false

0001576873

0001576873

2023-12-21

2023-12-21

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

8-K

CURRENT

REPORT

PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date

of Report (Date of earliest event reported): December 21, 2023

| AMERICAN

BATTERY TECHNOLOGY COMPANY |

| (Exact

name of registrant as specified in its charter) |

| Nevada

|

|

001-41811

|

|

33-1227980 |

| (State

or other jurisdiction of |

|

(Commission |

|

(IRS

Employer |

| incorporation

or organization) |

|

File

No.) |

|

Identification

Number) |

100

Washington Street, Suite 100

Reno,

NV |

|

89503

|

| (Address

of principal executive offices) |

|

(Zip

Code) |

(775)

473-4744

(Registrant’s

telephone number including area code)

N/A

(Former

name or former address, if changed since last report)

Check

the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under

any of the following provisions (see General Instruction A.2. below):

| ☐ |

Written

communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

|

| ☐ |

Soliciting

material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

|

| ☐ |

Pre-commencement

communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| |

|

| ☐ |

Pre-commencement

communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of Each Class |

|

Trading

Symbol(s) |

|

Name

of Each Exchange on Which Registered |

| Common

stock, $0.001 par value |

|

ABAT |

|

The

Nasdaq Stock Market LLC |

Indicate

by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405

of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging

growth company ☐

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item

8.01 Other Events.

On

January 18, 2024, American Battery Technology Company (“Company”) issued a press release announcing the completion of the

Updated Resource Estimate and Initial Assessment with Project Economics for the Tonopah Flats Lithium Project, Esmeralda and Nye Counties,

Nevada, USA (“Updated IA”) and the publication of the S-K 1300 Technical Report Summary (“TRS”) disclosing mineral

resources, including an initial economic assessment, for the Tonopah Flats Lithium Project. The TRS was completed by RESPEC Company LLC,

a qualified person, in compliance with Item 1300 of Regulation S-K and with an effective date of December 21, 2023.

A

copy of the press release is attached hereto as Exhibit 99.1 to this Current Report on Form 8-K and is incorporated herein by reference.

The final version of the Updated IA is filed as Exhibit 96.1 and the qualified person consent is filed as Exhibit 23.1 to this Current

Report on Form 8-K, each of which are incorporated herein by reference.

Item

9.01 Financial Statements and Exhibits.

(d)

Exhibits:

SIGNATURES

Pursuant

to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its

behalf by the undersigned hereunto duly authorized.

| |

AMERICAN

BATTERY TECHNOLOGY COMPANY |

| |

|

|

| Date:

January 22, 2024 |

By: |

/s/

Ryan Melsert |

| |

|

Ryan

Melsert |

| |

|

Chief

Executive Officer |

Exhibit 23.1

Exhibit 96.1

Exhibit

99.1

American

Battery Technology Company Announces Increased and Upgraded Lithium Resource to Measured and Indicated Classifications for One of the

Largest Lithium Projects in the United States

Company

continues to advance development of its Tonopah Flats Lithium Project, accelerating its path to commercialization of the domestic lithium

supply chain

Reno,

Nev., January 18, 2024 — American Battery Technology Company (ABTC) (NASDAQ:

ABAT), an integrated critical battery materials company that is commercializing its technologies for both primary battery minerals manufacturing

