. The terms of the Acquiring Fund VRDP Shares to be issued in connection with the Mergers will be substantially identical to the

terms of the Acquiring Fund’s outstanding VRDP Shares and will rank on parity with the Acquiring Fund’s outstanding VRDP Shares as to the payment of dividends and the distribution of assets upon dissolution, liquidation or winding up of

the affairs of the Acquiring Fund. The newly issued Acquiring Fund VRDP Shares will be subject to the same special rate period (including the terms thereof) applicable to the outstanding Acquiring Fund VRDP Shares as of the Closing Date of the

Merger. Such special rate period will terminate on June 19, 2024, unless extended. The Mergers will not result in any changes to the terms of the Acquiring Fund’s VRDP Shares currently outstanding.

The newly issued Acquiring Fund VRDP Shares will have terms that are similar to the terms of the outstanding Target Fund VRDP Shares, with

certain differences. The newly issued Acquiring Fund VRDP Shares will have terms that are substantially similar to the terms of the BKN VRDP Shares to be issued in connection with the VMTP Refinancing, if any. The VRDP Shares of BHV have a mandatory

redemption date of July 1, 2042, the VRDP Shares of MIY have a mandatory redemption date of May 1, 2041, and the VRDP Shares of MPA have a mandatory redemption date of June 1, 2041, while the newly issued Acquiring Fund VRDP Shares

are expected to have a mandatory redemption date of June 1, 2041. The VRDP Shares that will be issued be issued in connection with the VMTP Refinancing, if any, are expected to have a mandatory redemption date of June 1, 2041. A Fund may

designate any succeeding subsequent rate period of the VRDP Shares as a “special rate period” subject to the restrictions and requirements set forth in the governing instrument for such Fund’s VRDP Shares. During a special rate

period, a Fund may choose to modify the terms of the VRDP Shares as permitted by the governing instrument for such Fund’s VRDP Shares, including, for example, special provisions relating to the calculation of dividends and the redemption of the

VRDP Shares. The VRDP Shares of BHV, MIY, MPA and the Acquiring Fund are currently in a one year special rate period that will end on June 19, 2024, unless extended (each, a “Special Rate Period”). The terms of the special rate period

applicable to the newly issued Acquiring Fund VRDP Shares are expected to be identical to the terms of the Special Rate Period applicable to the outstanding Acquiring Fund VRDP Shares as of the Closing Date of the Merger. The transfer restrictions

applicable to the VRDP Shares of BHV, MIY, MPA and the Acquiring Fund during their respective Special Rate Periods are substantially similar.

None of the expenses of the Mergers are expected to be borne by the VRDP Holders or VMTP Holders, as applicable, of the Funds.

To the extent that the Acquiring Fund issues any new VRDP Shares in the Mergers, the VRDP Holders of each Fund, if any, will be VRDP Holders of

the larger Combined Fund that will have a larger asset base and more VRDP Shares outstanding than any Fund individually before the Mergers. With respect to matters requiring all preferred shareholders to vote separately or common and preferred

shareholders to vote together as a single class, following the Mergers, any VRDP Holders of the Combined Fund may hold a smaller percentage of the outstanding preferred shares of the Combined Fund as compared to their percentage holdings of

outstanding preferred shares, if any, of their respective Fund prior to the Mergers.

ix

| Q: |

How similar are the Funds? |

| A: |

The Funds have the same investment adviser, officers and directors/trustees. MPA is organized as a

Massachusetts business trust. BHV is organized as a statutory trust under the laws of the State of Delaware. BKN, MIY and the Acquiring Fund are each formed as a Maryland corporation. |

Each of the Funds has its common shares listed on the NYSE. BHV, MIY, MPA and the Acquiring Fund each has privately placed VRDP Shares

outstanding. BKN has privately placed VMTP Shares outstanding.

Each Fund is managed by a team of investment professionals led by Michael

Kalinoski, CFA, Kevin Maloney, CFA, Walter O’Connor, CFA, Christian Romaglino, CFA, Phillip Soccio, CFA and Kristi Manidis.

[Following the Mergers, it is expected that the Combined Fund will be managed by a team of investment professionals led by Michael Kalinoski,

CFA, Kevin Maloney, CFA, Walter O’Connor, CFA, Christian Romaglino, CFA, Phillip Soccio, CFA and Kristi Manidis.]

