UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended: November 30, 2023

☐ TRANSITION REPORT UNDER SECTION 13 OR 15(D) OF THE EXCHANGE ACT

For the transition period from to

Commission file number: 000-52838

DBMM GROUP

DIGITAL BRAND MEDIA & MARKETING GROUP, INC.

WWW.DBMMGROUP.COM

(Exact name of small business issuer as specified in its charter)

845 Third Avenue, 6th Floor, New York, NY 10022

(Address of principal executive offices)

Florida

State of incorporation

59-3666743

IRS Employer Identification No.

(646) 722-2706

(Issuer's telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such Files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ☐ Accelerated Filer ☐

Non-Accelerated Filer ☐ Smaller Reporting Company ☒

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes ☐ No ☒

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.001 par value | DBMM | OTC Markets |

Indicate the number of shares outstanding of each of the Issuer’s classes of common stock, as of the latest practicable date:

| Date | Shares Outstanding |

| January 16, 2024 | 825,218,631 |

INDEX

PART I. FINANCIAL INFORMATION

ITEM I. FINANCIAL STATEMENTS

|

DIGITAL BRAND MEDIA & MARKETING GROUP, INC. AND SUBSIDIARIES

|

|

|

CONSOLIDATED BALANCE SHEETS

|

|

| |

|

|

|

|

|

|

|

|

| |

|

(Unaudited)

|

|

|

(Audited)

|

|

| |

|

November 30,

|

|

|

August 31,

|

|

| |

|

2023

|

|

|

2023

|

|

|

ASSETS

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

CURRENT ASSETS

|

|

|

|

|

|

|

|

|

|

Cash

|

|

$ |

10,925 |

|

|

$ |

44,521 |

|

|

Accounts receivable, net

|

|

|

31,586 |

|

|

|

20,739 |

|

|

Prepaid expenses and other current assets

|

|

|

470 |

|

|

|

470 |

|

|

Total assets

|

|

$ |

42,981 |

|

|

$ |

65,730 |

|

| |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS' DEFICIT

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

CURRENT LIABILITIES

|

|

|

|

|

|

|

|

|

|

Accounts payable and accrued expenses

|

|

$ |

714,851 |

|

|

$ |

724,272 |

|

|

Accrued interest

|

|

|

1,312,921 |

|

|

|

1,189,387 |

|

|

Accrued compensation

|

|

|

1,283,436 |

|

|

|

1,313,536 |

|

|

Derivative liability

|

|

|

372,980 |

|

|

|

206,476 |

|

|

Loans payable, net

|

|

|

2,619,716 |

|

|

|

2,478,291 |

|

|

Officers loans payable

|

|

|

49,765 |

|

|

|

53,893 |

|

|

Convertible debentures, net

|

|

|

517,242 |

|

|

|

517,242 |

|

| |

|

|

6,870,911 |

|

|

|

6,483,097 |

|

| |

|

|

|

|

|

|

|

|

|

Loan payable, net of short-term portion

|

|

|

27,297 |

|

|

|

27,297 |

|

| |

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES

|

|

|

6,898,208 |

|

|

|

6,510,394 |

|

| |

|

|

|

|

|

|

|

|

|

STOCKHOLDERS' DEFICIT

|

|

|

|

|

|

|

|

|

| Preferred stock, Series 1, par value .001; authorized 2,000,000 shares; 1,995,185, and 1,995,185 shares issued and outstanding |

|

|

1,995 |

|

|

|

1,995 |

|

| Preferred stock, Series 2, par value .001; authorized 2,000,000 shares; 0 and 0 shares issued and outstanding |

|

|

- |

|

|

|

- |

|

| Common stock, par value .001; authorized 2,000,000,000 shares: 825,218,631 and 825,218,631 shares issued and outstanding |

|

|

825,218 |

|

|

|

825,218 |

|

|

Additional paid in capital

|

|

|

9,813,090 |

|

|

|

9,813,090 |

|

|

Other comprehensive loss

|

|

|

36,617 |

|

|

|

51,427 |

|

|

Accumulated deficit

|

|

|

(17,532,147 |

)

|

|

|

(17,136,394 |

)

|

| |

|

|

|

|

|

|

|

|

|

TOTAL STOCKHOLDERS' DEFICIT

|

|

$ |

(6,855,227 |

)

|

|

$ |

(6,444,664 |

)

|

| |

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIT

|

|

$ |

42,981 |

|

|

$ |

65,730 |

|

See Notes to Unaudited Consolidated Financial Statements.

|

DIGITAL BRAND MEDIA & MARKETING GROUP, INC. AND SUBSIDIARIES

|

|

|

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

|

|

| |

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended

November 30,

|

|

| |

|

2023

|

|

|

2022

|

|

| |

|

(Unaudited)

|

|

|

(Unaudited)

|

|

| |

|

|

|

|

|

|

|

|

|

Revenues

|

|

$ |

85,550 |

|

|

$ |

54,531 |

|

| |

|

|

|

|

|

|

|

|

|

Cost of revenues

|

|

|

74,339 |

|

|

|

27,078 |

|

|

Gross profit

|

|

|

11,211 |

|

|

|

27,453 |

|

| |

|

|

|

|

|

|

|

|

|

Operating expenses

|

|

|

|

|

|

|

|

|

|

Sales, general and administrative

|

|

|

116,707 |

|

|

|

148,704 |

|

|

Total operating expenses

|

|

|

116,707 |

|

|

|

148,704 |

|

|

Operating loss

|

|

|

(105,496 |

)

|

|

|

(121,251 |

)

|

| |

|

|

|

|

|

|

|

|

| Other income (expenses) |

|

|

|

|

|

|

|

|

|

Interest expense

|

|

|

(123,753 |

) |

|

|

(77,099 |

) |

|

Change in fair value of derivative liability

|

|

|

(166,504 |

) |

|

|

(166,320 |

) |

|

Total other (income) expenses, net

|

|

|

(290,257 |

) |

|

|

(243,419 |

) |

| |

|

|

|

|

|

|

|

|

|

Net loss

|

|

$ |

(395,753 |

) |

|

$ |

(364,670 |

)

|

| |

|

|

|

|

|

|

|

|

|

Other comprehensive income (loss)

|

|

|

|

|

|

|

|

|

|

Foreign exchange translation

|

|

|

(14,810 |

)

|

|

|

(35,006 |

)

|

|

Comprehensive income (loss)

|

|

|

(410,563 |

)

|

|

|

(399,676 |

)

|

| |

|

|

|

|

|

|

|

|

|

Net loss per share

|

|

|

|

|

|

|

|

|

|

Basic and diluted

|

|

$ |

(0.00 |

)

|

|

$ |

0.00 |

|

| |

|

|

|

|

|

|

|

|

|

WEIGHTED AVERAGE NUMBER OF SHARES

|

|

|

|

|

|

|

|

|

|

Basic and diluted

|

|

|

825,218,631 |

|

|

|

787,718,631 |

|

See Notes to Unaudited Consolidated Financial Statements.