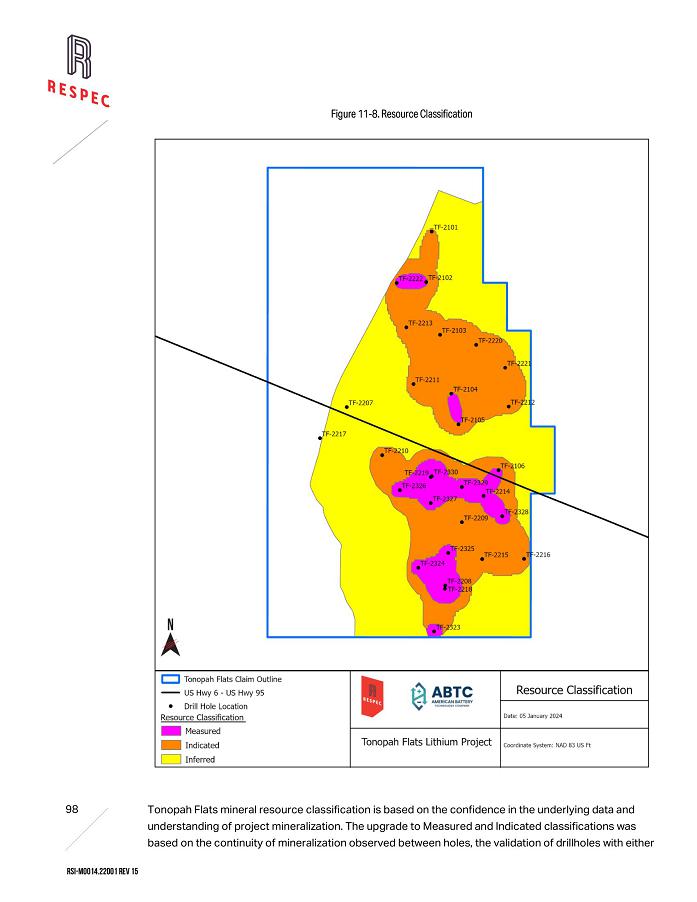

and secondary minerals lithium-ion battery recycling, is pleased to announce upgraded Measured Resource and Indicated Resource classifications

for its Tonopah Flats Lithium Project (TFLP) located in Big Smoky Valley near Tonopah, Nevada. The favorable announcement, published

in an S-K 1300 report titled Updated Resource Estimate and Initial Assessment with Project Economics for the Tonopah Flats Lithium

Project, Esmeralda and Nye Counties, Nevada, USA (Updated Initial Assessment), increases the resource’s classification

and attractiveness for commercialization.

In

December 2023, ABTC published its Initial Assessment for the TFLP which included data from its first two drill programs, and provided

a preliminary technical and economic study of the performance of the resource. The company’s Updated Initial Assessment incorporates

data from its third drill program, which results in an increase in total resource size and an upgraded classification for significant

portions of the resource.

| |

● |

Overall

increase in lithium resource size of 17% from the previous Initial Assessment |

| |

|

|

| |

● |

Approximately

54% of the resource is now classified at an upgraded classification as a Measured Resource or an Indicated Resource, representing

an increase in statistical confidence of quantity and quality of resource in progression of development towards commercialization |

| |

|

|

| |

● |

TFLP

continues to be one of the largest known lithium projects in the U.S., with a total quantified resource of 21.15 million tons of

lithium hydroxide monohydrate (LHM) |

| |

|

|

| |

● |

Deposit

remains unexplored and open to the South, Southwest, and at depth, allowing for potential to expand the resource with further drilling

in both the South and North claim blocks, however with a throughput of 33,000 tons LiOH/yr the current quantified resource already

has a mine life of over 400 years |

| |

|

|

| |

● |

Even

without incorporation of improved data from the third drill program, the TFLP demonstrates attractive after-tax cash flows: |

| |

|

|

| |

|

|

○ |

Net Present Value of $4.41 billion @10% discount rate |

| |

|

|

○ |

Internal Rate of Return of 65.8% |

| |

|

|

○ |

2.4-year payback period of initial investment |

| |

|

|

|

|

| |

● |

Updated

Initial Assessment provides necessary data and recommends next steps to further develop the resource, including the completion of

a Pre-Feasibility Study |

“We

are proud to have both further increased the total size of this critical material lithium resource through our step-out exploration,

and through our strategic infill drilling to have evolved the majority of this resource up to the Measured and Indicated classifications,”

stated ABTC CEO Ryan Melsert. “This is an important milestone in the commercialization of this deposit, and combined with the current

construction and installation of our integrated pilot system for the continuous demonstration of the manufacturing of battery grade lithium

hydroxide from this unconventional lithium resource, we are excited to continue the rapid development and commercialization of these

first-of-kind technologies.”