The investment

objective, significant investment strategies and operating policies, and investment restrictions of the Combined Fund will be those of the Acquiring Fund, which are similar to those of BHV, BKN, MIY and MPA, although there are some differences. For

purposes of the below comparisons, as applicable, “Managed Assets” means a Fund’s total assets (including any assets attributable to money borrowed for investment purposes) minus the sum of the Fund’s accrued liabilities (other

than money borrowed for investment purposes).

Investment Objective:

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

| BHV |

|

BKN |

|

MIY |

|

MPA |

|

Acquiring Fund

(MYI) |

| |

|

|

|

|

| The Fund’s investment objective is to provide current income exempt from regular federal income

taxes and Virginia personal income tax. |

|

The Fund’s investment objective is to provide high current income exempt from regular U.S. federal income tax consistent with the preservation of

capital. |

|

The Fund’s investment objective is to provide shareholders with as high a level of current income exempt from federal and Michigan income taxes as is

consistent with its investment policies and prudent investment management. |

|

The Fund’s investment objective is to provide shareholders with as high a level of current income exempt from U.S. federal and Pennsylvania income taxes as

is consistent with its investment policies and prudent investment management. |

|

The Fund’s investment objective is to provide stockholders with as high a level of current income exempt from federal income taxes as is

consistent with its investment policies and prudent investment management. |

Municipal Bonds: Below is a comparison of each Fund’s investment policy with respect to

municipal obligations issued by or on behalf of states, territories and possessions of the United States and their political subdivisions, agencies or instrumentalities, each of which pays interest that is excludable from gross income for federal

income tax purposes, in the opinion of bond counsel to the issuer, but is not excludable from gross income for certain state income tax purposes (“Municipal Bonds”). Unless otherwise noted, the term “Municipal Bonds” also

includes certain state Municipal Bonds, as applicable.

x

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

| BHV |

|

BKN |

|

MIY |

|

MPA |

|

Acquiring Fund

(MYI) |

| |

|

|

|

|

| Under normal market conditions, the Fund will invest at least 80% of its Managed Assets* in municipal bonds,

the interest of which is exempt from regular federal income tax and Virginia personal income tax. |

|

As a matter of fundamental policy, under normal market conditions, the Fund will invest at least 80% of its Managed Assets* in investments the income from which

is exempt from federal income tax (except that the interest may be subject to the federal alternative minimum tax). |

|

The Fund seeks to achieve its investment objective by investing at least 80% of an aggregate of the Fund’s net assets (including proceeds from the issuance

of any preferred stock) and the proceeds of any borrowings for investment purposes, in a portfolio of municipal obligations issued by or on behalf of the State of Michigan, its political subdivisions, agencies and instrumentalities and by other

qualifying issuers, each of which pays interest that, in the opinion of bond counsel to the issuer, is excludable from gross income for federal income tax purposes (except that the interest may be includable in taxable income for purposes of the

federal alternative minimum tax) and exempt from Michigan income taxes. |

|

The Fund seeks to achieve its investment objective by investing, as a fundamental policy, at least 80% of an aggregate of the Fund’s net assets (including

proceeds from the issuance of any preferred shares) and the proceeds of any borrowings for investment purposes, in a portfolio of municipal obligations issued by or on behalf of the State of Pennsylvania, its political subdivisions, agencies and

instrumentalities and by other qualifying issuers, each of which pays interest that, in the opinion of bond counsel to the issuer, is excludable from gross income for federal income tax purposes (except that the interest may be includable in

taxable income for purposes of the federal alternative minimum tax) and exempt from Pennsylvania income taxes. |

|

The Fund seeks to achieve its investment objective by investing at least 80% of an aggregate of the Acquiring Fund’s net assets

(including proceeds from the issuance of any preferred stock) and the proceeds of any borrowings for investment purposes, in a portfolio of municipal obligations issued by or on behalf of states, territories and possessions of the United States and

their political subdivisions, agencies or instrumentalities, each of which pays interest that, in the opinion of bond counsel to the issuer, is excludable from gross income for federal income tax purposes (except that the interest may be

includable in taxable income for purposes of the federal alternative minimum tax). |

| |

* |

“Managed Assets” means BKN’s total assets (including any assets attributable to money borrowed

for investment purposes) minus the sum of BKN’s accrued liabilities (other than money borrowed for investment purposes). |

