Form FWP - Filing under Securities Act Rules 163/433 of free writing prospectuses

08 März 2024 - 9:26PM

Edgar (US Regulatory)

Free Writing Prospectus pursuant to Rule 433 dated March 8, 2024

Registration Statement No. 333-269296

|

|

|

Autocallable ETF-Linked Notes due |

OVERVIEW |

The notes do not bear interest. The notes will mature on the stated maturity date unless they are automatically called on any call observation date commencing on September 23, 2024. Your notes will be automatically called on a call observation date if the closing level of each of the Energy Select Sector SPDR® Fund and the Utilities Select Sector SPDR® Fund on such date is greater than or equal to its applicable call level, resulting in a payment on the corresponding call payment date for each $1,000 face amount of your notes equal to such $1,000 face amount plus the product of $1,000 times the applicable call premium amount.

The return on your notes is linked to the performances of the Energy Select Sector SPDR® Fund and the Utilities Select Sector SPDR® Fund, and not to that of the Energy Select Sector Index or the Utilities Select Sector Index on which the respective ETFs are based.

The amount that you will be paid on your notes at maturity, if they have not been automatically called, is based on the performance of the lesser performing underlier (the underlier with the lowest underlier return). The underlier return for each underlier is the percentage increase or decrease in its final level from its initial level.

If the underlier return for any underlier is less than -30%, the percentage of the face amount of your notes you will receive will be based on the performance of the underlier with the lowest underlier return. In such event, you will receive less than 70% of the face amount of your notes.

You should read the accompanying preliminary pricing supplement dated March 8, 2024, which we refer to herein as the accompanying preliminary pricing supplement, to better understand the terms and risks of your investment, including the credit risk of GS Finance Corp. and The Goldman Sachs Group, Inc.

|

|

KEY TERMS |

CUSIP/ISIN: |

40057YPH0 / US40057YPH08 |

Company (Issuer): |

GS Finance Corp. |

Guarantor: |

The Goldman Sachs Group, Inc. |

Underliers (each individually, an underlier): |

the Energy Select Sector SPDR® Fund (current Bloomberg symbol: “XLE UP Equity”) and the Utilities Select Sector SPDR® Fund (current Bloomberg symbol: “XLU UP Equity”) |

Underlying indices (each individually, an underlying index): |

with respect to the Energy Select Sector SPDR® Fund, the Energy Select Sector Index, and with respect to the Utilities Select Sector SPDR® Fund, the Utilities Select Sector Index |

Trade date: |

expected to be March 22, 2024 |

Settlement date: |

expected to be March 27, 2024 |

Determination date: |

expected to be March 22, 2027 |

Stated maturity date: |

expected to be March 25, 2027 |

|

|

|

Hypothetical Amount in Cash Payable on a Call Payment Date |

If your notes are automatically called on the first call observation date (i.e., on the first call observation date the closing level of each underlier is greater than or equal to its applicable call level), the amount in cash that we would deliver for each $1,000 face amount of your notes on the applicable call payment date would be the sum of $1,000 plus the product of the applicable call premium amount times $1,000. If, for example, the closing level of each underlier were determined to be 120% of its initial underlier level, your notes would be automatically called and the amount in cash that we would deliver on your notes on the corresponding call payment date would be 107.3% of the face amount of your notes or $1,073 for each $1,000 of the face amount of your notes. |

Hypothetical Payment Amount At Maturity |

|

The Notes Have Not Been Automatically Called |

|

Hypothetical Final Underlier Level

(as a % of the Initial Underlier Level) |

Hypothetical Payment Amount at Maturity

(as a % of Face Amount) |

175.000% |

143.800% |

150.000% |

143.800% |

125.000% |

143.800% |

110.000% |

143.800% |

100.000% |

143.800% |

97.000% |

143.800% |

95.000% |

143.800% |

90.000% |

143.800% |

85.000% |

100.000% |

80.000% |

100.000% |

70.000% |

100.000% |

69.999% |

69.999% |

50.000% |

50.000% |

25.000% |

25.000% |

|

0.000% |

0.000% |

This document does not provide all of the information that an investor should consider prior to making an investment decision. You should not invest in the notes without reading the accompanying preliminary pricing supplement and related documents for a more detailed description of the underlier, the terms of the notes and certain risks.