American

Battery Technology Company’s Measured, Indicated, and Inferred Lithium Mineral Resource

| Classification | |

Total kTons | | |

Average ppm Li | | |

Li kTons | | |

LHM kTons | |

| Measured | |

| 721,000 | | |

| 702 | | |

| 510 | | |

| 3,060 | |

| Indicated | |

| 2,439,000 | | |

| 565 | | |

| 1,380 | | |

| 8,340 | |

| Measured + Indicated | |

| 3,160,000 | | |

| 596 | | |

| 1,890 | | |

| 11,400 | |

| Inferred | |

| 2,931,000 | | |

| 550 | | |

| 1,610 | | |

| 9,750 | |

| Total | |

| 6,091,000 | | |

| 574 | | |

| 3,500 | | |

| 21,150 | |

|

This updated initial assessment utilized data from

ABTC’s recently completed Drill Program III, with samples collected at TFLP from eight core drill holes with approximately 6,700

feet of drilling.

“The data from this third drill program’s

additional eight core holes has resulted in increased level of confidence towards pre-feasibility and bankable feasibility status,”

stated ABTC Chief Mineral Resource Officer Scott Jolcover. “I am pleased with the updated report and excited to continue accelerated

development of this resource by furthering progress with the recommended next steps.”

The Updated Initial Assessment maintains the previously-published

Initial Assessment economic analysis and values, and notes that these values are conservative considering the improved updated classification

of the resource in the Updated Initial Assessment. It is expected that with future updates the project economics will improve.

As

noted in the December 2023 Initial Assessment, the TFLP has an estimated mine life of over 400 years with average annual production of

33,000 tons LHM. For purposes of the economic analysis, the Initial Assessment limits the project to a mine life of 50 years for

approximately 643.2 million tons of claystone processed with an average of 3,815ppm LHM grade processed. With $781.8 million in initial

capital costs, production costs of $4,636/ton of LHM, overall operating costs of $6,080/ ton of LHM produced, and average annual production

of 33,000 tons of LHM, the report estimates a $9.56 billion after-tax net present value (NPV) at a 5% discount rate.

|

|

Recommended

Next Steps for Project Commercialization:

| |

● |

Perform

expanded bench scale metallurgy, pit optimization, and engineering analyses to further refine processing operations |

| |

|

|

| |

● |

Further

develop the resource to achieve a Probable and/or Proven Mineral Reserve |

| |

|

|

| |

● |

Perform

Hydrological and Geotechnical Drill Programs of TFLP property |

| |

|

|

| |

● |

Complete

remaining baseline environmental studies and National Environmental Policy Act (NEPA) review process |

| |

|

|

| |

● |

Complete

Pre-Feasibility Study |

| |

|

|

| |

● |

Complete

commissioning and commence operations of ABTC integrated pilot refinery system that will process TFLP claystone materials, and utilize

this data from a continuously operating integrated pilot refinery to further optimize the design of the commercial-scale refinery

|

| |

|

|

| |

● |

Complete

commercial-scale engineering design, construction, and commissioning for ABTC’s commercial refinery with lead EPC firm Black

& Veatch |

The

information contained in this press release is qualified in its entirety by reference to the complete text of the Updated Initial Assessment

effective December 21, 2023, including but not limited to the mineral resource estimates and economic analysis. To read the full Updated

Initial Assessment, visit: www.americanbatterytechnology.com_TonopahFlats_MI-Resource-Update.

Qualified

Person

The

mineral resource estimates presented in the ABTC Tonopah Flats Initial Assessment were performed by third-party, qualified person RESPEC,

LLC and were classified by geological and quantitative confidence in accordance with the Securities and Exchange Commission (SEC) Regulation

S-K 1300.

Initial

Assessment

Initial

assessment is a preliminary technical and economic study of the economic potential of all or parts of mineralization to support the disclosure

of mineral resources. The initial assessment must be prepared by a qualified person and must include appropriate assessments of reasonably

assumed technical and economic factors, together with any other relevant operational factors, that are necessary to demonstrate at the

time of reporting that there are reasonable prospects for economic extraction. An initial assessment is required for disclosure of mineral

resources but cannot be used as the basis for disclosure of mineral reserves.