Investment Grade and Non-Investment Grade Securities: Below is a comparison of each

Fund’s policy with respect to investment in investment grade quality securities and non-investment grade quality securities. Investment grade quality means that such bonds are rated, at the time of

investment, within the four highest grades (Baa or BBB or better by Moody’s Investor Service, Inc. (“Moody’s”), S&P Global Ratings (“S&P”) or Fitch Ratings (“Fitch”)) or are unrated but judged to be of

comparable quality by the Investment Advisor. Below investment grade quality means

xi

securities rated at the time of purchase Ba or below by Moody’s, BB or below by S&P or Fitch, or securities determined by the Investment Advisor to be of comparable quality. Below

investment grade quality is regarded as predominantly speculative with respect to the issuer’s capacity to pay interest and repay principal. Such securities commonly are referred to as “high yield” or “junk” bonds.

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

| BHV |

|

BKN |

|

MIY |

|

MPA |

|

Acquiring Fund

(MYI) |

| |

|

|

|

|

| Under normal market conditions, the Fund invests at least 80% of its Managed Assets in investment grade quality

municipal bonds. BHV may invest up to 20% of its Managed Assets in municipal bonds that are rated, at the time of investment, Ba/BB or B by Moody’s, S&P or Fitch or that are unrated but judged to be of comparable quality by the Investment

Advisor |

|

Under normal market conditions, BKN will invest at least 80% of its Managed Assets in investment quality securities. BKN may invest up to 20% of its Managed

Assets, measured at the time of investment, in securities rated BB/Ba or B by Moody’s S&P, Fitch or another nationally recognized rating agency or, if unrated, deemed to be of comparable credit quality by the Investment Advisor. |

|

Under normal market conditions, the Fund expects to invest primarily in a portfolio of long-term Municipal Bonds that are commonly referred to as

“investment grade” securities. The Fund may invest up to 20% of its managed assets in securities that are rated below investment grade. |

|

Under normal market conditions, the Fund expects to invest primarily in a portfolio of long-term Municipal Bonds that are commonly referred to as

“investment grade” securities. BHV may invest up to 20% of its Managed Assets in municipal bonds that are rated, at the time of investment, Ba/BB or B by Moody’s, S&P or Fitch or that are unrated but judged to be of comparable

quality by the Investment Advisor |

|

Under normal market conditions, the Fund expects to invest primarily in a portfolio of long-term Municipal Bonds that are commonly referred

to as “investment grade” securities. The Fund may invest up to 20% of its managed assets in securities that are rated below investment grade. |

Bond Maturity: Below is a comparison of each Fund’s policy with respect to bond maturity.

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

| BHV |

|

BKN |

|

MIY |

|

MPA |

|

Acquiring Fund

(MYI) |

| |

|

|

|

|

| The average maturity of the Fund’s portfolio securities will vary based upon the Investment Advisor’s

assessment of economic and market conditions. The Fund’s portfolio at any given time may include both long-term and intermediate-term municipal bonds. |

|

The average maturity of the Fund’s portfolio securities varies from time to time based upon an assessment of economic and market conditions by the

Investment Advisor. The Fund’s portfolio at any given time may include both long- term and intermediate-term Municipal Bonds. |

|

The average maturity of Fund’s portfolio securities varies from time to time based upon an assessment of economic and market conditions by the Investment

Advisor. The Fund’s portfolio at any given time may include both long-term and intermediate-term municipal bonds |

|

The average maturity of the Fund’s portfolio securities varies from time to time based upon an assessment of economic and market conditions by the

Investment Advisor. The Fund’s portfolio at any given time may include long-term, intermediate-term and short-term Municipal Bonds. |

|

The average maturity of the Fund’s portfolio securities varies from time to time based upon an assessment of economic and market

conditions by the Investment Advisor. The Acquiring Fund’s portfolio at any given time may include both long-term and intermediate-term municipal bonds. |

xii

Each Fund utilizes leverage through the issuance of VRDP Shares or VMTP Shares and tender option

bonds (“TOBs”). See “The Acquiring Fund’s Investments—Leverage;” “General Risks of Investing in the Acquiring Fund—Leverage Risk;” and “General Risks of Investing in the Acquiring Fund—Tender