1

|

|

Payment amount at maturity (for each $1,000 face amount of your notes): |

●if the final underlier level of each underlier is greater than or equal to 90% of its initial underlier level, $1,438; ●if the final underlier level of any underlier is less than 90% of its initial underlier level but the final underlier level of each underlier is greater than or equal to 70% of its initial underlier level , $1,000; or ●if the final underlier level of any underlier is less than 70% of its initial underlier level, the sum of (i) $1,000 plus (ii) the product of (a) the lesser performing underlier return times (b) $1,000 |

Company’s redemption right (automatic call feature): |

if a redemption event occurs, then the outstanding face amount will be automatically redeemed in whole and the company will pay an amount in cash on the following call payment date, for each $1,000 of the outstanding face amount, equal to the sum of (i) $1,000 plus (ii) the product of (a) $1,000 times (b) the applicable call premium amount specified under “Call observation dates” below |

Redemption event: |

a redemption event will occur if, as measured on any call observation date, the closing level of each underlier is greater than or equal to its applicable call level |

Call level: |

with respect to any call observation date, the applicable call level specified in the table set forth under “Call observation dates” below; as shown in such table, the call level decreases the longer the notes are outstanding |

Initial underlier level: |

with respect to an underlier, to be determined on the trade date and will be an intra-day level or the closing level of such underlier on the trade date |

Final underlier level: |

with respect to an underlier, the closing level of such underlier on the determination date |

Underlier return: |

with respect to an underlier, the quotient of (i) its final underlier level minus its initial underlier level divided by (ii) its initial underlier level, expressed as a percentage |

Lesser performing underlier return: |

the underlier return of the lesser performing underlier |

Lesser performing underlier: |

the underlier with the lowest underlier return |

Call premium amount: |

with respect to any call payment date, the applicable call premium amount specified in the table set forth under “Call observation dates” below |

Maturity date premium amount: |

43.8% |

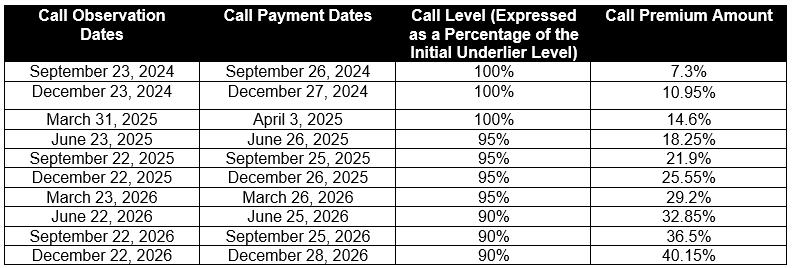

Call observation dates: |

expected to be the dates specified as such in the table below, commencing approximately six months after the trade date

|

Call payment dates: |

expected to be the dates specified as such in the table set forth under “Call observation dates” above |

Estimated value range: |

$925 to $955 (which is less than the original issue price; see accompanying preliminary pricing supplement) |

This document does not provide all of the information that an investor should consider prior to making an investment decision. You should not invest in the notes without reading the accompanying preliminary pricing supplement and related documents for a more detailed description of the underlier, the terms of the notes and certain risks.

2

GS Finance Corp. and The Goldman Sachs Group, Inc. have filed a registration statement (including a prospectus, as supplemented by the prospectus supplement, general terms supplement no. 8,999 and preliminary pricing supplement listed below) with the Securities and Exchange Commission (SEC) for the offering to which this communication relates. Before you invest, you should read the prospectus, prospectus supplement, general terms supplement no. 8,999 and preliminary pricing supplement, and any other documents relating to this offering that GS Finance Corp. and The Goldman Sachs Group, Inc. have filed with the SEC for more complete information about us and this offering. You may get these documents without cost by visiting EDGAR on the SEC web site at sec.gov. Alternatively, we will arrange to send you the prospectus, prospectus supplement, general terms supplement no. 8,999 and preliminary pricing supplement if you so request by calling (212) 357-4612.