|

DIGITAL BRAND MEDIA & MARKETING GROUP, INC., AND SUBSIDIARIES

|

|

|

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' DEFICIT

|

|

| |

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended

November 30,

|

|

| |

|

2023

|

|

|

2022

|

|

| |

|

(Unaudited)

|

|

|

(Unaudited)

|

|

| |

|

|

|

|

|

|

|

|

|

Series 1

|

|

|

|

|

|

|

|

|

|

Preferred stock

|

|

|

|

|

|

|

|

|

|

Shares, beginning and end of period

|

|

|

1,995,185 |

|

|

|

1,995,185 |

|

| |

|

|

|

|

|

|

|

|

|

Preferred stock

|

|

|

|

|

|

|

|

|

|

Balance, beginning and end of period

|

|

$ |

1,995 |

|

|

$ |

1,995 |

|

| |

|

|

|

|

|

|

|

|

|

Series 2

|

|

|

|

|

|

|

|

|

|

Preferred stock

|

|

|

|

|

|

|

|

|

|

Shares, beginning and end of period

|

|

|

- |

|

|

|

- |

|

| |

|

|

|

|

|

|

|

|

|

Preferred stock

|

|

|

|

|

|

|

|

|

|

Balance, beginning and end of period

|

|

$ |

- |

|

|

$ |

- |

|

| |

|

|

|

|

|

|

|

|

|

Common stock

|

|

|

|

|

|

|

|

|

|

Shares, beginning and end of period

|

|

|

825,218,631 |

|

|

|

787,718,631 |

|

| |

|

|

|

|

|

|

|

|

|

Balance, beginning and end of period

|

|

$ |

825,218 |

|

|

$ |

787,718 |

|

| |

|

|

|

|

|

|

|

|

|

Additional paid-in capital

|

|

|

|

|

|

|

|

|

|

Balance, beginning and end of period

|

|

$ |

9,813,090 |

|

|

$ |

9,666,590 |

|

| |

|

|

|

|

|

|

|

|

|

Other comprehensive income (loss)

|

|

|

|

|

|

|

|

|

|

Balance, beginning of period

|

|

$ |

51,427 |

|

|

$ |

93,478 |

|

|

Other comprehensive income (loss)

|

|

|

(14,810 |

)

|

|

|

(35,006 |

)

|

|

Balance, end of period

|

|

$ |

36,617 |

|

|

$ |

58,472 |

|

| |

|

|

|

|

|

|

|

|

|

Accumulated deficit

|

|

|

|

|

|

|

|

|

|

Balance, beginning of period

|

|

$ |

(17,136,394 |

)

|

|

$ |

(16,423,311 |

)

|

|

Net loss

|

|

|

(395,753 |

)

|

|

|

(364,470 |

)

|

|

Balance, end of period

|

|

$ |

(17,532,147 |

)

|

|

$ |

(16,787,981 |

)

|

| |

|

|

|

|

|

|

|

|

|

Total Stockholders' deficit

|

|

$ |

(6,855,227 |

)

|

|

$ |

(6,273,206 |

)

|

See Notes to Unaudited Consolidated Financial Statements.

|

DIGITAL BRAND MEDIA & MARKETING GROUP, INC. AND SUBSIDIARIES

|

|

|

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

|

| |

|

|

|

|

|

|

|

|

| |

|

For the Three months ended

|

|

| |

|

November 30,

|

|

| |

|

2023

|

|

|

2022

|

|

| |

|

(Unaudited)

|

|

|

(Unaudited)

|

|

|

CASH FLOWS FROM OPERATING ACTIVITIES

|

|

|

|

|

|

|

|

|

|

Net loss

|

|

$ |

(395,753 |

)

|

|

$ |

(364,670 |

)

|

| |

|

|

|

|

|

|

|

|

|

Adjustments to reconcile net loss to net cash used in operating activities:

|

|

|

|

|

|

|

|

|

|

Change in fair value of derivative liability

|

|

|

166,504 |

|

|

|

166,320 |

|

| |

|

|

|

|

|

|

|

|

|

Changes in operating assets and liabilities:

|

|

|

|

|

|

|

|

|

|

Accounts receivable

|

|

|

(10,006 |

)

|

|

|

679 |

|

|

Accounts payable and accrued expenses

|

|

|

4,604 |

|

|

|

20,909 |

|

|

Accrued interest

|

|

|

123,534 |

|

|

|

76,810 |

|

|

Accrued compensation

|

|

|

(30,100 |

)

|

|

|

(15,000 |

)

|

| |

|

|

|

|

|

|

|

|

|

NET CASH USED IN OPERATING ACTIVITIES

|

|

|

(141,217 |

)

|

|

|

(114,952 |

)

|

| |

|

|

|

|

|

|

|

|

|

CASH FLOWS FROM INVESTING ACTIVITIES

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

NET CASH USED IN INVESTING ACTIVITIES

|

|

|

- |

|

|

|

- |

|

| |

|

|

|

|

|

|

|

|

|

CASH FLOWS FROM FINANCING ACTIVITIES

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

Proceeds from loans payable

|

|

|

114,400 |

|

|

|

131,876 |

|

|

Principal repayments loan payable

|

|

|

(3,405 |

)

|

|

|

(2,927 |

)

|

|

Officers loans payable

|

|

|

(4,128 |

)

|

|

|

(7,758 |

)

|

| |

|

|

|

|

|

|

|

|

|

NET CASH PROVIDED BY FINANCING ACTIVITIES

|

|

|

106,867 |

|

|

|

121,191 |

|

| |

|

|

|

|

|

|

|

|

|

EFFECT OF VARIATION OF EXCHANGE RATE OF CASH

HELD IN FOREIGN CURRENCY

|

|

|

754 |

|

|

|

39 |

|

| |

|

|

|

|

|

|

|

|

|

NET INCREASE/(DECREASE) IN CASH

|

|

|

(33,596 |

)

|

|

|

6,278 |

|

| |

|

|

|

|

|

|

|

|

|

CASH - BEGINNING OF PERIOD

|

|

|

44,521 |

|

|

|

9,364 |

|

| |

|

|

|

|

|

|

|

|

|

CASH - END OF PERIOD

|

|

|

10,925 |

|

|

|

15,642 |

|

| |

|

|

|

|

|

|

|

|

|

Supplemental disclosures of cash flow information:

|

|

|

|

|

|

|

|

|

|

Cash paid for interest

|

|

$ |

219 |

|

|

$ |

- |

|

|

Cash paid for taxes

|

|

$ |

- |

|

|

$ |

- |

|

See Notes to Unaudited Consolidated Financial Statements.

DIGITAL BRAND MEDIA & MARKETING GROUP, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 – ORGANIZATION, BASIS OF PRESENTATION AND GOING CONCERN

Nature of Business and History of the Company

Digital Brand Media & Marketing Group, Inc. (“The Company” or “DBMM”) is an OTC:PK listed company. The Company was organized under the laws of the State of Florida on September 29, 1998.

The Company strategically focuses on developing the business of its wholly owned and revenue generating online marketing services company, Digital Clarity. With deep DNA in its operating market, blending the services of an experienced professional workforce leveraging a technology offering positions the Company in a strong, forward looking structure. Digital Clarity operates in the growing area of digital marketing that helps companies make the most of the digital economy focusing on areas such as Search Engine Marketing (Google, Yahoo! & Bing), Social Media (Twitter, Facebook & LinkedIn) and Internet Strategy Planning including Design, Analytics and Mobile Marketing.

Following the acquisition of Digital Clarity in 2011 the Company has been honing its business model to be the differentiating service provider in digital marketing space to its clients and prospective business as DBMM grows into one of the leaders in the industry going forward.

Today, DBMM Group crafts, designs and executes digital marketing strategies across multiple ad platforms and social media networks for a broad array of clients to help each of them establish a uniform brand identity across the digital universe. The product offering is a unique value proposition of intelligent analytics provided by an experienced digital marketing and technology team. Therefore, DBMM Group is a blend of data, strategy and creative execution.