Option Bond Risk.” The Acquiring Fund may continue to leverage its assets after the Closing Date of the Mergers through the use of VRDP Shares and TOBs. As noted above, the Board of the Acquiring Fund has authorized the redemption of up to 100%

of the Acquiring Fund’s currently outstanding VRDP Shares or VMTP Shares, as applicable, in connection with the Mergers prior to the Closing Date of any of the Mergers, which redemption would occur following shareholder approval of a Merger,

and the redemption of up to 67% of the Fund’s currently outstanding VRDP Shares on one or more occasions between October 11, 2023 and April 1, 2024, which redemption is not subject to shareholder approval of any of the Mergers. After

the consummation of the Mergers, common shareholders of the Acquiring Fund, including former Target Fund common shareholders, will bear the leverage costs associated with any Acquiring Fund VRDP Shares and will be subject to the terms of any

Acquiring Fund VRDP Shares, including that the Acquiring Fund VRDP Shares will be senior in priority to the Acquiring Fund common shares as to the payment of dividends and the distribution of assets upon dissolution, liquidation or winding up of the

affairs of the Acquiring Fund. Please see “Information about the Preferred Shares of the Funds” for additional information about the preferred shares of each Fund.

The annualized dividend rates for the preferred shares for each Fund’s most recent fiscal year ended July 31, 2023 were as follows:

|

|

|

|

|

|

|

|

|

| Fund |

|

Preferred Shares |

|

|

Rate |

|

| BHV |

|

|

VRDP Shares |

|

|

|

3.61 |

% |

| BKN |

|

|

VMTP Shares |

|

|

|

4.05 |

% |

| MIY |

|

|

VRDP Shares |

|

|

|

3.61 |

% |

| MPA |

|

|

VRDP Shares |

|

|

|

3.61 |

% |

| Acquiring Fund (MYI) |

|

|

VRDP Shares |

|

|

|

3.61 |

% |

Please see below a comparison of certain important ratios related to (i) each Fund’s use of leverage

as of July 31, 2023, (ii) the Combined Fund’s estimated use of leverage, assuming only the Merger of BHV into the Acquiring Fund had taken place as of July 31, 2023, which represents the combination of completed Reorganizations

presented in the Joint Proxy Statement/Prospectus that would result in the highest asset coverage ratio for the Combined Fund, and (iii) the Combined Fund’s estimated use of leverage, assuming the Mergers of all the Funds had taken place

as of July 31, 2023, which represents, in the Investment Advisor’s view, the most likely combination of the Reorganizations and the combination of the Reorganizations that would result in the lowest asset coverage ratio for the Combined

Fund.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Ratios |

|

BHV |

|

|

BKN |

|

|

MIY |

|

|

MPA |

|

|

Acquiring Fund

(MYI) |

|

|

Pro forma

Combined

Fund

(BHV into

MYI) |

|

|

Pro forma

Combined Fund

(BHV, BKN,

MIY and MPA

into MYI) |

|

| Asset Coverage Ratio |

|

|

272.0 |

% |

|

|

283.0 |

% |

|

|

263.1 |

% |

|

|

306.4 |

% |

|

|

337.0 |

% |

|

|

335.0 |

% |

|

|

303.3 |

% |

| Regulatory Leverage Ratio(1) |

|

|

36.8 |

% |

|

|

35.3 |

% |

|

|

38.0 |

% |

|

|

32.6 |

% |

|

|

29.7 |

% |

|

|

29.9 |

% |

|

|

33.0 |

% |

| Effective Leverage Ratio(2) |

|

|

40.6 |

% |

|

|

36.6 |

% |

|

|

38.7 |

% |

|

|

36.2 |

% |

|

|

38.3 |

% |

|

|

38.40 |

% |

|

|

38.0 |

% |

| |

(1) |

Regulatory leverage consists of preferred shares issued by the Fund, which is a part of the Fund’s capital

structure. Regulatory leverage is sometimes referred to as “1940 Act Leverage” and is subject to asset coverage limits set forth in the 1940 Act. |

| |

(2) |

Effective leverage is a Fund’s effective economic leverage and includes both regulatory leverage and the

leverage effects of certain derivative investments in the Fund’s portfolio. Currently, the leverage effects of TOB inverse floater holdings, in addition to any regulatory leverage, are included in effective leverage ratios.

|

xiii

| Q: |

How will the Mergers be effected? |

| A: |

Assuming a Merger receives the requisite shareholder approvals, as well as certain consents, confirmations