The notes are part of the Medium-Term Notes, Series F program of GS Finance Corp. and are fully and unconditionally guaranteed by The Goldman Sachs Group, Inc. This document should be read in conjunction with the following:

This document does not provide all of the information that an investor should consider prior to making an investment decision. You should not invest in the notes without reading the accompanying preliminary pricing supplement and related documents for a more detailed description of the underlier, the terms of the notes and certain risks.

3

An investment in the notes is subject to risks. Many of the risks are described in the accompanying preliminary pricing supplement, accompanying general terms supplement no. 8,999, accompanying prospectus supplement and accompanying prospectus. Below we have provided a list of certain risk factors discussed in such documents. In addition to the below, you should read in full “Additional Risk Factors Specific to Your Notes” in the accompanying preliminary pricing supplement and “Additional Risk Factors Specific to the Notes” in the accompanying general terms supplement no. 8,999, as well as the risks and considerations described in the accompanying prospectus supplement and accompanying prospectus.

The following risk factors are discussed in greater detail in the accompanying preliminary pricing supplement:

|

|

|

Risks Related to Structure, Valuation and Secondary Market Sales ▪The Estimated Value of Your Notes At the Time the Terms of Your Notes Are Set On the Trade Date (as Determined By Reference to Pricing Models Used By GS&Co.) Is Less Than the Original Issue Price Of Your Notes ▪The Notes Are Subject to the Credit Risk of the Issuer and the Guarantor ▪You May Lose Your Entire Investment in the Notes ▪The Amount You Will Receive on a Call Payment Date or on the Stated Maturity Date, as the Case May Be, Will Be Capped ▪The Return on Your Notes May Change Significantly Despite Only a Small Change in the Level of the Lesser Performing Underlier ▪Your Notes Are Subject to Automatic Redemption ▪The Amount In Cash That You Will Receive on a Call Payment Date or on the State Maturity Date is Not Linked to the Closing Levels of the Underliers at Any Time Other Than on the Applicable Call Observation Date or the Determination Date, as the Case May Be ▪The Cash Settlement Amount Will Be Based Solely on the Lesser Performing Underlier ▪The Market Value of Your Notes May Be Influenced By Many Unpredictable Factors ▪If You Purchase Your Notes at a Premium to Face Amount, the Return on Your Investment Will Be Lower Than the Return on Notes Purchased at Face Amount and the Impact of Certain Key Terms of the Notes Will Be Negatively Affected ▪The Return on Your Notes Will Not Reflect Any Dividends Paid on the Underliers or the Underlier Stocks ▪We May Sell an Additional Aggregate Face Amount of the Notes at a Different Issue Price |

|

Additional Risks Related to the Underliers ▪The Policies of the Underlier Investment Advisor For Any Underlier and of the Underlying Index Sponsor of the Underlying Index Tracked By Any Underlier Could Affect the Amount Payable on Your Notes and Their Market Value ▪There Is No Assurance That an Active Trading Market Will Continue for the Underliers or That There Will Be Liquidity in Any Such Trading Market; Further, the Underliers are Subject to Management Risks, Securities Lending Risks and Custody Risks ▪Each Underlier and Its Underlying Index Are Different and the Performance of Each Underlier May Not Correlate With the Performance of Its Underlying Index Additional Risks Related to the Energy Select Sector SPDR® Fund ▪The Energy Select Sector SPDR® Fund is Concentrated in the Energy Sector and Does Not Provide Diversified Exposure ▪The Energy Select Sector SPDR® Fund May Be Disproportionately Affected By the Performance of a Small Number of Stocks Additional Risks Related to the Utilities Select Sector SPDR® Fund ▪The Utilities Select Sector SPDR® Fund is Concentrated in the Utilities Sector and Does Not Provide Diversified Exposure Risks Related to Tax ▪The Tax Consequences of an Investment in Your Notes Are Uncertain ▪Your Notes May Be Subject to the Constructive Ownership Rules ▪Foreign Account Tax Compliance Act (FATCA) Withholding May Apply to Payments on Your Notes, Including as a Result of the Failure of the Bank or Broker Through Which You Hold the Notes to Provide Information to Tax Authorities |

This document does not provide all of the information that an investor should consider prior to making an investment decision. You should not invest in the notes without reading the accompanying preliminary pricing supplement and related documents for a more detailed description of the underlier, the terms of the notes and certain risks.