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America for interim financial information and with the instructions to Form 10-Q and Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by generally accepted accounting principles for complete financial statements. In the opinion of management, all normal recurring adjustments considered necessary for a fair presentation have been included. Operating results for the three months ended November 30, 2023 are not necessarily indicative of the results that may be expected for the year ending August 31, 2024. For further information refer to the financial statements and footnotes thereto included in the Company’s Form 10-K for the year ended August 31, 2023.

Going Concern

The accompanying condensed consolidated financial statements have been prepared on a going concern basis. The financial statements do not reflect any adjustments that might result if the Company is unable to continue as a going concern.

The Company has outstanding loans and convertible notes payable aggregating $3.2 million at November 30, 2023 and doesn’t have sufficient cash on hand to satisfy such obligations. The preceding raises substantial doubt about the ability of the Company to continue as a going concern. However, the Company generated proceeds of $106,867 from financing activities during the three months ending November 30, 2023. The Company also has a non-binding Commitment Letter from an investor of $250,000 which also includes a right of first refusal on additional capital raise up to $3 million which will contribute to satisfying such obligations and fund any potential cash flow deficiencies from operations for the foreseeable future.

Accordingly, the accompanying consolidated financial statements have been prepared in conformity with U.S. GAAP, which contemplates continuation of the Company as a going concern and the realization of assets and satisfaction of liabilities in the normal course of business. The carrying amounts of assets and liabilities presented in the financial statements do not necessarily purport to represent realizable or settlement values. The financial statements do not include any adjustment that might result from the outcome of this uncertainty.

NOTE 2 – CORRECTION OF AN ERROR

The Company had recognized $49,500 of accrued expenses as a general reserve for legal fees with no identifiable law firm or vendors in fiscal 2011. No law firms or similar vendors have made a claim regarding this accrual or other legal expenses since fiscal 2011, and accordingly, the Company believes that this accrued expense was recorded in error. The error resulted in an overstatement of accounts payable and accrued expenses and accumulated deficit as of November 30, 2022. This error did not impact the Company’s consolidated statement of operations and comprehensive income and consolidated statement of cash flows. The accounts payable and accrued expenses and accumulated deficit in the accompanying consolidated statements of changes in stockholders’ deficit have been restated as of November 30, 2022, respectively, to reflect the correction of the error.

NOTE 3 – SIGNIFICANT ACCOUNTING POLICIES

Basis of Consolidation

The unaudited condensed consolidated financial statements include the accounts of the Company and its wholly owned subsidiary Stylar (DBA Digital Clarity). All significant inter-company transactions are eliminated. The Company has dissolved RTG Ventures (Europe) Limited, a dormant subsidiary during November 2022 and the subsidiary was removed from the United Kingdom Companies House in February 2023.

Cash and Cash Equivalents

Cash and cash equivalents consist primarily of cash in banks. The Company considers cash equivalents to include all highly liquid investments with original maturities of three months or less to be cash equivalents. The Company had no cash equivalents as of November 30, 2023.

Accounts Receivable and Allowance for Doubtful Accounts

Accounts receivable are recorded at the invoiced amount and do not bear interest. Accounts receivable are presented net of allowance for doubtful accounts.

The Company has a policy of reserving uncollectible accounts based on its best estimate of the amount of probable credit losses in its existing accounts receivable. The Company periodically reviews its accounts receivable to determine whether an allowance is necessary based on an analysis of past due accounts and other factors that may indicate that the realization of an account may be in doubt. Account balances deemed to be uncollectible are charged to the bad debt expense after all means of collection have been exhausted and the potential for recovery is considered remote. The Company had no allowance for doubtful accounts as of November 30, 2023.

Property and Equipment

Property and equipment are stated at cost, less accumulated depreciation. Depreciation is provided using the straight-line method over the estimated useful lives of the related assets (primarily three to five years).

Revenue Recognition

Revenue is recognized upon transfer of control of promised or services to customers in an amount that reflects the consideration we expect to receive in exchange for those services. We enter into contracts that can include various combinations of services, which are generally capable of being distinct and accounted for as separate performance obligations. Revenue is recognized net of any taxes collected from customers, which are subsequently remitted to governmental authorities.

Nature of Services

The Company generally provides its services to companies primarily located in Europe but with international exposure. The Company generally provides its services ratably over the terms of the contract and bills such services at a monthly fixed rate. Some of the services are billed quarterly. The Company’s services are sold without guarantees.

Significant Judgments

Our contracts with customers sometimes include promises to transfer multiple services to a customer. Determining whether services are considered distinct performance obligations that should be accounted for separately versus together may require significant judgment.

Judgment is required to determine Standalone Selling Price (SSP) for each distinct performance obligation. The Company uses a single amount to estimate SSP for items that are not sold separately, including set-up services, monthly search advertising services, and monthly optimization and management.

Contract Balances

The timing of revenue recognition may differ from the timing of invoicing to customers. The Company records receivable when revenue is recognized prior to invoicing, or unearned revenue when revenue is recognized subsequent to invoicing.

The allowance for doubtful accounts reflects our best estimate of probable losses inherent in the accounts receivable balance. We determine the allowance based on known troubled accounts, historical experience, and other currently available evidence.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and disclosure of contingent assets and liabilities, at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Included in these estimates are assumptions about the collection of its accounts receivable, converted amount of cash denominated in a foreign currency, and estimated amounts of cash, the derivative liability could settle, if not in common shares. Actual results could differ from those estimates.

Income Taxes

The Company follows the provisions of the ASC 740 -10 related to, Accounting for Uncertain Income Tax Positions. When tax returns are filed, it is highly certain that some positions taken would be sustained upon examination by the taxing authorities, while others are subject to uncertainty about the merits of the position taken or the amount of the position that would be ultimately sustained. In accordance with the guidance of ASC 740-10, the benefit of a tax position is recognized in the financial statements in the period during which, based on all available evidence, management believes it is more likely than not that the position will be sustained upon examination, including the resolution of appeals or litigation processes, if any. Tax positions taken are not offset or aggregated with other positions. Tax positions that meet the more-likely-than-not recognition threshold are measured as the largest amount of tax benefit that is more than 50 percent likely of being realized upon settlement with the applicable taxing authority. The portion of the benefits associated with tax positions taken that exceeds the amount measured as described above should be reflected as a liability for uncertain tax benefits in the accompanying balance sheet along with any associated interest and penalties that would be payable to the taxing authorities upon examination. The Company believes its tax positions are all highly certain of being upheld upon examination. As such, the Company has not recorded a liability for uncertain tax benefits.

The Company has adopted ASC 740-10-25 Definition of Settlement, which provides guidance on how an entity should determine whether a tax position is effectively settled for the purpose of recognizing previously unrecognized tax benefits and provides that a tax position can be effectively settled upon the completion of an examination by a taxing authority without being legally extinguished. For tax positions considered effectively settled, an entity would recognize the full amount of tax benefit, even if the tax position is not considered more likely than not to be sustained based solely on the basis of its technical merits and the statute of limitations remains open.

Earnings (loss) per common share

The Company utilizes the guidance per FASB Codification “ASC 260 "Earnings Per Share". Basic earnings per share is calculated on the weighted effect of all common shares issued and outstanding and is calculated by dividing net income available to common stockholders by the weighted average shares outstanding during the period. Diluted earnings per share, which is calculated by dividing net income available to common stockholders by the weighted average number of common shares used in the basic earnings per share calculation, plus the number of common shares that would be issued assuming conversion of all potentially dilutive securities outstanding, is not presented separately as it is anti- dilutive. Such securities have been excluded from the per share computations for the three months period ended November 30, 2023 and the three and nine-month periods ended November 30, 2022. During the three-month period ended November 30, 2023, the dilutive securities amounted to 172,889,284 shares of common stock and related to convertible notes.