Inferred

Resource

Inferred

mineral resource is that part of a mineral resource for which quantity and grade or quality are estimated on the basis of limited geological

evidence and sampling. The level of geological uncertainty associated with an inferred mineral resource is too high to apply relevant

technical and economic factors likely to influence the prospects of economic extraction in a manner useful for evaluation of economic

viability. Because an inferred mineral resource has the lowest level of geological confidence of all mineral resources, which prevents

the application of the modifying factors in a manner useful for evaluation of economic viability, an inferred mineral resource may not

be considered when assessing the economic viability of a mining project, and may not be converted to a mineral reserve.

Indicated

Resource

Indicated

mineral resource is that part of a mineral resource for which quantity and grade or quality are estimated on the basis of adequate geological

evidence and sampling. The level of geological certainty associated with an indicated mineral resource is sufficient to allow a qualified

person to apply modifying factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit.

Because an indicated mineral resource has a lower level of confidence than the level of confidence of a measured mineral resource, an

indicated mineral resource may only be converted to a probable mineral reserve.

Measured

Resource

Measured

mineral resource is that part of a mineral resource for which quantity and grade or quality are estimated on the basis of conclusive

geological evidence and sampling. The level of geological certainty associated with a measured mineral resource is sufficient to allow

a qualified person to apply modifying factors, as defined in this section, in sufficient detail to support detailed mine planning and

final evaluation of the economic viability of the deposit. Because a measured mineral resource has a higher level of confidence than

the level of confidence of either an indicated mineral resource or an inferred mineral resource, a measured mineral resource may be converted

to a proven mineral reserve or to a probable mineral reserve.

Probable

Mineral Reserve

Probable

mineral reserve is the economically mineable part of an indicated and, in some cases, a measured mineral resource.

Proven

Mineral Reserve

Proven

mineral reserve is the economically mineable part of a measured mineral resource and can only result from conversion of a measured mineral

resource.

Pre-Feasibility

Study

A

preliminary feasibility study (or pre-feasibility study) is a comprehensive study of a range of options for the technical and economic

viability of a mineral project that has advanced to a stage where a qualified person has determined (in the case of underground mining)

a preferred mining method, or (in the case of surface mining) a pit configuration, and in all cases has determined an effective method

of mineral processing and an effective plan to sell the product. A pre-feasibility study includes a financial analysis based on reasonable

assumptions, based on appropriate testing, about the modifying factors and the evaluation of any other relevant factors that are sufficient

for a qualified person to determine if all or part of the indicated and measured mineral resources may be converted to mineral reserves

at the time of reporting. The financial analysis must have the level of detail necessary to demonstrate, at the time of reporting, that

extraction is economically viable. A pre-feasibility study is less comprehensive and results in a lower confidence level than a feasibility

study. A pre-feasibility study is more comprehensive and results in a higher confidence level than an initial assessment.

About

American Battery Technology Company

American

Battery Technology Company (ABTC), headquartered in Reno, Nevada, has pioneered first-of-kind technologies to unlock domestically manufactured

and recycled battery metals critically needed to help meet the significant demand from the electric vehicle, stationary storage, and

consumer electronics industries. Committed to a circular supply chain for battery metals, ABTC works to continually innovate and master

new battery metals technologies that power a global transition to electrification and the future of sustainable energy.

Forward-Looking

Statements

This

press release contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private

Securities Litigation Reform Act of 1995. All statements, other than statements of historical fact, are “forward-looking statements.”

Although the American Battery Technology Company’s (the “Company”) management believes that such forward-looking statements

are reasonable, it cannot guarantee that such expectations are, or will be, correct. These forward-looking statements involve a number

of risks and uncertainties, which could cause the Company’s future results to differ materially from those anticipated. Potential

risks and uncertainties include, among others, risks and uncertainties related to the Company’s ability to continue as a going

concern; interpretations or reinterpretations of geologic information, unfavorable exploration results, inability to obtain permits required

for future exploration, development or production, general economic conditions and conditions affecting the industries in which the Company

operates; the uncertainty of regulatory requirements and approvals; fluctuating mineral and commodity prices, final investment approval

and the ability to obtain necessary financing on acceptable terms or at all. Additional information regarding the factors that may cause

actual results to differ materially from these forward-looking statements is available in the Company’s filings with the Securities

and Exchange Commission, including the Annual Report on Form 10-K for the year ended June 30, 2023. The Company assumes no obligation

to update any of the information contained or referenced in this press release.