4

The following risk factors are discussed in greater detail in the accompanying general terms supplement no. 8,999:

|

|

|

Risks Related to Structure, Valuation and Secondary Market Sales ▪If the Value of an Underlier Changes, the Market Value of Your Notes May Not Change in the Same Manner ▪Past Performance is No Guide to Future Performance ▪Your Notes May Not Have an Active Trading Market ▪The Calculation Agent Will Have the Authority to Make Determinations That Could Affect the Market Value of Your Notes, When Your Notes Mature and the Amount, If Any, Payable on Your Notes ▪The Calculation Agent Can Postpone the Determination Date, Averaging Date, Call Observation Date or Coupon Observation Date If a Market Disruption Event or Non-Trading Day Occurs or Is Continuing ▪With Respect to Notes Linked to Index Stocks or Exchange-Traded Funds, You Have Limited Anti-Dilution Protection ▪With Respect to Notes Linked to Exchange-Traded Funds, Except to the Extent GS&Co. and One or More of Our Other Affiliates Act as Authorized Participants in the Distribution of, and, at Any Time, May Hold, Shares of, the Applicable Exchange-Traded Fund to Which Your Notes Are Linked, There Is No Affiliation Between the Investment Advisor of such Exchange-Traded Fund and Us Risks Related to Conflicts of Interest ▪Other Investors in the Notes May Not Have the Same Interests as You |

|

▪Hedging Activities by Goldman Sachs or Our Distributors May Negatively Impact Investors in the Notes and Cause Our Interests and Those of Our Clients and Counterparties to be Contrary to Those of Investors in the Notes ▪Goldman Sachs’ Trading and Investment Activities for its Own Account or for its Clients Could Negatively Impact Investors in the Notes ▪Goldman Sachs’ Market-Making Activities Could Negatively Impact Investors in the Notes ▪You Should Expect That Goldman Sachs Personnel Will Take Research Positions, or Otherwise Make Recommendations, Provide Investment Advice or Market Color or Encourage Trading Strategies That Might Negatively Impact Investors in the Notes ▪Goldman Sachs Regularly Provides Services to, or Otherwise Has Business Relationships with, a Broad Client Base, Which May Include the Sponsors of the Underlier or Underliers or Constituent Indices, As Applicable, the Investment Advisors of the Underlier or Underliers, As Applicable, or the Issuers of the Underlier or the Underlier Stocks or Other Entities That Are Involved in the Transaction ▪The Offering of the Notes May Reduce an Existing Exposure of Goldman Sachs or Facilitate a Transaction or Position That Serves the Objectives of Goldman Sachs or Other Parties Risks Related to Tax ▪Certain Considerations for Insurance Companies and Employee Benefit Plans |

The following risk factors are discussed in greater detail in the accompanying prospectus supplement:

|

|

|

▪The Return on Indexed Notes May Be Below the Return on Similar Securities ▪The Issuer of a Security or Currency That Serves as an Index Could Take Actions That May Adversely Affect an Indexed Note ▪An Indexed Note May Be Linked to a Volatile Index, Which May Adversely Affect Your Investment ▪An Index to Which a Note Is Linked Could Be Changed or Become Unavailable |

|

▪We May Engage in Hedging Activities that Could Adversely Affect an Indexed Note ▪Information About an Index or Indices May Not Be Indicative of Future Performance ▪We May Have Conflicts of Interest Regarding an Indexed Note |

The following risk factors are discussed in greater detail in the accompanying prospectus:

|

|

|

Risks Relating to Regulatory Resolution Strategies and Long-Term Debt Requirements |

|

|

▪The application of regulatory resolution strategies could increase the risk of loss for holders of our securities in the event of the resolution of Group Inc. |

|

▪The application of Group Inc.’s proposed resolution strategy could result in greater losses for Group Inc.’s security holders |

This document does not provide all of the information that an investor should consider prior to making an investment decision. You should not invest in the notes without reading the accompanying preliminary pricing supplement and related documents for a more detailed description of the underlier, the terms of the notes and certain risks.

5

Goldman Sachs (NYSE:GS-K)

Historical Stock Chart

Von Apr 2024 bis Mai 2024

Goldman Sachs (NYSE:GS-K)

Historical Stock Chart

Von Mai 2023 bis Mai 2024