Derivative Liabilities

The Company assessed the classification of its derivative financial instruments as of November 30, 2023, which consist of convertible instruments and rights to shares of the Company’s common stock and determined that such derivatives meet the criteria for liability classification under ASC 815.

ASC 815 generally provides three criteria that, if met, require companies to bifurcate conversion options from their host instruments and account for them as free standing derivative financial instruments. These three criteria include circumstances in which (a) the economic characteristics and risks of the embedded derivative instrument are not clearly and closely related to the economic characteristics and risks of the host contract, (b) the hybrid instrument that embodies both the embedded derivative instrument and the host contract is not re-measured at fair value under otherwise applicable generally accepted accounting principles with changes in fair value reported in earnings as they occur and (c) a separate instrument with the same terms as the embedded derivative instrument would be considered a derivative instrument subject to the requirements of ASC 815. ASC 815 also provides an exception to this rule when the host instrument is deemed to be conventional, as described.

During the three-month period ended November 30, 2023 and 2022, the Company had notes payable outstanding in which the conversion rate was variable and undeterminable. Accordingly, the Company has recognized a derivative liability in connection with such instruments. The Company uses judgment in determining the fair value of derivative liabilities at the date of issuance at every balance sheet thereafter and in determining which valuation is most appropriate for the instrument (e.g., Binomial method), the expected volatility, the implied risk-free interest rate, as well as the expected dividend rate.

Fair Value of Financial Instruments

Effective January 1, 2008, the Company adopted FASB ASC 820-Fair Value Measurements and Disclosures, or ASC 820, for assets and liabilities measured at fair value on a recurring basis. ASC 820 establishes a common definition for fair value to be applied to existing generally accepted accounting principles that require the use of fair value measurements establishes a framework for measuring fair value and expands disclosure about such fair value measurements. The adoption of ASC 820 did not have an impact on the Company’s financial position or operating results but did expand certain disclosures.

ASC 820 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Additionally, ASC 820 requires the use of valuation techniques that maximize the use of observable inputs and minimize the use of unobservable inputs. These inputs are prioritized below.

|

Level 1

|

Observable inputs such as quoted market prices in active markets for identical assets or liabilities.

|

|

Level 2

|

Observable market-based inputs or unobservable inputs that are corroborated by market data.

|

|

Level 3

|

Unobservable inputs for which there is little or no market data, which require the use of the reporting entity’s own assumptions.

|

The Company did not have any Level 2 or Level 3 assets or liabilities as of November 30, 2023, except for its derivative liabilities which are valued based on Level 3 inputs.

Cash is highly liquid and easily tradable as of November 30, 2023 and therefore classified as Level 1 within our fair value hierarchy.

In addition, FASB ASC 825-10-25 Fair Value Option, or ASC 825-10-25, was effective January 1, 2008. ASC 825-10-25 expands opportunities to use fair value measurements in financial reporting and permits entities to choose to measure many financial instruments and certain other items at fair value. The Company did not elect the fair value options for any of its qualifying financial instruments.

Convertible Instruments

The Company evaluates and accounts for conversion options embedded in its convertible instruments in accordance with professional standards for “Accounting for Derivative Instruments and Hedging Activities”.

Professional standards generally provide three criteria that, if met, require companies to bifurcate conversion options from their host instruments and account for them as free standing derivative financial instruments. These three criteria include circumstances in which (a) the economic characteristics and risks of the embedded derivative instrument are not clearly and closely related to the economic characteristics and risks of the host contract, (b) the hybrid instrument that embodies both the embedded derivative instrument and the host contract is not re-measured at fair value under otherwise applicable generally accepted accounting principles with changes in fair value reported in earnings as they occur and (c) a separate instrument with the same terms as the embedded derivative instrument would be considered a derivative instrument. Professional standards also provide an exception to this rule when the host instrument is deemed to be conventional as defined under professional standards as “The Meaning of “Conventional Convertible Debt Instrument”.

The Company accounts for convertible instruments (when it has determined that the embedded conversion options should not be bifurcated from their host instruments) in accordance with professional standards when “Accounting for Convertible Securities with Beneficial Conversion Features,” as those professional standards pertain to “Certain Convertible Instruments.” Accordingly, the Company records, when necessary, discounts to convertible notes for the intrinsic value of conversion options embedded in debt instruments based upon the differences between the fair value of the underlying common stock at the commitment date of the note transaction and the effective conversion price embedded in the note. Debt discounts under these arrangements are amortized over the term of the related debt to their earliest date of redemption. The Company also records when necessary deemed dividends for the intrinsic value of conversion options embedded in preferred shares based upon the differences between the fair value of the underlying common stock at the commitment date of the note transaction and the effective conversion price embedded in the note.

ASC 815-40 provides that, among other things, generally, if an event is not within the entity’s control or require net cash settlement, then the contract shall be classified as an asset or a liability.

Stock Based Compensation

We account for the grant of stock options and restricted stock awards in accordance with ASC 718, “Compensation-Stock Compensation.” ASC 718 requires companies to recognize in the statement of operations the grant-date fair value of stock options and other equity-based compensation.

Foreign Currency Translation

Assets and liabilities of subsidiaries operating in foreign countries are translated into U.S. dollars using either the exchange rate in effect at the balance sheet date or historical rate, as applicable. Results of operations are translated using the average exchange rates prevailing throughout the year. The effects of exchange rate fluctuations on translating foreign currency assets and liabilities into U.S. dollars are included in a separate component of stockholders’ equity (accumulated other comprehensive loss), while gains and losses resulting from foreign currency transactions are included in operations.

Concentration of Risks

The Company’s accounts and receivable as of November 30, 2023 and August 31, 2023 and revenues for the three-month period ended November 30, 2023 and 2022 are primarily from five customers.

Recently Issued Accounting Pronouncements

Management does not believe that any other recently issued, but not yet effective, accounting standards if currently adopted would have a material effect on the accompanying condensed consolidated financial statements.

NOTE 4 – LOANS PAYABLE

| |

|

November 30,

2023

|

|

|

August 31,

2023

|

|

|

Loans payable

|

|

$ |

2,647,013 |

|

|

$ |

2,505,588 |

|

The loans payables are generally due on demand and have not been called, are unsecured, and are bearing interest at a range of 0-12%., with the exception of one loan payable to a financial institution. Such loan, which amounted to $38,531 at November 30, 2023 bears interest rate at 2.5%, is unsecured, matures in November 2027 with principal and interest payable monthly. This loan is part of a Bounce Back Loan Scheme from the UK Government.

The company may have to provide alternative consideration (which may be in cash, fixed number of shares or other financial instruments) up to amounts accrued to satisfy its fixed obligations under certain unsecured loans payable. The consideration hasn’t been issued yet and is included in accrued expenses and interest expense and was valued based on the fair value of the consideration at issuance.