###

American

Battery Technology Company

Media

Contact:

Tiffiany

Moehring

tmoehring@batterymetals.com

720-254-1556

v3.23.4

| X |

- DefinitionBoolean flag that is true when the XBRL content amends previously-filed or accepted submission.

| Name: |

dei_AmendmentFlag |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionFor the EDGAR submission types of Form 8-K: the date of the report, the date of the earliest event reported; for the EDGAR submission types of Form N-1A: the filing date; for all other submission types: the end of the reporting or transition period. The format of the date is YYYY-MM-DD.

| Name: |

dei_DocumentPeriodEndDate |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:dateItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe type of document being provided (such as 10-K, 10-Q, 485BPOS, etc). The document type is limited to the same value as the supporting SEC submission type, or the word 'Other'.

| Name: |

dei_DocumentType |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:submissionTypeItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionAddress Line 1 such as Attn, Building Name, Street Name

| Name: |

dei_EntityAddressAddressLine1 |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionAddress Line 2 such as Street or Suite number

| Name: |

dei_EntityAddressAddressLine2 |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- Definition

+ References

+ Details

| Name: |

dei_EntityAddressCityOrTown |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionCode for the postal or zip code

| Name: |

dei_EntityAddressPostalZipCode |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionName of the state or province.

| Name: |

dei_EntityAddressStateOrProvince |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:stateOrProvinceItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionA unique 10-digit SEC-issued value to identify entities that have filed disclosures with the SEC. It is commonly abbreviated as CIK. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityCentralIndexKey |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:centralIndexKeyItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionIndicate if registrant meets the emerging growth company criteria. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityEmergingGrowthCompany |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionCommission file number. The field allows up to 17 characters. The prefix may contain 1-3 digits, the sequence number may contain 1-8 digits, the optional suffix may contain 1-4 characters, and the fields are separated with a hyphen.

| Name: |

dei_EntityFileNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:fileNumberItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTwo-character EDGAR code representing the state or country of incorporation.

| Name: |

dei_EntityIncorporationStateCountryCode |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:edgarStateCountryItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe exact name of the entity filing the report as specified in its charter, which is required by forms filed with the SEC. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityRegistrantName |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe Tax Identification Number (TIN), also known as an Employer Identification Number (EIN), is a unique 9-digit value assigned by the IRS. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityTaxIdentificationNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:employerIdItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionLocal phone number for entity.

| Name: |

dei_LocalPhoneNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 13e

-Subsection 4c

| Name: |

dei_PreCommencementIssuerTenderOffer |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 14d

-Subsection 2b

| Name: |

dei_PreCommencementTenderOffer |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTitle of a 12(b) registered security. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b

| Name: |

dei_Security12bTitle |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:securityTitleItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionName of the Exchange on which a security is registered. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection d1-1

| Name: |

dei_SecurityExchangeName |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:edgarExchangeCodeItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as soliciting material pursuant to Rule 14a-12 under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Section 14a

-Number 240

-Subsection 12

| Name: |

dei_SolicitingMaterial |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTrading symbol of an instrument as listed on an exchange.

| Name: |

dei_TradingSymbol |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:tradingSymbolItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as written communications pursuant to Rule 425 under the Securities Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Securities Act

-Number 230

-Section 425

| Name: |

dei_WrittenCommunications |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

American Battery Technol... (NASDAQ:ABAT)

Historical Stock Chart

Von Feb 2025 bis Mär 2025

American Battery Technol... (NASDAQ:ABAT)

Historical Stock Chart

Von Mär 2024 bis Mär 2025