The aggregate schedule maturities of the Company’s loans payable outstanding as of November 30, 2023 are as follows:

|

2024

|

|

$ |

2,619,716 |

|

|

2025

|

|

|

11,948 |

|

|

2026

|

|

|

12,708 |

|

|

2027

|

|

|

2,641 |

|

| |

|

|

|

|

| |

|

$ |

2,647,013 |

|

NOTE 5 – CONVERTIBLE DEBENTURES

The Company’s convertible debentures consisted of the following:

| |

|

November 30,

2023

|

|

|

August 31,

2023

|

|

|

Convertible notes payable

|

|

$ |

517,242 |

|

|

$ |

517,542 |

|

|

Unamortized debt discount

|

|

|

- |

|

|

|

- |

|

|

Total

|

|

$ |

517,242 |

|

|

$ |

517,542 |

|

The convertible debentures matured in 2015, and bear interest at ranges between 6% and 15%. The convertible debentures are convertible at ratios varying between 45% and 50% of the closing price at the date of conversion through, at its most favorable terms for the holders, the average of the three lowest closing bids for a period of 5-30 days prior to conversion.

No convertible debentures have been issued since 2015 and none executed since 2016. Certain settlements with holders of convertible debentures have been agreed since 2018 to the benefit to the Company.

NOTE 6 – OFFICERS LOANS PAYABLE

| |

|

November 30,

2023

|

|

|

August 31,

2023

|

|

|

Officers loans payable

|

|

$ |

49,765 |

|

|

$ |

53,893 |

|

The loans payables are due on demand, are unsecured, and are non-interest bearing.

NOTE 7 – DERIVATIVE LIABILITIES

The Company accounts for the embedded conversion features included in its convertible instruments as derivative liabilities. At each measurement date, the fair value of the embedded conversion features was based on the lattice binomial method using the following assumptions:

| |

|

November 30,

2023

|

|

|

August 31,

2023

|

|

|

Effective Exercise price

|

|

|

0.0022-0.00352 |

|

|

|

0.0045 |

|

|

Effective Market price

|

|

|

0.0044 |

|

|

|

0.009 |

|

|

Volatility

|

|

|

31.02 |

% |

|

|

40.55 |

% |

|

Risk-free interest

|

|

|

5.16 |

% |

|

|

5.18 |

% |

|

Terms

|

|

|

365 days |

|

|

|

365 days |

|

|

Expected dividend rate

|

|

|

0 |

% |

|

|

0 |

% |

Changes in the derivative liabilities during the nine-month period ended November 30, 2023 is as follows:

|

Balance at August 31, 2023

|

|

$ |

206,476 |

|

|

Changes in fair value of derivative liabilities

|

|

|

166,504 |

|

|

Balance, November 30, 2023

|

|

$ |

372,980 |

|

NOTE 8 – ACCRUED COMPENSATION

As of November 30, 2023, and August 31, 2023, the Company owes $1,283,436 and $1,313,536, respectively, in accrued compensation and expenses to certain directors and consultants. The amounts are non-interest bearing.

NOTE 9 – COMMON STOCK AND PREFERRED STOCK

Preferred Stock- Series 1 and 2

The designation of the Preferred Stock- Series 1 is as follows: Authorized 2,000,000 shares, par value of $0.001. One share of the Company’s Preferred Stock- Series is convertible into 53.04 shares of the Company’s common stock, at the holder’s option and with the Company’s acquiescence, and has three votes per share.

The designation of the Preferred Stock- Series 2 is as follows: Authorized 2,000,000 shares, par value of $0.001. One share of the Company’s Preferred Stock- Series is convertible into one share of the Company’s common stock, at the holder’s option and with the Company’s acquiescence, and has no voting rights.

Common Stock

The Authorized Shares were increased to 2,000,000,000 in April 4, 2016.

NOTE 10 – COMMITMENTS AND CONTINGENCIES

Leases

The Company leases its facilities under non-cancellable operating leases which are renewable monthly. The leases have monthly base rents. The latest monthly base rent for the Company’s facilities ranges between $285 and $800.

Rental expense amounted to $3,106 and $2,058 during the three-month period ended November 30, 2023 and 2022, respectively.

Consulting Agreement

The annual compensation of Linda Perry amounts to $150,000 for her role as a consultant and as Executive Director for US interface to provide oversight regarding external regulatory reporting requirements. In addition, Ms. Perry is the lead executive for capital funding requirements and business development. The agreement has a rolling three-year term through September 2025.

Legal Proceedings

From time to time, the Company has become or may become involved in certain lawsuits and legal proceedings which arise in the ordinary course of business. The Company intends to vigorously defend its positions. However, litigation is subject to inherent uncertainties and an adverse result in those or other matters may arise from time to time that may harm its financial position, or our business and the outcome of these matters cannot be ultimately predicted.

NOTE 11 – FOREIGN OPERATIONS

As of November 30, 2023, a majority of our revenues and assets are associated with subsidiaries located in the United Kingdom. Assets at November 30, 2023 and revenues for the nine-month period ended November 30, 2023 were as follows (unaudited)

| |

|

United States

|

|

|

Great Britain

|

|

|

Total

|

|

|

Revenues

|

|

$ |

30,000 |

|

|

$ |

55,550 |

|

|

$ |

85,550 |

|

|

Total revenues

|

|

$ |

30,000 |

|

|

$ |

55,550 |

|

|

$ |

85,550 |

|

|

Identifiable assets at November 30, 2023

|

|

$ |

12,221 |

|

|

$ |

30,760 |

|

|

$ |

42,981 |

|

As of November 30, 2022, most of our revenues and assets are associated with subsidiaries located in the United Kingdom. Assets at November 30, 2022 and revenues for the nine-month period ended November 30, 2022 were as follows (unaudited)

| |

|

United States

|

|

|

Great Britain

|

|

|

Total

|

|

|

Revenues

|

|

$ |

- |

|

|

$ |

54,531 |

|

|

$ |

54,531 |

|

|

Total revenues

|

|

$ |

- |

|

|

$ |

54,531 |

|

|

$ |

54,531 |

|

|

Identifiable assets at November 30, 2022

|

|

$ |

14,057 |

|

|

$ |

23,864 |

|

|

$ |

37,921 |

|

NOTE 12 – SUBSEQUENT EVENTS

The Company has analyzed its operations after November 30, 2023 through the date these financial statements were issued and has determined that it does not have any material subsequent events to disclose.

.

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Readers are cautioned that certain statements contained herein are forward-looking statements and should be read in conjunction with our disclosures under the heading “Forward-Looking Statements” above. These statements are based on current expectations and assumptions that are subject to risks and uncertainties. This discussion also should be read in conjunction with the notes to our consolidated financial statements contained in Item 8. "Financial Statements and Supplementary Data" of this Report.

OPERATIONS OVERVIEW/OUTLOOK

The Company developed a document called the Creds Deck which provides a description to prospective clients of Digital Clarity’s value proposition http://www.dbmmgroup.com/wp-content/uploads/2023/07/DBMM_Creds_Deck_2023.pdf

The fourth quarter of fiscal 2023 has focused on a measured return to normalcy as businesses have faced enormous challenges over the past few years, and DBMM's operating business Digital Clarity, is no exception. However, for context, it is worth reminding investors and shareholders, that Digital Clarity was acquired by DBMM as a cash-flow positive business with a great reputation and industry network, winning industry awards.

As stated in the MD&A's for many years since the acquisition of Digital Clarity, the operating business has always been cash flow positive, but the costs of maintaining a public company far exceed the gross profit in the audited financial statements. That was expected, following the digital business model, though many digital companies do not have any operating revenues while they build the business. The business is developed to a 'to be determined level' (TBD), with all capital infusion and revenues (if any) remaining in the growth model.

As the economy recovers, and the Company's mitigating circumstances have all been positively concluded, there is also an opportunity for their clients, both new and prospective, to gain a competitive advantage in the post-pandemic commercial environment. The transformation of a company guided by Digital Clarity as its digital architect, demands a "seat at the table" of decision makers as the subject matter expert in the new digital landscape. Digital Clarity has earned that role. The industry as seen today and in the future is described below:

2023 REALITIES TEMPER 2024 BUDGETS AND OUTLOOK

One year ago, leaders were facing global unrest, supply chain instability, soaring inflation, the long shadow of the pandemic, and a projected economic slowdown. Yet most had overly optimistic expectations heading into budget season, with every function expecting to lock in modest budget increases for 2023.

Many of last year’s concerns didn’t materialize, and the outlook for the global economy in 2024 appears brighter as supply chain disruptions ease and inflation edges back toward targets. That said, businesses will have to deal with the after-effects of not only the global pandemic but new challenges. The backdrop as we enter 2024, it is clear that B2B leaders have concerns about inflation and higher interest rates, as they plan for 2024.

Though the general business sentiment is cautious, Digital Clarity has adapted its model to continually focus on areas that will allow the business to thrive as we come out of the challenging economic backdrop.

Digital Clarity has been pivoting during these challenging headwinds and working to build upon its experience in the B2B space and engaging with prospects in the SaaS and Tech market.

Discretionary marketing budgets, sales headcount, and software costs will continue to be scrutinized closely in 2024, though the demand for maximum performance continues, even though inflation abates particularly in the US. This will only accelerate revenue-focused marketing leadership and reduce the money invested in non-hyper-targeted channels.

Expansion will become the new-new business, making the line between revenue marketing and demand generation very thin. More of an emphasis will be on preserving revenue through retention and expansion efforts over acquiring net new customers, this is an area where Digital Clarity excels.

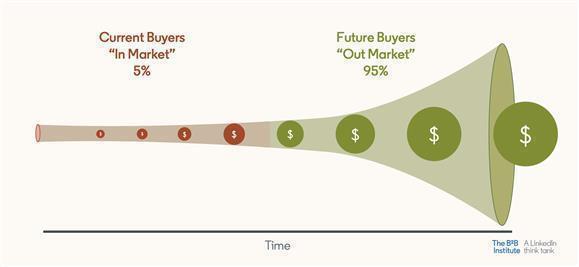

This will also push leaders to critically evaluate the way in which they acquire customers, including increasing their focus on the technology that helps them prioritize the right accounts. B2B companies beware, It may feel like you have fewer “in-market” accounts than in prior years, so the risk of wasting resources on accounts that won’t buy is much higher. To avoid this, double down on the ‘95-5’ rule, there will be a shift. to get in front of the 5% of in-market accounts that are ready to buy now. If not, it's inevitable that your competitors will target them first.

WHY B2B IS THE RIGHT PLACE AT THE RIGHT TIME

Just before and during the pandemic, DBMM’s operating business, Digital Clarity analyzed market data and found that there was a large market segment that was very badly served by the digital marketing sector and in particular lacked a level planning, strategy and general, good advice when it came to sales growth and brand positioning. This was the Business to Business (B2B) sector. In particular, the technology, software and software services sector (SaaS). This pivot was the model for Digital Clarity’s return to a level of normal trading against a continued volatile economic backdrop.

B2B is undergoing a renaissance as business models, innovation drivers, and buyers evolve dramatically from decades prior. Now some of the most profitable companies across the globe are B2B companies.

As perceptions of the U.S. economy decline, concerns over inflation persist. More than half of small business owners continue to cite it as their top concern. However, B2B leaders are hopeful about the future, even in these uncertain times.

While many in the business community cite serious concerns over global economic uncertainty, B2B leaders are largely optimistic about the outlook for their organizations and the role of marketing in helping them grow.

The B2B Marketing Benchmark uncovers the trends and practices fueling this optimism: Marketing budgets are on the rise worldwide; Excitement among B2B leaders about emerging technologies like Generative AI, with growth in the adoption of creative and technical skills that will help marketers meet the demands of these emerging technologies and trends.

Digital Clarity is well poised to enable B2B leaders to thrive in a rapidly changing environment and how to plan for the long term.

THE B2B BUYER JOURNEY IS COMPLEX. THIS IS WHY EXPERTS LIKE DIGITAL CLARITY NEED TO BE INVOLVED FROM THE START.

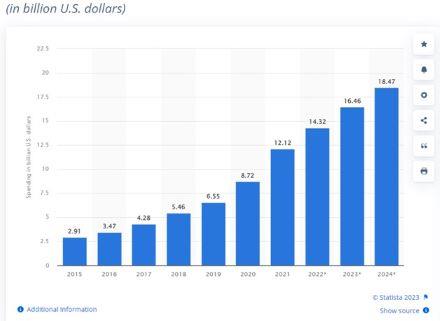

Savvy communication experts like Digital Clarity produce ideas that shape perceptions and grow markets. There has never been a better time to navigate into the B2B Marketplace as demand for an experienced, safe pair of hands is required. This sector is growing rapidly and the demand for expertise and skill to help businesses in marketing their services and products is sought after. B2B digital ad spending is projected to reach $18.47 billion by 2024, it will account for nearly 50% of total B2B ad spending that year according to Insider Intelligence.

For a long time, tried and tested B2B marketing strategies have been based around a linear model, where activities aim to gather prospects at one end of a pipeline (or funnel) and gently nudge and nurture until they leave as newly won customers at the other end.

It’s been this way for quite a while giving rise to language that any B2B marketer is familiar with such as “MQLs” (marketing qualified leads) and “SQLs” (sales qualified leads), shaping how B2B marketing and sales should work together (where one hands the baton on to the other in the form of a well nurtured, warm lead) and KPIs that evaluate this linear performance (pipeline velocity, #MQLs and #SQLs, to name just three).

So established is the thinking that the world’s biggest CRM platforms are structured around this linear model of how B2B buying takes place.

DEVELOPING A STRONGER US FOOTPRINT FOR DIGITAL CLARITY IN 2024-2025

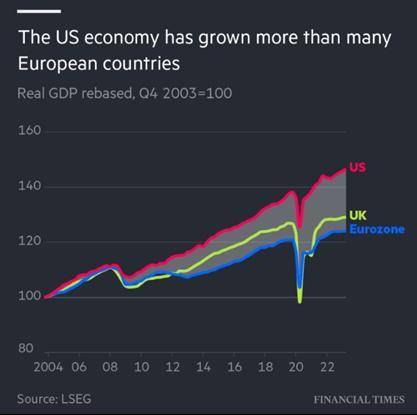

The IMF last week became the latest economics organization to declare that the US economy would power ahead, forecasting an expansion of 1.5 percent next year. This compares with IMF forecasts of 1.2 percent for the eurozone and 0.6 percent for the UK.

A critical structural factor behind the US-European divergence is the difference in the industrial composition of the economies.

2023 saw Digital Clarity have a stronger demand by prospective customers in the burgeoning B2B Tech sector and with this laser focus in the tech marketing market, Digital Clarity is well positioned to take advantage of applying its successful methodology into the largest economy in the world.

The US has a booming tech sector, with successful and innovative companies such as Amazon, Alphabet, and Microsoft that have no European equivalents in Europe. With the US dominating artificial intelligence, that gap is likely to widen, economists warn.

By contrast, Europe specializes in industries that are increasingly facing the threat of Chinese competition, such as electric vehicles.

With stronger investment and better demographics, the gap between the US and Europe is likely to widen further in the coming years.

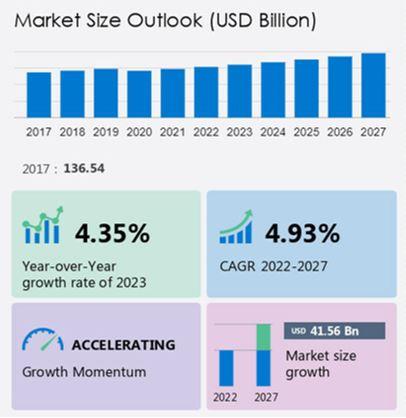

DEMAND FOR MARKETING CONSULTING IN NORTH AMERICA IS PREDICTED TO GROW BY 36%

The marketing consulting services segment is forecast to increase by USD 41.56 billion between now and 2027 with North America estimated to contribute 36% to the growth. Data from research company Technavio’s analysts have elaborately explained the regional trends, drivers, and challenges that are expected to shape the market during the forecast period. With the development of new research companies and the availability of various databases and business analytics tools, this North American region is a major contributor to the global marketing consulting market. This allows businesses to collect meaningful, useful data at a fraction of the cost that marketing consultants pay.

Additionally, the ease of scaling virtualization and automating administrative tasks dynamically will increase SaaS adoption. Due to digitalization, various businesses and organizations in this region are adopting SaaS solutions, which help improve a range of operations such as business planning, order fulfilment, and customer service. Hence, such factors are expected to drive market growth in this region during the forecast period.

B2B BRAND INVESTMENT IS THE BIG FOCUS FOR 2024 AND BEYOND

THE SHIFT TO DIGITAL IS PERMANENT

Digital will continue to command a greater overall share as more B2B marketers make the permanent shift from traditional advertising to online activities.

One of the most pronounced effects the pandemic had on B2B marketing was exponentially accelerating its transition into digital. As the business world recovers from the pandemic and returned to more traditional models, this transition has slowed down. The past year has affirmed, however, that it will not stop.

By 2025, Gartner expects 80% of B2B sales interactions between suppliers and buyers to occur in digital channels.

B2B buying behaviors have been shifting toward a buyer-centric digital model, a change that has been accelerated the past couple of years.

Digital Clarity sits at the intersection of marketing, analysis and sales growth for B2B Tech companies. Focus on digital-lead generation and qualification. The pandemic lockdown underscored how important it is to source and qualify new leads beyond the relationships you already have. It also accelerated digital-lead generation toward high-value customer segments. Traditional lead generation tactics like cold calling are being replaced or supplemented by lower-touch digital leads focused on meeting customers “where they are.” Sales should work closely with Marketing to source leads from typical digital sources (such as Google and LinkedIn), as well as from relevant third-party affiliates (such as LendingTree for mortgages, Trivago for travel, and Buyerzone for B2B services) that are becoming initial destinations for shoppers. Leaders in digital-lead generation can cost-effectively source and qualify leads as well as automate the lead-generation process to support their sales teams with higher propensity leads.

This can energize a sales force. For example, a private-equity owned B2B company was recently challenged with high turnover of entry-level salespeople who lost energy after months of cold calling. Focusing on a digital lead-generation strategy helped them to source more qualified leads with a higher propensity to purchase. This was a huge boost for newer salespeople and helped to supplement their other lead-generation activities, positioning them for greater sales success and reduced salesperson churn.

SALES ARE GOING DIGITAL

Gartner Says 80% of B2B Sales Interactions Between Suppliers and Buyers Will Occur in Digital Channels by 2025.

Over the next five years, an even greater rise in digital interactions between buyers and suppliers will break traditional sales models.

The Gartner Future of Sales 2025 report predicts that by 2025, 80% of B2B sales interactions between suppliers and buyers will occur in digital channels. Chief sales officers (CSOs) and other senior sales leaders must accept that buying preferences have permanently changed and, as a result, so too will the role of sellers.

Sales organizations must be able to sell to customers everywhere the customer expects to engage, interact and transact with suppliers. Gartner defines the future of sales as the permanent transformation of organizations’ sales strategies, processes and allocation of resources, moving from a seller-centric to a buyer-centric orientation and shifting from analogy sales processes to digital-first engagement with customers.

Disruptive buyer dynamics are rewriting the rulebook for B2B sales, demanding digital-first engagement with customers. The rise in digital sales will be driven by marketing that creates demand and trust in brands.

This doesn’t portend the eventual “death of the sales rep,” but it does signal drastic changes needed in the seller role. Sales leaders must deliver significant value through digital and omnichannel sales models, aided by sales professionals who can steer self-learning customers toward more confident decisions. Digital delivers this.

THE GROWTH OF THE DIGITAL OMNICHANNEL

Gartner research shows a steady shift of customer preferences from in-person sales interactions to digital channels. B2B buyers spend only 17% of the total purchase journey with sales reps.

Because the average deal involves multiple suppliers, a sales rep gets roughly 5% of a customer’s total purchase time. And 44% of millennials prefer no sales rep interaction at all in a B2B setting.

Sales leaders must deliver significant value through digital and omnichannel sales models, aided by sales professionals who can steer self-learning customers toward more confident decisions.

THE OMNICHANNELREMAINS KEY IN B2B BUYING

Digital Clarity can help organizations adopt the B2B Omnichannel. Eight in ten B2B leaders say that omnichannel is as or more effective than traditional methods, a sentiment that has grown sharply in the last 2 years. Even as in-person engagement re-emerged as an option, buyers made clear they prefer a cross-channel mix, choosing in-person, remote, and digital self-serve interactions in equal measure.

B2B e-commerce has taken the lead as the most effective sales channel. It is rated first by 35 percent of respondents, ahead of in-person sales (26 percent), video conference (12 percent), email (10 percent), and telephone (8 percent) according to a recent report from McKinsey. Companies winning market share have not only digital self-serve channels such as their own websites but also broader e-commerce offerings. For example, 48 percent of winners are on industry-specific marketplaces, compared with only 13 percent of companies losing share.

Digital Clarity helps companies deploy hybrid marketing models, both online and offline, that then feed into sales teams. Hybrid sales models, which are comprised of roles with a mix of both in-person and remote time with customers, are deployed by 57 percent of market-leading companies.

Customers are increasingly willing to spend big on e-commerce transactions. Many B2B companies shun e-commerce over concern about channel conflict: 38 percent of respondents said it was the biggest reason they avoided selling online. However, the sales growth opportunity may now outweigh related potential costs. Similar to last year, about 70 percent of decision-makers are prepared to spend up to $500,000 on a single e-commerce transaction. At the highest end of the spectrum, however, we see meaningful movement: the number of decision-makers willing to spend as much as $10 million or more has increased by 83 percent. This trend holds true particularly in China, India, and the United States, and in global energy and materials (GEM); telecommunications, media, and technology (TMT); and advanced industries sectors.

McKinsey says that the equilibrium is no accident. As B2B buyers flexed to remote and digital ways of engaging, they found much to like. The use and preference for e-commerce—self-serve, for example—has continually grown year on year.

Omnichannel is more effective than traditional sales models alone. As more companies enable face-to-face, remote, and e-commerce interactions, satisfaction with the sales model has grown exponentially. More than 90 percent of B2B companies say their go-to-market model is just as or more effective than before the pandemic began.

Taking an omnichannel approach means strategy and ROI are built in from the start too, so as an approach, it helps measure what works - allowing accurate attribution of results and enabling marketers to move the budget from what doesn’t work to doing more of what does. According to the recent DMA Response Rate Report, 65% of marketers use two or more media channels in their marketing campaigns while 44% of marketers use three or more.

There might be data, software, automation, and analytics considerations but B2B marketing is chiefly about ROI and about creating a large top-of funnel that can be nurtured through to sales conversion. Omni-channel is also inherent in the design. Campaigns that are planned for all relevant channels are not an afterthought.

DIGITAL CLARITY PERFECTLY POSITIONED FOR GROWTH

Organizations will have to fight hard to retain loyalty if customer needs are not met: for example, eight in ten B2B decision makers say they will actively look for a new supplier if performance guarantees.

Buyers are more willing than ever before to spend big through remote or online sales channels, with 35 percent willing to spend $500,000 or more in a single transaction. Seventy-seven percent of B2B customers are also willing to spend $50,000 or more.

B2B customers now regularly use ten or more channels to interact with suppliers.

Digital Clarity is a specialist in many of these channels and has been for a number of years. This expertise, experience, and trust will put Digital Clarity front of mind for organizations as they seek professional consultancy.

THE B2B MILLENIAL BUYER IS CHANGING THE LANDSCAPE

Millennials and Gen Z, or those born between 1996 and 2012, constitute 64% of business buyers.

Younger buyers are more demanding, engaging in more buying activities, and more willing to express their dissatisfaction with the buying process.

Nearly half of millennial buyers prefer no engagement with a salesperson at all, with the average being a third. In 2025, digital channels will account for four-fifths of all B2B sales engagements. Ultimately, the breakdown of the traditional sales model is driven by the digital shift in industrial buying, dramatically speeded up by the social distancing of vendors and clients.

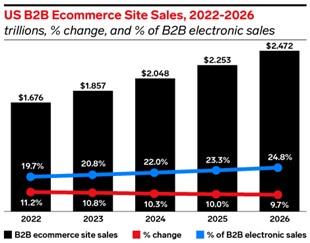

This is where Digital Clarity comes in. Part of the consulting strategy is to help B2B product sales by reshaping marketing strategies to focus on the millennial B2B e-commerce sector. Between 2024 - 2026, over $2 trillion in B2B product sales will be taking place over ecommerce websites. However, this will still represent only a small portion of overall US B2B product sales and just over a fifth of B2B electronic sales.

Millennial refers to people born between 1981 and 1996. Gen Z refers to those born between 1996 and 2012. According to a recent report from Forrester Research Inc. Millennial and Gen Z B2B buyers are now the chief purchasers of goods and services for their organization. And when it comes to ecommerce, the growing number of millennial and Gen Z professionals have very high expectations for B2B ecommerce,

Millennial and Gen Z B2B buyers also have high standards for engaging and purchasing online from sellers. Younger buyers carry new demands and expectations for B2B buying. Forrester predicts that in two years, more than a third of millennial and Gen Z business buyers will purchase through self-guided digital channels. Those include vendor websites, marketplaces, app stores, or directly from an existing product.

Furthermore, Millennials and Gen Z B2B buyers are active information seekers. Younger buyers go to more sources and find third-party resources more impactful than vendor resources. This group is quicker to express dissatisfaction with the buying experience. 90% of younger buyers cite dissatisfaction with their vendor in at least one area compared to 71% of older buyers. Digital is permanent and its market share growing. That is the future.

CONTENT MARKETING

Content has become a critical tool in the marketing mix for almost every B2B brand. Nine out of ten B2B marketers are using content marketing strategies to pull in new customers. This year, the most successful marketers were already spending 40% or more of their budget on their content strategy.

At its simplest, B2B content marketing is when a brand uses stories, ideas, and insights to engage and influence a business audience.

There is a realization amongst B2B brands that rather than being faceless organizations, they need to tell their brand’s story and show a more human side to their business, endear and promote demand from other businesses and customers. The best content marketing campaigns back up these stories and ideas with robust insights: interesting data points, original research, and real-world examples that help their customers understand a new trend or challenge and equip them with the tools and best practices to respond and thrive.

These data points and research is utilized by Digital Clarity to support companies in shaping their content strategy. Typically, areas that Digital Clarity help clients are:

|

|

●

|

Blog posts – marketers who make blogging a priority are 13x more likely to see a positive ROI for their efforts.

|

|

|

|

|

|

|

●

|

White papers – favored by 22% of business leaders, these longer research-based reports provide more in-depth information. Learn more about writing a compelling B2B marketing white paper here.

|

|

|

|

|

|

|

●

|

Short-form articles – enjoyed by 37% of execs, these have to research-based if they are to stand out.

|

|

|

|

|

|

|

●

|

Case studies – these provide buyers with reassurance further down the buying funnel and can be made sector-specific. Nearly half of all business leaders appreciate them.

|

|

|

|

|

|

|

●

|

Infographics – these have become one of the most popular content marketing tools in recent years.

|

|

|

|

|

|

|

●

|

Podcasts – increasingly popular lead generation tools with marketers looking to deliver thought leadership content to buyers on the move.

|

|

|

|

|

|

|

●

|

Videos – companies using video, experience clickthrough rates that are 27% higher and web conversion rates 34% greater than those that don’t.

|

|

|

|

|

|

|

●

|

Email – nearly eight out of 10 marketers report see g an increase in email engagement over the past 12 months of 2022.

|

|

|

|

|

|

|

●

|

LinkedIn – generates more than 50% of all social traffic to B2B websites & blogs.

|

CONTENT IS INFORMATION, AND DISCOVERABLE INFORMATION DRIVES REVENUE

Information drives purchase ease and high-quality sales

All of this looping around and bouncing from one job to another means that buyers value suppliers that make it easier for them to navigate the purchase process.

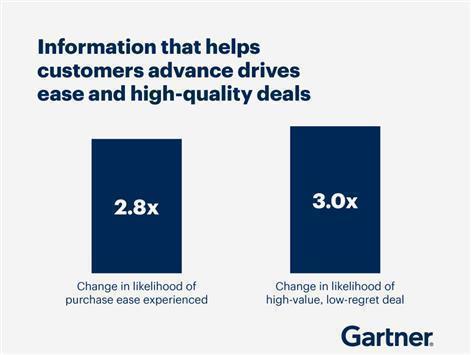

In fact, Gartner research found that customers who perceived the information they received from suppliers to be helpful in advancing across their buying jobs were 2.8 times more likely to experience a high degree of purchase ease, and three times more likely to buy a bigger deal with less regret.

Digital Clarity’s model shapes their client’s content to provide more discoverable, differentiating information, and this increases revenues. This process is one of Digital Clarity’s competitive advantages.

Buyer enablement, or the provisioning of information to customers in a way that enables them to complete information online, like gathering information or making a purchase, is an area that Digital Clarity are helping organizations.

KEY MILESTONES

As the market conditions in the consumer market are increasing in the US, the team at Digital Clarity pivoted their business model to address the need in the B2B business sector. This is a more strategic offering for prospective customers.

Digital Clarity has started offering a wider array of services to its fast-growing S company in the US. Services include, LinkedIn strategy, content positioning and SEO.

Digital Clarity has attended a major convergence summit with its client in the Unified Communication and Digital Transformation arena. This allowed the team to meet with the likes of SaaS CX providers, 8x8, Five9, and Mitel, amongst others. This will be an area of focus for the company into 2023.

In October, Digital Clarity was part of a select group that part of a panel that discussed the impact of NFTs, Blockchain and the growth of Web 3 and the Metaverse. The event was arranged by leading law firm Memery Crystal, part of Rosenblatt.

Digital Clarity has been on a large business development path and attended various networking events in London. The events include Enterprise Cyber Security hosted at the London Stock Exchange as well as diverse events in DeFi and InsureTech.